June 9, 2026

The Hidden Architecture of Holdco Debt: Why Capital Structure Design Defines Resource Conglomerate Survival

Across the global natural resources sector, some of the most consequential financial risks never appear in an operating company's balance sheet. They live one level above, at the holding company, where leverage is serviced not by direct earnings but by the willingness and capacity of subsidiaries to push cash upward through dividends, inter-company arrangements, and brand fee structures. When commodity cycles turn, this architectural vulnerability becomes the central plot of every refinancing crisis in the sector's history.

It is within this structural reality that the Vedanta Resources holdco debt restructuring becomes one of the most analytically rich corporate finance exercises unfolding in emerging market credit markets today. The transaction is not simply a refinancing. It is a deliberate attempt to redesign the capital architecture of a London-based parent whose financial health is tethered to the earnings rhythms of five soon-to-be-independent commodity businesses operating primarily in India.

When big ASX news breaks, our subscribers know first

Why Holdco Debt Is Structurally Different From Operating Company Debt

Understanding the Vedanta Resources holdco debt restructuring requires a clear grasp of what makes holding company debt fundamentally different from debt held at the operational level.

An operating company generates revenue directly, services its own obligations from that revenue, and maintains direct control over its assets. A holding company, by contrast, owns stakes in those operating businesses and must extract cash through dividend distributions, brand or royalty fee arrangements, and inter-company loan repayments to fund its own debt service. This creates a structural dependency that introduces layers of risk absent from the opco level.

In diversified natural resource conglomerates specifically, the relationship between commodity prices and mining performance directly shapes holdco liquidity. Consider these compounding structural pressures:

- Dividend capacity at the opco level contracts during commodity downturns, precisely when the holdco may need it most

- Large bullet repayment schedules create concentrated liquidity events that coincide, often destructively, with weak commodity price environments

- The holdco cannot simply reach into opco cash registers; it must navigate minority shareholder protections, regulatory obligations, and board-level governance at each subsidiary

- This creates a pro-cyclical liquidity squeeze, where the parent's ability to service debt diminishes at the same time its refinancing costs increase

This structural tension sits at the core of Vedanta Resources' current predicament and its proposed solution.

Snapshot: The Debt Position Driving the Restructuring Decision

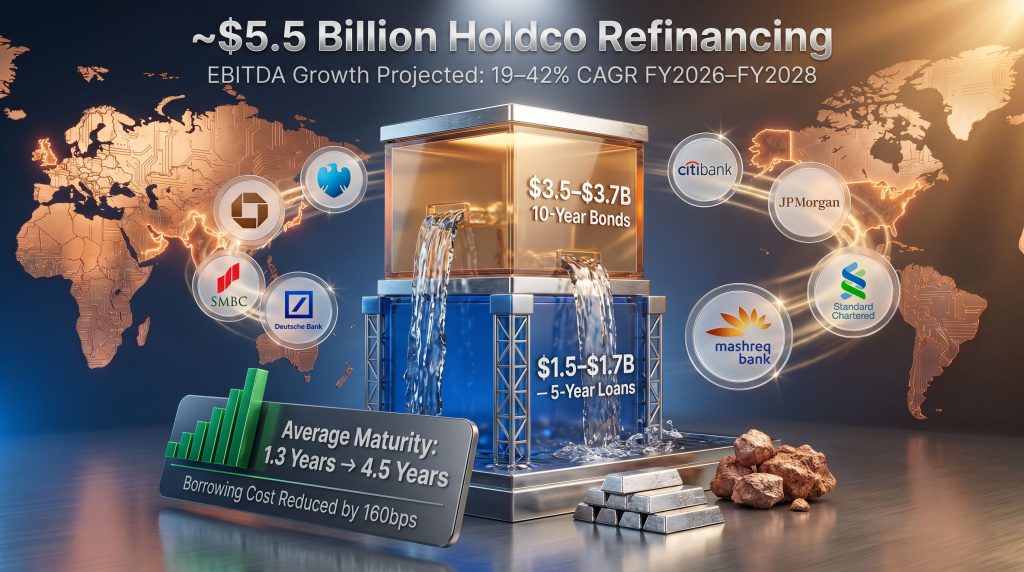

As of early 2026, Vedanta Resources carried approximately $5.25 to $5.5 billion in holdco-level debt, including an inter-company loan component of roughly $200 million. The near-term repayment obligations create a demanding cash flow schedule:

| Metric | Estimated Figure |

|---|---|

| Total Holdco Debt (February 2026) | ~$5.25–$5.5 billion |

| Inter-Company Loan Component | ~$200 million |

| Annual Debt Repayments (FY2026–FY2028) | $500–$600 million per year |

| Projected Obligation in FY2030 | ~$1.25 billion |

| Current Liquidity Position | $2.6 billion |

| Net Debt (Group Level) | $11.4 billion |

| Leverage Ratio (Current) | 2.0x (improved from 2.3x prior year) |

| Average Debt Maturity (December 2025) | ~4.5 years (up from 1.3 years two years prior) |

The improvement in average debt maturity from 1.3 years to 4.5 years over a two-year window is genuinely significant. It reflects sustained liability management discipline. However, the spike in obligations approaching FY2030 signals that the refinancing pressure has been redistributed forward in the maturity profile rather than extinguished entirely.

The critical insight here is that deferred refinancing risk is not resolved refinancing risk. The FY2030 obligation of approximately $1.25 billion represents a structural cliff that the current transaction must address with genuine finality.

The Two-Tranche Refinancing Architecture: Design Logic and Mechanics

Rather than pursuing a sequence of smaller liability management exercises, Vedanta Resources is targeting a single consolidated refinancing of its entire holdco debt stack. The strategic rationale is compelling: a unified transaction eliminates residual maturity mismatches, reduces the execution uncertainty of rolling sequential refinancings, and delivers a more decisive signal to credit markets about the group's financial reset.

The proposed structure separates the holdco liability into two distinct instruments:

Tranche 1: Long-Tenor Bonds

- Target raise: $3.5 to $3.7 billion

- Proposed maturity: 10 years

- Structure: Amortising over the full tenure, distributing principal repayments across the period

- Capital structure position: Junior to the loan tranche

Tranche 2: Medium-Term Amortising Loans

- Target raise: $1.5 to $1.7 billion

- Proposed maturity: 5 years

- Average maturity profile: approximately 2.5 to 3 years within the tenure

- Capital structure position: Senior to the bonds; expected to be repaid first

The design logic is elegant. By separating obligations into a senior amortising loan and a subordinated long-tenor bond, the structure creates a waterfall repayment mechanism that aligns principal repayments with the predictable cash generation cycle of operating subsidiaries. Bullet repayments, the historical source of Vedanta's refinancing cliff risk, are replaced by a spreading of obligations across time.

The shift from bullet to amortising instruments is a textbook correction to one of the sector's most persistent structural vulnerabilities. When large lump-sum repayments coincided with commodity downturns in prior cycles, the company faced pressure to upstream elevated dividends from operating entities, a response the market consistently penalised.

This design directly converts what was a refinancing event risk into a cash flow management exercise, a categorically different and more manageable problem. Furthermore, this approach mirrors broader trends in mining industry consolidation, where groups are increasingly rationalising their financial structures alongside operational ones.

The International Banking Syndicate: Geography as Strategy

Vedanta Resources has engaged at least eight major international financial institutions across multiple banking jurisdictions for the refinancing discussions:

| Bank | Headquarters Region |

|---|---|

| Citibank | United States |

| JP Morgan | United States |

| Barclays | United Kingdom |

| Standard Chartered | United Kingdom |

| Deutsche Bank | Germany |

| Sumitomo Mitsui Banking Corporation (SMBC) | Japan |

| Mashreq Bank | UAE |

| First Abu Dhabi Bank | UAE |

The deliberate inclusion of Middle Eastern banks alongside Western and Japanese institutions is not incidental. It reflects a strategic decision to diversify the creditor base beyond traditional Western capital market relationships. For a group with significant exposure to emerging market credit conditions, broadening the lender pool reduces concentration risk and expands the available liquidity base.

The participation of Gulf-region institutions also signals growing appetite among Middle Eastern capital for resource-sector debt paper, a trend with broader implications for how Indian conglomerates access international credit.

The Demerger Complication: Five Entities, One Cash Flow Need

Vedanta Resources holds approximately 56% of Vedanta Ltd., which is in the process of being restructured into five separate listed entities spanning distinct commodity verticals. While the demerger is designed to unlock shareholder value by creating pure-play commodity businesses with clearer capital structures and standalone credit profiles, it introduces meaningful complexity for the holding company's cash flow model.

Previously, the holdco received dividends from a single consolidated subsidiary. Post-demerger, it must coordinate dividend and brand fee flows from five independent entities, each with:

- Its own board and minority shareholders

- Separate regulatory obligations and governance frameworks

- Distinct dividend policies and capital allocation priorities

- Individual credit ratings and funding access profiles

This aggregation challenge is not trivial. Bond markets have been closely watching whether the demerger process will, in practical terms, impair the holdco's ability to access cash flows from the newly independent subsidiaries. Indeed, the strategic focus on core assets that underpins the demerger logic must be balanced against the practical cash flow requirements of the parent.

Brand Fees as a Contractual Cash Flow Anchor

One mechanism providing some stability in the post-demerger cash flow model is the brand fee arrangement. The spun-off entities will pay brand fees of approximately 3% of turnover to the holdco through FY2029. The copper business carries a reduced rate of 0.75%, reflecting its different scale and profitability profile.

Historically, annual brand fees from Vedanta Ltd. have totalled approximately $350 million. Fitch Ratings has projected that combined brand fees and opco dividends will cover $800 million to $1 billion of annual holdco debt service obligations between FY2026 and FY2029, providing a meaningful contractual floor beneath the holdco's liquidity position.

The next major ASX story will hit our subscribers first

What Credit Rating Agencies Are Saying

The rating agency landscape for Vedanta Resources reflects genuinely divergent analytical conclusions, and that divergence itself is informative for investors.

S&P Global issued a ratings upgrade with a constructive forward outlook, projecting group EBITDA of approximately $7 billion in both FY2027 and FY2028. The agency estimates that improved earnings combined with moderated dividend distributions will expand discretionary cash flow materially:

- FY2027: Adjusted debt declines by approximately $500 million

- FY2028: Adjusted debt declines by approximately $1 billion

- FFO-to-debt ratio expected to remain comfortably above 30% over the next 12 to 24 months

Fitch Ratings acknowledges the group's improved financial discipline, citing proactive refinancing activity, smoother maturity profiles, and declining borrowing costs as positive developments. However, Fitch characterises management's target of reducing holdco debt to $3 billion by FY2027 as ambitious, implying a meaningful gap between the company's stated timeline and what the agency views as achievable.

Moody's has previously assigned Vedanta Resources a Caa2 credit rating, a position deep within speculative-grade territory that reflects the agency's historical view of elevated refinancing risk and structurally weak credit quality at the holdco level.

The divergence between S&P's upgraded outlook and Moody's Caa2 rating is not a technicality. It reflects genuine analytical disagreement about the sustainability of cash flow generation and the achievability of deleveraging targets. Bond market participants will price this uncertainty directly into the new instruments.

The Earnings Engine: EBITDA Growth Projections and Key Commodities

The credibility of the entire refinancing narrative rests on whether the group's operating subsidiaries can deliver the earnings growth that supports both debt service and deleveraging. Consequently, understanding the underlying commodity dynamics is essential to assessing the transaction's viability.

Analysts have estimated that all listed Vedanta group entities are projected to deliver 19 to 42% EBITDA compound annual growth rates over FY2026 to FY2028, with the notable exception of the oil and gas segment. This range of projected growth is substantial, and if sustained, it would meaningfully improve the holdco's debt service capacity.

Key earnings growth drivers include:

- Aluminium: Backward integration through bauxite and coal mine development is designed to reduce input cost volatility; these projects, though delayed, are targeted for completion in FY2027

- Zinc (Hindustan Zinc): A 250 kilotonne expansion at the Debari plant in Rajasthan is expected to anchor earnings growth for the group over the medium term

- Zinc International and Copper: The group has outlined cumulative capital expenditure of approximately $8 billion over the medium term, with priority allocation to these two segments

The borrowing cost trajectory also supports the earnings story. The group refinanced $550 million of high-cost debt during the first half of the last fiscal year, reducing average borrowing costs by 160 basis points year-on-year to approximately 10%. Lower debt service costs at the opco level preserve more free cash flow for dividend distribution upward to the holdco.

Capital Allocation: The Central Tension in the Investment Case

Perhaps the most underappreciated risk in the Vedanta Resources holdco debt restructuring narrative is the capital allocation tension at the subsidiary level. The group's cumulative capex commitment of approximately $8 billion over the medium term is substantial. Every dollar directed toward zinc expansion in Rajasthan or new copper capacity is a dollar not available for dividend distribution to the holding company.

This tension is not hypothetical. It is a structural feature of any resource conglomerate pursuing simultaneous growth investment and holdco deleveraging. The key variables to monitor:

- Dividend payout ratios at each of the five demerged entities post-listing

- Capex execution timing across zinc, copper, and aluminium projects

- Minority shareholder positions at entities like Hindustan Zinc, which may create governance constraints on dividend upstreaming

- Commodity price trajectories for aluminium, zinc, and copper, which directly determine opco free cash flow availability

Scenario Analysis: Three Trajectories for the Holdco Debt Profile

| Scenario | Key Assumptions | Holdco Debt by FY2028 | Outcome |

|---|---|---|---|

| Base Case | Full refinancing completed; EBITDA reaches $7bn | ~$4.3 billion | Credit profile improves; potential ratings upgrade |

| Stress Case | Partial refinancing; EBITDA $5.5–$6bn; reduced dividends | Above $5 billion | Continued refinancing pressure; negative rating risk |

| Adverse Case | Demerger disruption; credit markets deteriorate | Liquidity runway narrows by FY2027 | Potential asset disposals or further liability management |

Key Risk Factors That Could Derail the Restructuring

Four dimensions of vulnerability warrant active monitoring. In addition, broader commodity market turmoil and geopolitical risks in mining could amplify any of these pressures significantly:

-

Commodity price sensitivity: Aluminium and zinc pricing directly determines opco EBITDA and dividend capacity. Backward integration reduces but does not eliminate this exposure.

-

Demerger execution complexity: Five independent entities mean five separate boards, five governance frameworks, and five sets of minority shareholders, all of which could constrain practical dividend accessibility.

-

Capital allocation discipline: The $8 billion medium-term capex commitment creates a direct mathematical tension with the holdco's deleveraging ambitions. Higher opco investment means lower upstreamed cash flow.

-

Global credit market conditions: The success of the bond issuance depends on sustained appetite for high-yield emerging market paper. Rising interest rates or risk-off sentiment could increase the cost or reduce the achievable volume of the new bonds.

Frequently Asked Questions: Vedanta Resources Holdco Debt Restructuring

What is the total size of Vedanta Resources' holdco debt being refinanced?

Vedanta Resources is seeking to refinance approximately $5.25 to $5.5 billion of holding company debt, comprising a mix of bonds and loans, as of early 2026.

How is the new debt being structured?

The refinancing is divided into two tranches: approximately $3.5 to $3.7 billion in 10-year amortising bonds ranked junior in the capital structure, and $1.5 to $1.7 billion in 5-year amortising loans ranked senior. Both instruments use amortising rather than bullet repayment structures.

Why is Vedanta pursuing this refinancing now?

Annual debt repayment obligations of $500 to $600 million per year through FY2028 rise sharply to approximately $1.25 billion in FY2030. The consolidated refinancing aims to smooth this repayment profile and align debt service with predictable cash flows from operating subsidiaries.

How does the Vedanta Ltd. demerger affect the holdco's financial position?

The demerger creates five independent listed entities, each with separate credit profiles and dividend policies. While it improves operational clarity, it introduces complexity in aggregating cash flows to the holdco and raises practical questions about dividend accessibility. S&P's recent analysis highlights these structural considerations in detail.

What do credit rating agencies say about the restructuring?

S&P Global has issued an upgraded outlook projecting $7 billion EBITDA by FY2027 and meaningful debt reduction. Fitch acknowledges improved discipline but considers the FY2027 debt target of $3 billion ambitious. Moody's has previously rated VRL at Caa2, reflecting elevated refinancing risk.

What is the role of brand fees in the holdco's cash flow model?

Brand fees charged at approximately 3% of turnover from the demerged entities through FY2029 (with a reduced 0.75% rate for copper) provide a contractual income stream supplementing dividend flows. Combined with opco dividends, these are projected by Fitch to cover $800 million to $1 billion of annual debt service.

Strategic Verdict: Progress Without Finality

The Vedanta Resources holdco debt restructuring represents genuine strategic progress. The transition from bullet to amortising instruments corrects a well-documented structural flaw. The extension of average debt maturity from 1.3 years to 4.5 years over two years demonstrates that the group is capable of executing complex liability management at scale. The 160 basis point reduction in average borrowing costs confirms improving credit market access.

However, the bull case and bear case for this transaction remain separated by a meaningful analytical gap. The deleveraging narrative depends on three variables that remain genuinely uncertain: the trajectory of aluminium and zinc prices, the practical dividend accessibility from five newly independent subsidiaries each with their own governance constraints, and the discipline of capital allocation in a group simultaneously committed to $8 billion of growth investment.

The bond market's pricing of the new instruments, when they are ultimately issued, will provide the most honest real-time verdict on which scenario creditors find more convincing. For now, the structural redesign is sound. Whether the operating fundamentals deliver the cash flows required to make it credible is the question that will define Vedanta Resources' credit trajectory through the end of the decade.

This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and credit ratings cited are sourced from publicly available analyst reports and rating agency publications and are subject to change. Investors should conduct independent due diligence before making any financial decisions.

Want To Identify ASX Mineral Discoveries Before The Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable investment insights for both short-term traders and long-term investors — begin your 14-day free trial today and explore the historic returns major mineral discoveries have generated.