July 16, 2026

The Upstream Capital Problem That Earthquakes Did Not Create

Long-cycle energy investment rarely fails because of geological surprises. It fails because the conditions required to justify capital commitment — contract enforceability, infrastructure reliability, fiscal predictability, and political stability — deteriorate faster than investors can reprice their exposure. Venezuela has spent years accumulating exactly these kinds of structural deficits, and the June 2026 seismic events did not introduce a new investment thesis. They forced a reckoning with one that had been quietly building for over a decade.

Understanding Venezuela earthquake oil investment risks requires separating the physical from the structural. The tremors, measuring magnitudes of 7.2 and 7.5, caused devastating humanitarian consequences across northern and coastal regions of the country, with Al Jazeera reporting thousands of deaths and widespread infrastructure disruption. Yet for capital allocators assessing upstream exposure, the more consequential damage was not to oilfields — it was to an already-fragile system of power generation, logistics, and institutional credibility that Venezuela's production recovery had been quietly depending on.

When big ASX news breaks, our subscribers know first

Why Venezuela's Production Recovery Was Always Fragile

Output Gains Without Capital Conviction

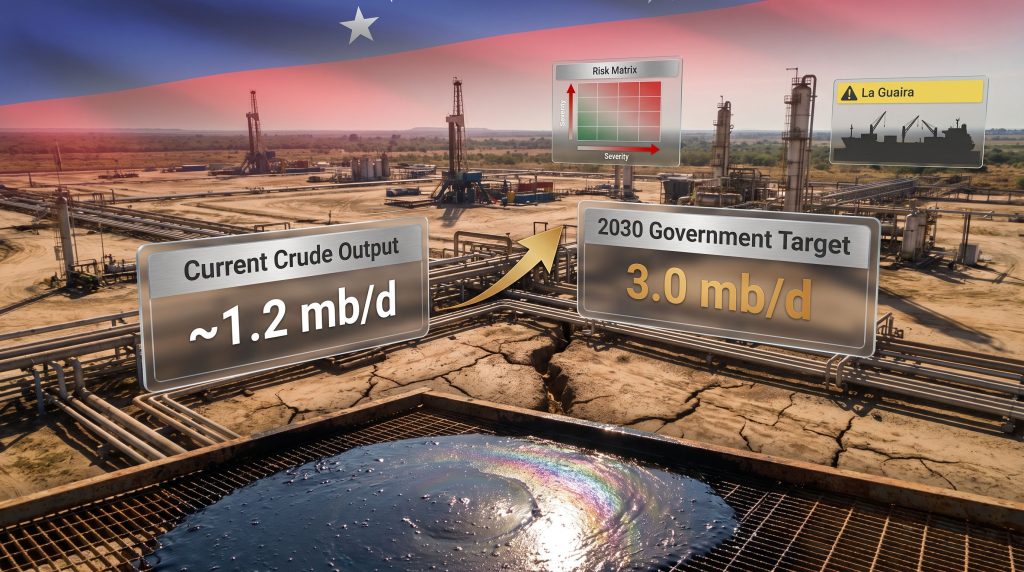

Venezuela's crude production had climbed to approximately 1.2 million barrels per day (mb/d) ahead of the June 2026 earthquakes, with Reuters reporting export volumes reaching roughly 1.25 mb/d in May 2026. On the surface, these figures suggested momentum. Beneath that surface, however, the recovery rested on existing joint venture frameworks and legacy infrastructure rather than new capital commitment cycles.

This distinction matters enormously. Production growth driven by incremental optimisation of existing assets has a ceiling. Achieving the government's stated 2030 target of 3.0 mb/d — a 2.5x increase from current levels — requires entirely different conditions: greenfield development programmes, grid expansion, port upgrades, and the kind of long-term contractual certainty that attracts institutional capital. None of those conditions were in place before June 2026, and the seismic events have made each of them harder, not easier, to establish.

How Venezuela Compares to Peer Frontier Markets

Comparable heavy crude jurisdictions illustrate the gap between output recovery and genuine investment attractiveness. Canadian heavy crude alternatives such as the oil sands and Kazakhstan's Kashagan field attracted sustained upstream capital only after demonstrating consistent contract enforceability and regulatory predictability across multiple investment cycles. Venezuela, by contrast, has struggled to convert preliminary commercial arrangements into binding long-term commitments — a structural disconnect that predates the earthquakes by years.

| Production Metric | Pre-Earthquake Level | 2030 Government Target | Gap |

|---|---|---|---|

| Crude Output | ~1.2 mb/d | 3.0 mb/d | ~1.8 mb/d |

| Export Volume (May 2026) | ~1.25 mb/d | Not publicly specified | Significant |

| Power Generation Availability | Less than 40% of installed capacity | Adequate for 3.0 mb/d target | Severe shortfall |

| Orinoco Belt Development Stage | Partial joint ventures active | Full upstream buildout required | Multi-decade capital programme needed |

The 2030 production target requires not just drilling activity but also grid stabilisation, expanded port throughput, and contract reform — none of which are on a credible near-term delivery path under current conditions.

Five Risk Dimensions That Must Be Re-Priced

Risk Dimension 1: Power Grid Instability as a Production Constraint

Venezuela's electricity system was already under severe stress before the earthquakes struck. Reuters reported in May 2026 that less than 40% of the country's installed generation capacity was available — a level that, for most industrial economies, would trigger emergency infrastructure programmes. In Venezuela, it had become the operational baseline.

The June seismic events pushed an already-fragile grid further into dysfunction, triggering blackouts across multiple states including Carabobo and Aragua — regions critical to energy logistics and industrial operations. What makes this particularly consequential for upstream investors is the energy profile of Venezuelan crude itself. Extra-heavy oil extracted from the Orinoco Belt is among the most energy-intensive crude grades in the world to process. Upgrading, pumping, and transporting Orinoco crude requires continuous high-voltage industrial power that an unstable grid simply cannot guarantee.

Production volatility caused by power interruptions creates a cascading problem for joint venture partners: revenue forecasts become unreliable, offtake schedules break down, and the financial modelling that underpins long-cycle investment decisions loses validity. Grid weakness, it is worth emphasising, is not a seismic problem. It reflects chronic underinvestment that has been accumulating for well over a decade. The earthquakes simply removed the option of treating it as a manageable background risk.

Risk Dimension 2: Logistics, Port Infrastructure, and Export Chain Disruption

La Guaira port was placed under a formal disaster declaration following the June earthquakes, creating immediate uncertainty across the export chain even where terminal infrastructure had not been physically destroyed. Road network damage and localised power outages compounded shipping delays, translating into elevated freight costs, higher insurance premiums, and increased demurrage charges on crude cargoes.

The downstream exposure extends well beyond Venezuela's borders. India has emerged as a significant destination for Venezuelan crude in recent years, with ONGC Videsh holding direct equity stakes in Venezuelan upstream projects. Supply disruptions — even temporary ones rooted in logistics rather than production failures — force Indian refiners to source replacement heavy crude at premium cost, adding supply chain complexity and compressing refinery margins. For ONGC Videsh specifically, the situation creates a dual exposure: simultaneous operational disruption and asset valuation risk within the same investment portfolio.

Risk Dimension 3: The Asymmetry Between IOC and State Asset Vulnerability

One of the more nuanced findings from the post-earthquake assessment is the pronounced divergence between internationally operated and state-managed asset performance. Major operators including Chevron, Eni, and Repsol confirmed continued operations with no material production interruptions attributable directly to seismic damage — a testament to the higher maintenance standards and capital discipline typically applied by international oil companies.

State-controlled assets told a different story. El Palito refinery reported partial offline status in the earthquake aftermath, while Pequiven Morón petrochemical complex experienced reported storage tank integrity issues, though official confirmation through state channels remained limited. Morón operations were subsequently restarted, but the episode crystallised a pattern that experienced investors in Venezuela already understand: the vulnerability of PDVSA-managed infrastructure is structural, not incidental.

| Asset Type | Operator | Post-Earthquake Status | Investment Signal |

|---|---|---|---|

| Orinoco Belt upstream fields | Chevron, Eni, Repsol JVs | Operations confirmed continuing | Low direct damage risk |

| El Palito Refinery | PDVSA | Partial offline reported | High state asset vulnerability |

| Pequiven Morón Complex | PDVSA | Storage tank issues reported | Chronic maintenance deficit exposed |

| La Guaira Port | State-managed | Disaster declaration issued | Logistics risk elevated |

| National Power Grid | State-managed | Multi-state blackouts | Systemic fragility confirmed |

Risk Dimension 4: Political Risk, Contract Mechanics, and Fiscal Reform Delays

Emergency response environments historically consume government administrative bandwidth in ways that delay energy sector reform timelines. The fiscal and regulatory attention required to manage post-disaster recovery competes directly with the institutional capacity needed to advance upstream contract modernisation — and in Venezuela's case, that capacity was already constrained before the earthquakes.

Venezuela's upstream fiscal framework presents commercial complexity that foreign investors have struggled to navigate. Payment arrangements combining cash, goods, and services — including oil prepayment structures — complicate balance sheet management and make revenue predictability difficult for joint venture partners. Early 2026 saw gas agreements concluded between the government and operators including Repsol and Eni, demonstrating continued commercial engagement. However, these arrangements have not catalysed broader upstream capital commitment, pointing to the persistent gap between preliminary agreements and the kind of binding, internationally arbitrable contracts that institutional investors require.

The US sanctions architecture adds a further layer of constraint. Shifts in the US policy on PDVSA have directly shaped the universe of eligible capital providers, reducing the competitive tension in upstream licensing that would otherwise accelerate deal-making and improve fiscal terms for the Venezuelan government. Furthermore, the broader oil price geopolitics at play in 2025 and 2026 have compounded these pressures, making the post-disaster environment harder to navigate politically.

Risk Dimension 5: Sovereign Risk and Macroeconomic Shock Absorption

Preliminary economic loss estimates from the June 2026 earthquakes range from $1 billion to $8 billion, representing approximately 1 to 7% of Venezuela's GDP. Tail risk scenarios project potential total losses reaching $100 billion if recovery efforts stall and secondary economic effects compound over multiple years.

For investment structures that depend on Venezuelan government co-financing or royalty reinvestment, this fiscal deterioration creates a feedback loop that experienced investors in distressed sovereign markets will recognise immediately. Weaker government finances reduce PDVSA's capacity to fund its share of joint venture capital obligations. That in turn either increases the financial burden on international partners or triggers production curtailments that reduce revenue for everyone involved. Sovereign fiscal fragility and upstream production risk are not separate variables in Venezuela — they are directly linked through the joint venture architecture that governs most of the country's producing assets.

The Before-and-After Risk Matrix

| Risk Factor | Pre-Earthquake Status | Post-Earthquake Status | Severity Change |

|---|---|---|---|

| Power grid reliability | Critical (less than 40% capacity) | Deteriorated — multi-state blackouts | Increased significantly |

| Port and logistics stability | Functional with chronic inefficiencies | Disrupted — La Guaira disaster declaration | Increased moderately |

| Direct oilfield damage | Not applicable | Minimal for IOC-operated assets | Low |

| State asset vulnerability | Chronic maintenance deficit | Exposed by refinery and tank incidents | Increased moderately |

| Political reform momentum | Slow but present | Diverted by emergency response | Increased moderately |

| Fiscal and sovereign stability | Fragile | Worsened by $1 to $8 billion loss estimates | Increased significantly |

| Contract enforceability | Uncertain | Environment more complex post-disaster | Increased moderately |

| International operator confidence | Cautious but engaged | Operations maintained; no new commitments | Unchanged |

Heavy Crude Market Pricing and What It Signals

The Risk Premium Embedded in Heavy Crude Spreads

Venezuelan supply uncertainty carries pricing implications that extend well beyond the country's borders. Global crude markets price a risk premium for heavy and sour crude grades when Venezuelan output reliability comes into question — a dynamic that affects U.S. Gulf Coast refinery margins dependent on heavy crude feedstocks and shapes purchasing decisions across Asian import markets simultaneously.

The heavy-light crude spread functions as a sensitive barometer of Venezuelan supply credibility. Widening spreads signal market concern about sustained disruptions, while a narrowing spread indicates restored confidence. For investors holding Venezuelan upstream equity, this dynamic creates a counterintuitive tension: elevated risk premiums may improve near-term revenue per barrel while simultaneously reflecting the structural instability that makes additional capital commitment difficult to justify. The broader sanctions and oil trading environment reinforces this dynamic, as parallel constraints on Russian crude have reshaped global heavy crude flows in ways that indirectly affect Venezuelan market positioning.

Asian Importers and the Diversification Response

India's growing reliance on Venezuelan crude has created a meaningful vulnerability for its refining sector. When Venezuelan logistics break down, Indian refiners face not just higher costs but also the need to establish alternative supply relationships at short notice — typically with competing heavy crude exporters who are positioned to command premium pricing precisely because of Venezuela's reliability deficit. Consequently, the geopolitical risk landscape affecting resource-producing nations in 2025 and 2026 has made supply diversification a strategic imperative rather than a precautionary measure for Asian importers.

What a Credible Investment Recovery Actually Requires

Assessing Venezuela earthquake oil investment risks honestly means acknowledging that recovery is not simply a matter of infrastructure repair. Four structural preconditions must be met before new upstream capital commitments become commercially rational:

-

Grid stabilisation at scale — not incremental repairs, but a fundamental overhaul of generation and transmission infrastructure capable of supporting energy-intensive Orinoco Belt operations continuously.

-

Contract reform with enforceable mechanisms — transition from hybrid payment arrangements to transparent upstream contracts with internationally arbitrable dispute resolution provisions.

-

An expanded universe of eligible capital providers — whether through formal sanctions relief or structured licensing exemptions, the competitive pool of investors must widen before deal economics can improve.

-

A demonstrated operational track record — a sustained period of at least 12 to 18 months of uninterrupted production, export, and payment performance is the minimum threshold for rebuilding institutional capital market confidence.

Even in an optimistic scenario where all four preconditions are met simultaneously, the lag between capital commitment and production impact in the Orinoco Belt is measured in years rather than quarters. Venezuela's 3.0 mb/d target for 2030 is structurally implausible under any realistic capital deployment timeline.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Venezuela Earthquake Oil Investment Risks

Did the June 2026 earthquakes directly damage Venezuela's major oilfields?

Direct physical damage to core production assets, particularly in the Orinoco Belt, was reported as minimal. Major international operators confirmed continued operations. The primary disruption pathways were indirect: power grid failures, port logistics disruption, and heightened political uncertainty rather than physical oilfield damage. S&P Global similarly confirmed that Venezuelan oil production and refining remained broadly unharmed by the June 24 earthquakes.

What magnitude were the Venezuela earthquakes in June 2026?

Two significant seismic events were recorded, measuring magnitudes of 7.2 and 7.5, causing widespread humanitarian impact and infrastructure disruption across northern and coastal regions.

Which international oil companies are currently operating in Venezuela?

Chevron, Eni, and Repsol maintain active upstream positions, primarily through joint venture structures with state oil company PDVSA.

What is Venezuela's current oil production and its 2030 target?

Crude output stood at approximately 1.2 mb/d before the earthquakes, with export volumes reaching roughly 1.25 mb/d in May 2026 according to Reuters. The government's 2030 target of 3.0 mb/d represents a level requiring sustained foreign capital that current conditions are unlikely to attract.

What is the estimated economic damage from the June 2026 earthquakes?

Preliminary estimates place direct losses in the range of $1 billion to $8 billion, equivalent to approximately 1 to 7% of Venezuela's GDP, with tail risk scenarios projecting up to $100 billion in total economic impact if recovery stalls.

Key Takeaways for Capital Allocators

The strategic conclusion for investors assessing Venezuela earthquake oil investment risks is that the June 2026 seismic events functioned as a stress test that quantified pre-existing fragility rather than a catalyst that created new risk categories.

-

The most material investment risks are above-ground and institutional in nature — power infrastructure, contract enforceability, sanctions constraints, and sovereign fiscal health.

-

International operators maintaining current positions are doing so on the basis of existing contractual obligations, not new capital conviction.

-

Infrastructure resilience due diligence — particularly power grid stability and port operational continuity — should be weighted as primary risk variables in any Venezuela upstream assessment.

-

Investors should model extended disruption timelines rather than assuming rapid post-earthquake normalisation, given Venezuela's chronic maintenance deficit.

-

Heavy crude spread dynamics are a meaningful early-warning indicator of Venezuelan supply reliability even for investors without direct in-country exposure.

The earthquakes will likely be assessed in retrospect not as the cause of Venezuela's investment challenges but as the event that made it impossible to treat those challenges as acceptable background noise. The structural reform agenda required to change that assessment remains unaddressed — and without it, the gap between Venezuela's production ambitions and the capital conditions necessary to achieve them will continue to widen.

Disclaimer: This article contains forward-looking analysis, forecasts, and scenario projections based on publicly available information as of mid-2026. It does not constitute investment advice. Readers should conduct independent due diligence before making any capital allocation decisions related to Venezuelan upstream assets or related markets.

For additional coverage of Latin American energy markets, upstream investment dynamics, and regional policy developments, visit World Energy Wire.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

While Venezuela's structural investment risks underscore the importance of jurisdictional clarity and real-time information, Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries — transforming complex data across 30+ commodities into clear, actionable insights for both traders and long-term investors. Explore how major discoveries have historically generated exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.