June 17, 2026

Why Giant Copper Districts Are Being Revalued Worldwide

Copper projects are no longer judged only by headline tonnage. Investors, lenders, and miners increasingly screen for a narrower set of qualities: long mine life, scalable processing, by-product credits, jurisdictional durability, and the ability to justify multibillion-dollar infrastructure spending over decades rather than cycles.

That backdrop helps explain why the Vicuña copper megaproject in Argentina has become one of the most closely watched undeveloped mining systems in the world. Instead of a single pit or a conventional standalone operation, Vicuña is being assessed as a district-scale Andean copper-gold-silver development with enough size to influence corporate strategy, regional infrastructure planning, and Argentina's future place in global copper supply.

For resource investors, the real question is not simply whether Vicuña is large. It is whether a project of this scale can move from geological promise to executable capital plan without being undermined by cost inflation, timing slippage, water constraints, or shifts in sovereign risk. Furthermore, the broader copper supply crunch facing global markets only heightens the scrutiny applied to every undeveloped district of this magnitude.

In very large copper developments, orebody quality matters first, but execution discipline often determines whether value is created or destroyed.

When big ASX news breaks, our subscribers know first

What Is the Vicuña Copper Megaproject in Argentina?

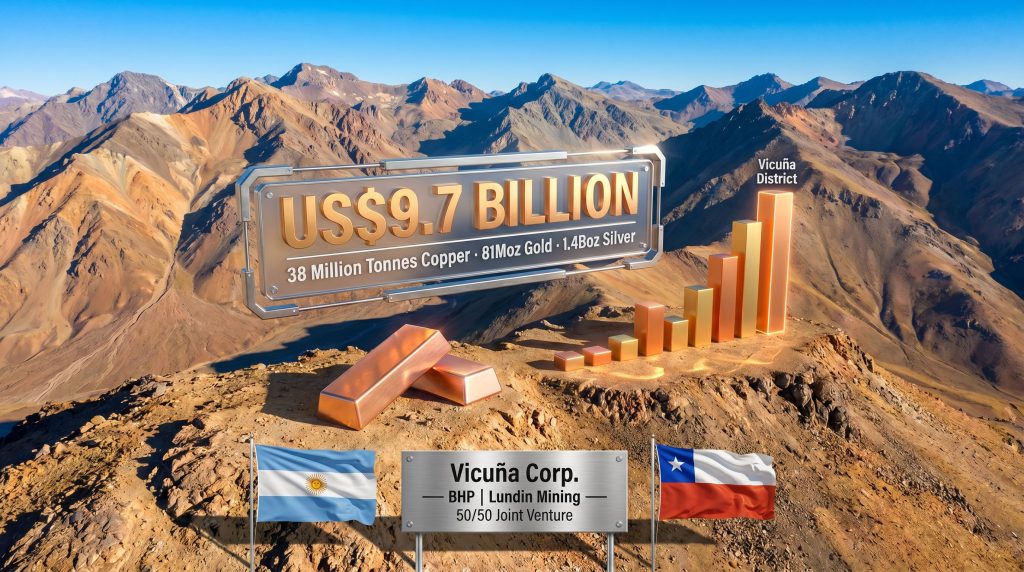

The Vicuña copper megaproject in Argentina refers to a district-scale mining development centered on the Josemaría and Filo del Sol deposits in the broader Vicuña district, spanning San Juan province and the Chile-Argentina border region. The assets are being advanced through Vicuña Corp., a 50/50 joint venture between Lundin Mining and BHP.

What makes the district unusual is the integrated development logic. Rather than treating each deposit as a separate mining story, the joint venture is evaluating the area as a shared mineral system with common infrastructure, processing options, logistics planning, and capital sequencing. This approach mirrors the strategy behind other prominent examples, such as the major copper-gold project at Reko Diq, where district-level thinking has similarly reshaped the investment conversation.

Across all resource categories cited in company disclosures and widely referenced industry reporting, the district is reported to contain approximately:

- 38 million tonnes of copper

- 81 million ounces of gold

- 1.4 billion ounces of silver

Those are exceptional numbers in any jurisdiction. They place Vicuña among the most significant undeveloped copper-rich systems globally, particularly because precious metals by-products may materially affect operating margins and payback dynamics.

Why Copper Majors Care About District-Scale Systems

Large mining houses tend to prefer deposits that can support:

- multi-decade production profiles

- phased capital deployment

- optionality across changing commodity prices

- processing optimisation over time

- infrastructure amortisation over very large throughput bases

In that sense, Vicuña fits the strategic profile of a potential Tier 1 asset, even though it remains in the pre-production stage and still faces engineering, environmental, permitting, and financing milestones before any construction timeline becomes bankable.

How Vicuña Compares With Major Undeveloped Copper Assets

Not all large copper resources are equal. Investors often confuse scale with economic quality. In reality, the market applies a premium only when scale is paired with mining width, metallurgy, recoveries, strip ratio potential, logistical feasibility, and co-product value.

A simplified comparison framework looks like this:

| Metric | Why it matters for valuation | Vicuña significance |

|---|---|---|

| Resource size | Supports mine life and throughput scale | Globally significant across copper, gold, and silver |

| By-product credits | Can lower effective copper costs | Strong due to gold and silver endowment |

| District optionality | Allows staged development and redesign | High because Josemaría and Filo del Sol can be sequenced |

| Sponsor quality | Improves financing and execution confidence | Strengthened by BHP and Lundin Mining |

| Infrastructure burden | Drives capex intensity and schedule risk | Material challenge due to altitude and region |

One lesser-known point in large Andean systems is that district thinking can be more valuable than individual deposit economics. A standalone feasibility study may understate value if nearby deposits later share power, water, roads, camps, haulage routes, or processing facilities. That potential synergy is part of why major miners often revisit older project assumptions once district consolidation occurs. Consequently, analysts tracking the major copper system in Argentina have increasingly focused on precisely these infrastructure-sharing dynamics.

Argentina's RIGI Framework and Why It Matters

A major part of the investment case around the Vicuña copper megaproject in Argentina is the country's RIGI, or Régimen de Incentivo para Grandes Inversiones. This framework was created to attract large-scale capital commitments by offering a more predictable investment setting for qualifying projects. According to Panorama Minero, Vicuña has already begun its formal RIGI admission process, marking a significant step forward for the project.

The regime is generally understood to include benefits such as:

- longer-term fiscal stability provisions

- changes affecting export duties

- protections tied to access to and repatriation of foreign currency, subject to the framework's conditions

- a more structured regulatory pathway for very large investments

Vicuña's inclusion under RIGI is important because Argentina has historically struggled to attract large-scale foreign direct investment consistently. Currency controls, inflation, tax uncertainty, and sovereign risk have frequently raised hurdle rates for long-dated mining projects.

A Framework Is Not the Same as Project-Specific Support

It is important to be precise here. RIGI is a policy framework, not proof that a project has guaranteed economic success. It does not eliminate:

- environmental approval risk

- construction risk

- cost overruns

- political change over a multi-decade mine life

- commodity price volatility

So while RIGI may improve the investment architecture, it should not be confused with assured delivery.

Policy certainty can narrow a discount rate, but it cannot replace geology, engineering, or social licence.

Breaking Down the US$9.7 Billion Initial Commitment

The investment figures associated with Vicuña need careful interpretation because they refer to different development scopes and timeframes.

Here is the capital structure as widely discussed in the market:

| Development scope | Capital estimate | Main purpose |

|---|---|---|

| Josemaría Phase 1 | ~US$7.1 billion | Mine, plant, and core operating infrastructure |

| Broader staged development | ~US$11 billion | Expansion logic across Josemaría and Filo del Sol |

| Extended district build-out | US$15 billion to US$18 billion | Wider infrastructure and integrated full-scale potential |

| RIGI-approved initial commitment | US$9.7 billion | Anchor foreign investment for the first major stage |

This staged approach is common in world-class copper developments for several reasons:

- It reduces upfront execution risk by focusing first on the most construction-ready component.

- It preserves flexibility if engineering data, metallurgical work, or market conditions change.

- It helps match funding sources to clearer development milestones.

- It can improve financing outcomes if early-stage infrastructure supports later district expansion.

From a funding standpoint, the eventual financing mix could include corporate capital, project debt, and potentially streaming, royalty, or other structured instruments. However, the final form remains dependent on feasibility outcomes, market conditions, and sponsor capital allocation priorities.

Strategic Scenario Modelling for Vicuña's Development Path

Because Vicuña is not yet producing, scenario analysis is more useful than linear forecasting.

Scenario 1: Accelerated Execution

In the optimistic case, the joint venture reaches final investment decision by the end of 2026, broadly in line with the public target that has circulated around the project. Under that path:

- Josemaría becomes the anchor build

- construction begins soon after FID

- first copper could arrive after a 4 to 5 year construction period

- copper prices remain supportive, potentially above US$4.50/lb

- the regulatory and fiscal assumptions underpinning RIGI hold through future political cycles

This scenario would place first production roughly around the turn of the decade, assuming no major redesign.

Scenario 2: Delayed but Still Viable Development

This is arguably the more realistic middle case. Here, the project remains fundamentally attractive, but timing extends because district-scale mines rarely move from concept to construction without revisions.

Potential causes include:

- environmental review taking longer than expected

- community engagement timelines expanding

- updated engineering changing plant scope or sequencing

- metallurgical work altering how Josemaría and Filo del Sol should be phased

Under this pathway, FID may slide into 2027 or 2028, pushing first production into the early 2030s.

Scenario 3: Macro and Geopolitical Disruption

The downside case is not that the deposit disappears. It is that capital discipline overrides ambition.

Key downside triggers could include:

- copper falling below US$3.50/lb

- a rise in Argentina's sovereign risk premium

- instability in the practical application of the investment regime

- cross-border logistics or regulatory friction

- shifts in BHP or Lundin Mining portfolio priorities

In this scenario, Vicuña could remain a world-class orebody but an indefinitely deferred project.

The next major ASX story will hit our subscribers first

Infrastructure, Altitude, Water, and Power

A common mistake in mining analysis is to focus on metal inventory and ignore physical execution. High-altitude Andean development is expensive because almost every input must be solved at scale. For Vicuña, enabling infrastructure is not a side issue. It is central to project economics.

Critical Infrastructure Needs

- Road access and haulage corridors for equipment, reagents, fuel, and concentrate movement

- Processing infrastructure sized for district growth, not just initial output

- Power supply, potentially including grid linkage and renewable integration

- Water management systems suitable for an arid mountain environment

- Camp, maintenance, and logistics facilities for remote operations

- Export pathways, including coordination tied to routes through Argentina and potentially Chile

Why Water and Energy Are Strategic Variables

In large copper systems, water and power can be as decisive as grade. Sulphide copper operations typically require substantial grinding and flotation energy, while water balance affects everything from processing stability to environmental approvals.

Investors should watch for future disclosures on:

- source water type and pumping requirements

- recycling rates within the processing circuit

- potential desalination or long-distance transfer assumptions, if any are later proposed

- power intensity per tonne milled

- renewable versus conventional electricity mix

These details often determine whether headline project economics prove resilient or optimistic.

Why the BHP and Lundin Mining Partnership Matters

The ownership structure adds strategic credibility to the Vicuña copper megaproject in Argentina. Fastmarkets has reported that the project targets approximately 395,000 tonnes per year of copper concentrate, underscoring the scale of ambition that BHP and Lundin Mining are aligning behind.

| Partner | Strategic role |

|---|---|

| BHP | Global copper scale, balance sheet depth, development and operating capability |

| Lundin Mining | Regional experience, project continuity, Latin American operating familiarity |

| Vicuña Corp. | Unified management vehicle for district planning and development |

A 50/50 venture can improve alignment on long-duration capital decisions while sharing risk on one of the largest undeveloped copper buildouts in the region. It also reduces the chance that one sponsor alone must carry the full burden of capex escalation. In addition, exploring the broader landscape of copper partnerships between majors and juniors reveals how structurally important such arrangements have become for de-risking district-scale development.

From an investor psychology perspective, BHP's involvement changes how the market frames execution risk. Large diversified miners do not eliminate risk, but they can reshape perceptions around financing access, technical review standards, and development discipline.

Global Copper Supply Pressure and Vicuña's Strategic Relevance

The long-term copper thesis remains rooted in electrification, grid reinforcement, data centre expansion, renewable energy buildout, and electric vehicle adoption. Most major demand outlooks through 2035 to 2040 point to substantial growth, even though exact deficit forecasts differ by source and methodology.

At the same time, the industry faces structural constraints:

- declining grades at mature operations

- longer permitting cycles

- rising capital intensity per tonne of new capacity

- water and community constraints in established producing regions

- limited availability of genuinely large new discoveries

That is why projects like Vicuña attract disproportionate attention. Very few undeveloped districts are large enough to matter at global supply scale. Furthermore, investors exploring copper investment strategies for 2025 and beyond are increasingly weighing district-scale exposure as a core portfolio consideration.

Argentina's Position in the Latin American Copper Race

Chile and Peru remain the region's dominant copper powers. Argentina, by contrast, is better viewed as an emerging pipeline jurisdiction with substantial undeveloped resource potential. If Vicuña advances successfully, it could become a marker for whether Argentina can convert exploration success into long-life operating mines.

Risk and Opportunity Checklist for Investors

Main Risks

- Sovereign risk: policy durability across electoral cycles

- Capex escalation: inflation, altitude, and infrastructure complexity

- Timeline risk: permitting and engineering revisions

- Commodity sensitivity: long-dated exposure to copper price cycles

- Environmental risk: especially water-related approvals and operating constraints

Main Opportunities

- Scale premium: a rare district with generational resource size

- Gold and silver credits: potentially improving project economics materially

- Staged development: flexibility to sequence capital

- High-quality partners: stronger execution credibility than junior-led development

- Macro copper tailwinds: supportive long-range demand case

This article is for informational purposes only and should not be treated as financial advice. Timelines, pricing assumptions, and development scenarios are inherently uncertain. Pre-production mining assets are exposed to permitting, technical, market, and jurisdictional risks that can materially change valuation outcomes.

Frequently Asked Questions About the Vicuña Copper Megaproject in Argentina

What Is the Vicuña Copper Megaproject in Argentina?

It is a district-scale copper-gold-silver development in and around San Juan province and the Chile-Argentina border area, built around the Josemaría and Filo del Sol deposits and managed through Vicuña Corp., a 50/50 joint venture between Lundin Mining and BHP.

How Much Copper Does the Vicuña District Contain?

Reported figures across all resource categories indicate about 38 million tonnes of copper, plus 81 million ounces of gold and 1.4 billion ounces of silver.

What Is RIGI?

RIGI is Argentina's large-investment incentive framework designed to improve fiscal and regulatory predictability for qualifying major projects.

When Could Vicuña Reach Final Investment Decision?

A public target has pointed to end-2026, but investors should treat that as a target rather than a certainty.

What Is the Estimated Capital Cost?

Current figures discussed publicly include about US$7.1 billion for Josemaría Phase 1, a broader staged estimate near US$11 billion, and wider district development concepts in the US$15 billion to US$18 billion range, with US$9.7 billion representing the approved initial investment commitment under the relevant framework.

Who Owns the Project?

The project is held through Vicuña Corp., owned 50/50 by Lundin Mining and BHP.

What Vicuña Signals for Argentina's Mining Future

The broader significance of the Vicuña copper megaproject in Argentina goes beyond one asset. It tests whether Argentina can become a dependable home for the kind of long-life copper developments the market increasingly needs.

If execution holds, Vicuña could strengthen the case that Argentina deserves a larger place in the Latin American copper map. If timelines slip badly or economic assumptions weaken, it may instead reinforce the market's longstanding caution toward frontier-style sovereign exposure.

Either way, Vicuña now sits at the intersection of three powerful forces: the global hunt for new copper supply, the increasing strategic value of district-scale orebodies, and Argentina's effort to convince international capital that large mining investments can be developed on stable terms through the 2030s and beyond.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.