May 14, 2026

The Investment Gap That Policy Cannot Close: Examining Vietnam Scrap Recycling Investment Skepticism

Across Southeast Asia's emerging industrial economies, a familiar pattern repeats itself: governments design increasingly sophisticated incentive frameworks to attract private capital, only to discover that fiscal concessions alone cannot resolve the deeper structural deficiencies that make investors hesitant. Vietnam scrap recycling investment skepticism exemplifies this dynamic with particular clarity. When institutional capital evaluates a new processing hub, it is not primarily concerned with corporate tax rates. It is interrogating collection infrastructure, regulatory predictability, downstream demand certainty, and environmental compliance architecture.

When big ASX news breaks, our subscribers know first

What Institutional Investors Actually Require Before Committing Capital

The evaluation criteria applied by private-sector capital to secondary metals processing investments in developing economies are distinct from those applied to greenfield mining or manufacturing. Recycling infrastructure requires a functioning feedstock ecosystem upstream, industrial-grade processing capability midstream, and reliable offtake absorption downstream. All three must be present simultaneously for investment to be commercially viable.

Vietnam's current position across each of these dimensions reveals the structural mismatch at the heart of its recycling ambitions:

| Investment Factor | Threshold Typically Required | Vietnam's Current Position |

|---|---|---|

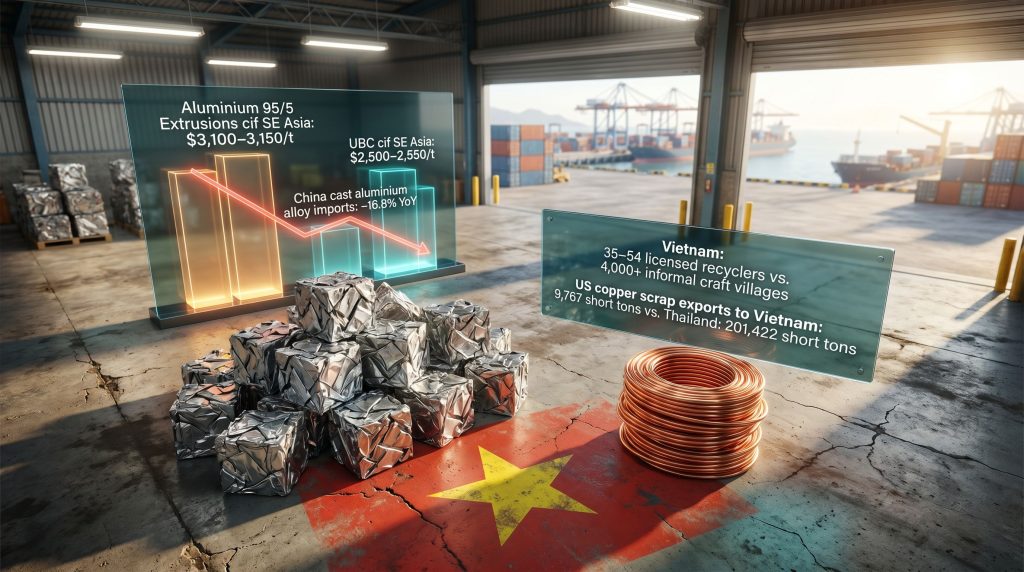

| Formal domestic scrap collection | Over 50% formalized | 35-54 formal companies vs. 4,000+ informal craft villages |

| Downstream demand certainty | Stable, multi-year offtake | Fragmented; reliant on Chinese and Japanese imports |

| Regulatory predictability | Clear, enforced import/export rules | Narrow whitelist; high capex licensing burden |

| Environmental compliance | Industrial-grade standards | Largely informal; craft village-based processing |

| Overall recycling rate | Over 50% for viability | Approximately 33% for plastics; metals similarly underdeveloped |

"The gap between Vietnam's policy ambitions and its structural readiness is not primarily a question of government willingness. It is a fundamental mismatch between incentive design and ground-level operational realities that fiscal measures alone are insufficient to bridge."

How Global Trade Disruption Is Reshaping Secondary Metal Supply Chains

The US-China Tariff Cascade and Its Downstream Effect on Scrap Flows

The escalation of US-China trade tensions has generated systemic disruption across established scrap metal corridors. Tariffs on US goods entering China reached as high as 125% in April 2025, a level that forces fundamental supply chain restructuring rather than marginal sourcing adjustments. These tariff-driven supply chain shifts have compelled Chinese importers of copper and aluminium scrap to rethink procurement geography entirely, accelerating diversification toward European, UK, and Middle Eastern supply sources.

Several compounding pressures are simultaneously reshaping the flow of secondary materials:

- Transhipment routes through Southeast Asia and Japan have grown in strategic importance as Chinese buyers seek tariff-neutral sourcing pathways

- Anticipated EU aluminium scrap export levies in Q2 2026 are compressing European supply options at precisely the moment Chinese buyers are trying to diversify toward them

- Increasingly rigorous port inspections across Thailand, Malaysia, and Japan are narrowing transhipment flexibility that had previously served as a pressure release valve

- Middle Eastern supply disruptions have introduced further unpredictability into global scrap availability calculations

Why Trade Fragmentation Creates Opportunity But Not Necessarily for Vietnam

The assumption that Vietnam is the natural beneficiary of supply chain fragmentation deserves critical scrutiny. Trade rerouting requires not just geographic proximity to disrupted flows, but processing readiness, regulatory clarity, and downstream demand absorption. These are precisely the three dimensions where Vietnam currently underperforms relative to its regional competitors. For context, the broader Southeast Asian scrap trade landscape illustrates just how competitive this regional dynamic has become.

The deterioration of downstream demand signals compounds this vulnerability. Chinese imports of cast aluminium alloys (HS 7601.20) fell approximately 16.8% year-on-year, declining from roughly 1.2 million tonnes in 2024 to approximately 1.0 million tonnes in 2025. This contraction reflects not a temporary demand dip but the proliferation of domestic ADC12 producers within China, which has structurally reduced that country's appetite for imported secondary alloys.

The trajectory of ADC12 aluminium ingot pricing reinforces this concern. Fastmarkets assessed ADC12 (exw dp China) at 22,800-23,100 yuan ($3,338-3,382) per tonne in mid-May 2026, marking a sixth consecutive week of price declines. This sustained compression indicates demand-side weakness rather than supply disruption, a less favourable scenario for processors seeking stable offtake.

What Policy Incentives Has Vietnam Actually Offered to Recycling Investors?

Breaking Down Vietnam's Fiscal and Regulatory Framework for Secondary Metals

Vietnam's incentive architecture for the recycling sector has become meaningfully more sophisticated in the 2025-2026 period, developed within the country's broader commitment to achieving net-zero emissions by 2050.

| Policy Instrument | Details |

|---|---|

| Corporate Income Tax (CIT) for Recyclers | Preferential rate of 10% for 15 years (revised 2025 CIT law) |

| CIT for Energy-Saving Manufacturers | 17% rate for 10 years |

| Standard CIT Rate | 20% for all other investment projects |

| Battery Recycler Support Packages (Decision 21/2025) | Up to three packages per year; each up to 20 billion VND (~$800,000 USD) |

| EPR Framework Overhaul | Decree No. 110/2026/ND-CP, effective May 25, 2026 |

Mandatory Recycling Rates Under the Revised EPR Framework

The updated Extended Producer Responsibility framework establishes minimum processing obligations by material category:

- Aluminium packaging: Minimum 22% recycling rate

- Steel and other metal packaging: Minimum 20% recycling rate

- Rechargeable batteries: Minimum 8-12% recycling rate

- Electrical and electronic equipment: Minimum 3-15% recycling rate

Manufacturers unable to meet these thresholds retain an alternative compliance pathway: contribution to the Vietnam Environment Protection Fund. This flexibility, while pragmatic, also reveals a critical weakness. When financial contributions substitute for actual processing achievement, the framework's capacity to drive measurable infrastructure development is correspondingly diluted.

"The sophistication of Vietnam's policy architecture on paper stands in sharp contrast to the enforcement infrastructure, compliance monitoring mechanisms, and capital support systems required to translate these mandates into bankable investment propositions."

Why Vietnam Scrap Recycling Investment Skepticism Persists Despite Incentives

Barrier One: The Informal Collection System Cannot Support Industrial Processing

Vietnam's domestic scrap collection ecosystem is structurally incompatible with the operational requirements of modern secondary smelters and processing facilities. According to data presented at the China Metal Recycling Association's CMRA 2026 conference held in Hanoi in May 2026, the country's scrap processing landscape is characterised by a profound formalization deficit.

| Metric | Data Point |

|---|---|

| Informal processing hubs | 4,000+ craft villages |

| Formally licensed recycling companies | 35-54 nationally |

| Ratio of informal to formal operations | Approximately 73:1 |

| Import dependency for steelmaking inputs | Over 70% |

| Wastewater generated (Minh Khai hub alone) | 7 million litres daily |

The craft village model, while historically functional for small-scale operations, creates persistent exposure to hazardous materials and dangerous emissions without standardised environmental controls. Reporting from France 24 has highlighted the human cost of this informal processing, documenting the dangerous conditions facing workers in these communities. Modern secondary smelters require traceability documentation, contamination tolerances, and consistent material specifications that informal collection chains are fundamentally unable to provide.

The result is an import dependency that accounts for over 70% of critical steelmaking raw materials, including iron ore, coking coal, and steel scrap, according to 2025 data from the Vietnam Steel Association. Fastmarkets assessed steel scrap (HMS 1&2, 80:20, cfr Vietnam) at $395-405 per tonne on May 8, 2026, a benchmark that reflects Vietnam's sustained and structurally entrenched import reliance.

Barrier Two: Import Licensing Complexity Creates Prohibitive Entry Costs

The paradox at the heart of Vietnam's recycling investment challenge is this: domestic scrap supply is inadequate to feed industrial processors, yet the regulatory framework simultaneously restricts the importation of lower-grade material that could compensate for this domestic shortfall.

Decree No. 08/2022/ND-CP mandates that most imported scrap must be processed into higher value-added goods within Vietnam, with limited conditional licences permitted for temporary import and re-export. Environmental assessment requirements attached to import licensing are extensive. Furthermore, one smelter reported during CMRA 2026 that its licensing requirements included constructing the access road to its own site, an infrastructure cost that would ordinarily be a public provision.

The consequences of this narrow regulatory environment are visible in pricing dynamics. Vietnam maintains an extremely tight approved import whitelist, creating intense competitive pressure for permitted grades:

- Aluminium scrap 95/5 Extrusions (cif Southeast Asia): $3,100-3,150 per tonne as of May 2026, up $1,000-1,050 per tonne year-on-year

- Used beverage cans (cif Southeast Asia): $2,500-2,550 per tonne, up $600-650 per tonne year-on-year

Vietnamese bids for aluminium extrusion have in recent months exceeded even bids from Thailand, a country with significantly larger installed processing capacity. This bidding premium is not a sign of commercial strength; it is a symptom of supply desperation caused by inadequate domestic collection and restrictive import access.

Barrier Three: Downstream Demand Signals Are Weakening

Perhaps the most commercially consequential concern for prospective investors is the deteriorating demand picture from Vietnam's key export markets. Even if processing infrastructure were fully operational, the capacity to place secondary alloy output profitably into end markets is increasingly uncertain.

Japanese aluminium alloy imports tell a similarly discouraging story. Volumes of cast aluminium alloys entering Japan fell to just under 250,000 tonnes in the first quarter of 2026, the lowest Q1 figure recorded since 2013. Despite supply disruptions from the Middle East pushing spot prices to all-time highs in late April 2026, weak automotive sector demand has kept Japanese import activity on a hand-to-mouth basis.

ADC12 ingot (cfr Japan) was assessed at $3,300-3,350 per tonne in mid-May 2026. Electric vehicles being de-prioritised within China's 15th Five-Year Plan further suppresses future ADC12 demand projections. Since EVs typically utilise cast aluminium alloys in battery housings and powertrain assemblies, reduced EV production ambitions represent a structural demand headwind that pricing adjustments alone cannot offset. Meanwhile, the broader China steel market outlook reflects similarly challenging conditions for secondary metals across East Asia.

How Underdeveloped Is Vietnam's Domestic Nonferrous Scrap Market?

Aluminium Recycling: Capacity Exists, But Demand Absorption Remains Uncertain

Vietnam's aluminium scrap processing sector has expanded meaningfully, with industrial zones across northern provinces including Bac Ninh, Hung Yen, and Nam Dinh, and southern hubs in Dong Nai, Long An, and Ba Ria-Vung Tau hosting a growing concentration of secondary processing operations.

| Metric | Estimated Figure |

|---|---|

| Total aluminium scrap processing capacity | ~700,000 tonnes per year |

| Domestic ADC12 consumption | ~120,000 tonnes per year |

| Domestic ADC12 production coverage | ~60,000 tonnes per year |

| Residual demand gap (import-dependent) | ~60,000 tonnes per year |

This 60,000-tonne residual demand gap has attracted aggressive competition from Chinese exporters alongside regional suppliers from Thailand and Malaysia quoting CIF Vietnam prices as high as $3,380 per tonne in late May 2026. The competitive intensity for this relatively modest demand pool further illustrates why Vietnam's market does not yet represent a compelling destination for large-scale processing investment.

Secondary Copper: Even Further Behind the Development Curve

Vietnam's secondary copper processing sector lags considerably behind its aluminium counterpart. Copper scrap handling is concentrated among medium-sized rod and ingot producers serving electrical and construction end-markets, with sourcing skewed toward domestic material due to tighter import licensing for copper scrap grades.

The scale gap relative to regional competitors is stark. Vietnam received just 9,767 short tons of US copper scrap exports (HS 7404) in 2025, representing less than 1% of total US copper scrap export volumes. By comparison, Thailand received 201,422 short tons of US copper scrap in 2025, nearly double its 2024 intake of 105,616 short tons.

"This volume differential is not simply a reflection of current processing capacity. It reflects the cumulative effect of years of regulatory environment, infrastructure development, and end-market relationships that Thailand has built and Vietnam has not."

The next major ASX story will hit our subscribers first

Vietnam vs. Regional Competitors: Where Does Investment Capital Actually Flow?

Comparative Analysis Across Southeast Asia and the Middle East

| Evaluation Criterion | Vietnam | Thailand | Middle East (UAE/Saudi Arabia) |

|---|---|---|---|

| Processing infrastructure maturity | Early-stage; craft village dominant | Advanced; major OEM presence | Rapidly developing; port upgrades underway |

| Regulatory environment | Complex; narrow import whitelist | More permissive; established frameworks | Investment-friendly; strategic hub positioning |

| Perceived corruption risk | Moderate | Lower (market participant assessment) | Varies by jurisdiction |

| Global manufacturer presence | Limited | Extensive | Growing |

| Long-term demand creation | Policy-dependent | Demand-driven by existing industry | Active demand engineering strategy |

| Transhipment hub potential | Constrained by port capacity | Established | Explicitly strategic over 10-year horizon |

Why Thailand Maintains Its Competitive Advantage

Market participants at CMRA 2026 consistently highlighted Thailand's structural advantages. The Thai secondary metals sector is described as considerably more advanced than comparable markets in the region, benefiting from a dense ecosystem of global automotive manufacturers and metal fabricators that generate consistent and predictable scrap demand. The perceived lower corruption risk relative to regional peers was also cited as a commercial differentiator by major scrap suppliers.

The Middle East's Emerging Role as a Global Scrap Hub

Muzzammil Haji Amin Gadawala, vice president and executive board member of the Bureau of Middle East Recycling (BMR), articulated the strategic positioning of the Middle East at CMRA 2026: the region is not waiting passively for scrap trade flows to arrive. In addition, Saudi Arabia's industrial strategy demonstrates a broader regional commitment to actively constructing the infrastructure and industrial demand base needed to become a primary East-West connector for secondary metals over the next decade.

This distinction is commercially significant. Vietnam is attempting to attract demand through fiscal incentives. The Middle East, however, is engineering demand through direct industrial investment and infrastructure commitment, a fundamentally different and historically more effective strategy.

Fringe Routes: Bangladesh and Pakistan

Some Chinese traders have explored transhipment through South Asian ports including Bangladesh and Pakistan as alternatives to increasingly scrutinised Southeast Asian routes. However, persistent cashflow constraints and logistical limitations at these ports mean such corridors remain peripheral to mainstream scrap trade flows, representing contingency thinking rather than commercially viable alternatives.

What Would It Actually Take for Vietnam to Become a Credible Recycling Hub?

Structural Transformations Required to Convert Policy Ambition Into Investment Reality

For Vietnam to meaningfully close the gap between stated recycling ambitions and private-sector confidence, several interconnected transformations would need to occur simultaneously rather than sequentially:

- Formalization of domestic scrap collection: Transitioning from 4,000+ informal craft villages toward regulated processing clusters with standardised environmental controls and material quality assurance protocols

- Regulatory liberalisation on scrap imports: Expanding the approved import whitelist to reduce competitive distortion and improve raw material access for formal processors

- Downstream demand development: Stimulating domestic automotive, construction, and electronics manufacturing to create reliable and consistent offtake for secondary metals output

- Infrastructure investment frameworks: Resolving the capex burden on investors, including basic site infrastructure such as access roads that currently falls entirely on private operators

- EPR enforcement credibility: Demonstrating that Decree No. 110/2026 translates into measurable recycling rate improvements rather than compliance-by-fund-contribution

- Pollution liability clarity: Establishing legal standards that protect formal investors from legacy environmental liabilities associated with informal predecessor operations

Consequently, investment in critical minerals supply chains across other regions provides a useful benchmark for what credible policy-backed industrial transformation actually requires in practice.

"If Vietnam successfully formalises even 30% of its informal scrap collection network and expands its import whitelist within three years, it could plausibly position itself as a secondary processing node for Southeast Asian scrap flows. However, under current conditions, it would still trail Thailand significantly in total processing capacity, market maturity, and end-market connectivity."

This article is intended for informational purposes only and does not constitute investment advice. Commodity price assessments and trade flow data cited are sourced from Fastmarkets reporting as of May 2026. Market conditions, regulatory frameworks, and pricing benchmarks are subject to change. Forecasts and scenario projections represent analytical estimates based on available data and should not be relied upon as predictions of future outcomes.

Frequently Asked Questions: Vietnam Scrap Recycling Investment

Why are investors skeptical about Vietnam's scrap recycling sector?

Investors point to a combination of structural barriers: an informal domestic collection system dominated by over 4,000 craft villages that cannot support industrial-scale processing, restrictive import licensing that limits raw material access for formal processors, unexpectedly high capital expenditure requirements, weak downstream demand from key export markets in China and Japan, and insufficient enforcement mechanisms for environmental regulations. Furthermore, Fastmarkets reporting on investor sentiment confirms that fiscal incentives including preferential corporate income tax rates exist but are insufficient to offset these compounding operational and regulatory risks.

What are Vietnam's current recycling rates for metals?

Vietnam's overall domestic collection capacity for metals remains severely underdeveloped, with over 70% of critical steelmaking inputs sourced through imports according to 2025 data from the Vietnam Steel Association. Aluminium processing capacity stands at approximately 700,000 tonnes per year, but domestic ADC12 consumption is only around 120,000 tonnes annually, with domestic production covering roughly half of that. The secondary copper sector is more constrained still, receiving less than 1% of total US copper scrap export volumes in 2025.

How does Vietnam compare to Thailand as a scrap processing destination?

Thailand maintains a significantly more advanced secondary metals sector, with established processing infrastructure, a larger installed base of global manufacturing clients, and a more permissive regulatory environment. Vietnam received 9,767 short tons of US copper scrap in 2025, compared to Thailand's 201,422 short tons, illustrating the substantial scale differential between the two markets at their current stages of development.

What is Vietnam's Extended Producer Responsibility framework?

Vietnam's revised EPR framework under Decree No. 110/2026/ND-CP, effective May 25, 2026, establishes mandatory minimum recycling rates by material: 22% for aluminium packaging, 20% for steel packaging, 8-12% for rechargeable batteries, and 3-15% for electrical and electronic equipment. Manufacturers unable to meet these targets may contribute to the Vietnam Environment Protection Fund as an alternative compliance pathway.

Where are scrap recycling investments flowing if not to Vietnam?

Thailand remains the preferred destination for secondary metals investment in Southeast Asia among active market participants. The Middle East, particularly the UAE and Saudi Arabia, is emerging as a strategically important hub over a 10-year horizon, driven by active port infrastructure investment and deliberate industrial demand creation rather than passive incentive-offering. Fringe transhipment routes through Bangladesh and Pakistan remain logistically and financially constrained.

What scrap metal prices are relevant to Vietnam's recycling market in 2026?

Key Fastmarkets benchmark assessments as of May 2026 include: steel scrap HMS 1&2 (cfr Vietnam) at $395-405 per tonne; aluminium scrap 95/5 Extrusions (cif Southeast Asia) at $3,100-3,150 per tonne, up over $1,000 year-on-year; used beverage cans (cif Southeast Asia) at $2,500-2,550 per tonne; ADC12 aluminium ingot (cfr Japan) at $3,300-3,350 per tonne; and ADC12 (exw dp China) at 22,800-23,100 yuan ($3,338-3,382) per tonne amid six consecutive weeks of price decline.

Want to Stay Ahead of the Next Major Resource Discovery Before the Broader Market Catches On?

While Vietnam's scrap recycling landscape illustrates how quickly commodity supply chains can shift, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly notifying subscribers of significant mineral discoveries with actionable insights suited to both traders and long-term investors — explore historic discovery returns on Discovery Alert's discoveries page and begin your 14-day free trial to secure a market-leading edge.