July 14, 2026

The Hidden Pricing Lever That Every ASX Resource Investor Should Understand

Most investors focus on production volumes, capital expenditure schedules, and management quality when evaluating mining stocks. Yet one of the most powerful forces shaping earnings outcomes for ASX resource companies operates entirely outside the mine gate. Understanding the relationship between the weak US dollar and ASX resource stocks is not optional for serious resource investors in 2026 — it is foundational.

The US dollar's role as the universal pricing currency for industrial commodities creates a structural linkage that transmits greenback movements directly into the revenue lines of every miner on the planet. For Australian miners reporting in AUD, this transmission mechanism is both an opportunity and a risk — and right now, the signals are pointing firmly in one direction.

When big ASX news breaks, our subscribers know first

The Macro Mechanism: How USD Movements Ripple Into Commodity Markets

Because virtually every major commodity — iron ore, copper, aluminium, lithium, and crude oil — is priced in US dollars on international markets, the strength or weakness of the greenback functions as an invisible tariff or subsidy on global commodity trade. When the dollar depreciates, buyers transacting in other currencies receive an effective cost reduction on every tonne purchased without any change in the underlying commodity's listed price.

This mechanics creates a self-reinforcing feedback loop. Lower effective costs stimulate purchasing activity, which tightens supply-demand balances and pushes prices higher in USD terms. For producers whose costs are anchored in non-USD currencies, this combination of volume uplift and price appreciation can produce a disproportionate earnings response.

The historical record supports this pattern clearly. The commodity supercycle of the mid-2000s coincided with a sustained period of broad USD weakness. Furthermore, the post-2020 commodity rally was similarly amplified by a declining dollar index during the early phases of that cycle.

What Is Driving the 2026 USD Decline?

The current episode of dollar weakness is being driven by a convergence of structural and cyclical pressures that analysts describe as unusually broad-based:

| Driver | Description | Market Impact |

|---|---|---|

| US fiscal sustainability concerns | Expanding deficit trajectory and debt ceiling uncertainty | Reduced confidence in USD as reserve currency |

| Trade policy volatility | Tariff escalation and bilateral trade disruptions | Capital reallocation away from USD-denominated assets |

| Federal Reserve policy caution | Slower-than-expected rate normalisation cycle | Compressed interest rate differential versus peer currencies |

| US Dollar Index decline | Down more than 8% since January 2026 | Lowest reading since 2022 |

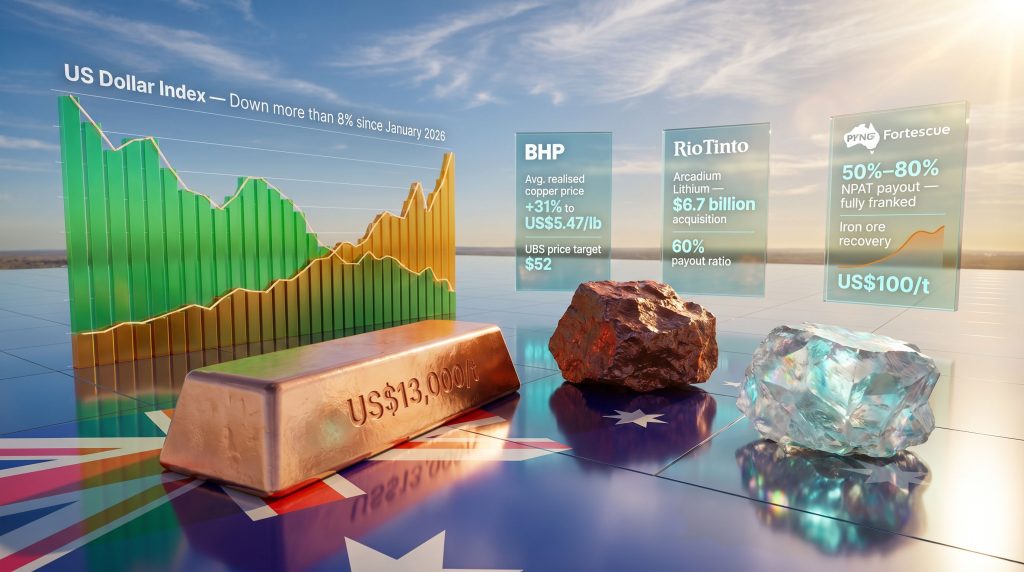

The US Dollar Index (DXY), which measures the greenback against a basket of six major currencies including the euro, yen, and British pound, has declined by more than 8% since the start of 2026, reaching its lowest point since 2022. This is not a minor fluctuation — it represents a meaningful repricing of the dollar's relative value with direct implications for commodity prices and mining earnings.

Why Australian Miners Face a Dual Currency Effect — and Why It Usually Resolves Positively

A natural counterforce applies to Australian miners operating in this environment. When the USD weakens, the AUD typically appreciates in relative terms, because the Australian dollar tends to move inversely to the greenback given Australia's commodity export profile. This appreciation partially compresses the AUD revenue benefit that miners would otherwise receive from higher USD commodity prices.

However, the historical pattern consistently shows that the net effect is positive for ASX miners when commodity demand fundamentals are intact. The reasoning is straightforward: a demand-driven commodity rally amplified by USD weakness generates a larger absolute price increase in USD terms than the offsetting AUD appreciation erodes in translation.

The distinction between a demand-driven commodity rally and a purely currency-driven price move matters enormously here. In the former scenario, real purchasing activity is increasing, inventories are tightening, and the price signal is reinforced by physical market dynamics. According to Fairmont Equities, a lower USD generally supports Australian resource stocks through precisely this kind of earnings amplification effect.

The Four-Variable Earnings Framework for ASX Resource Investors

Accurately estimating the earnings impact of a weak USD on an ASX miner requires simultaneous analysis of four compounding variables. Investors who focus on currency alone risk misreading the picture entirely.

- Commodity price change in USD terms — the gross revenue movement per unit of production

- AUD/USD appreciation magnitude — the degree of translation offset when converting USD revenue to AUD

- Unhedged production volume exposed to spot pricing — the proportion of output that actually captures spot market movements versus locked-in forward contracts

- Operating cost base structure — Australian producers carry the majority of their cost base in AUD, meaning a rising AUD does not proportionally increase costs even as it partially reduces revenues

This cost-base asymmetry is a frequently overlooked advantage for Australian miners. Labour, energy, maintenance, and overhead costs are predominantly AUD-denominated. Consequently, the net margin can actually expand in a USD-weak, AUD-strong environment when commodity prices are rising fast enough.

Copper: Structural Demand Meets the Weak Dollar Amplifier

Copper's price trajectory in 2026 illustrates the compounding dynamics at play with unusual clarity. The metal has surged above US$13,000 per tonne on the London Metal Exchange, reflecting both the USD weakness tailwind and genuinely unprecedented structural demand growth. The ongoing copper supply crunch compounds these pricing pressures further.

Three forces are simultaneously pulling copper demand higher:

- AI data centre construction requires substantially more copper wiring per square metre than conventional commercial buildings due to high-density power distribution requirements

- Electric vehicle manufacturing uses roughly three to four times more copper per vehicle than an equivalent internal combustion engine platform

- Grid infrastructure expansion across North America, Europe, and Asia requires enormous conductor volumes to connect renewable generation to consumption centres

The supply side provides little relief. Copper's long project development timelines, typically 12 to 20 years from discovery to production, mean the industry cannot respond rapidly to demand signals.

The combination of inelastic near-term supply, surging structural demand from electrification, and a weakening USD creates conditions that historically produce sustained rather than transient commodity price elevation.

BHP's March quarter update provided a concrete illustration of this dynamic translating into earnings. The company's average realised copper price rose 31% to US$5.47 per pound, a direct consequence of both the structural rally in the underlying commodity and the currency amplification effect. UBS maintained a hold rating on BHP with a price target of $52, acknowledging the company's fundamental quality while flagging near-term iron ore price uncertainty as a balancing consideration.

Iron Ore: Chinese Purchasing Economics and the USD Transmission

Iron ore's recovery above US$100 per tonne reflects a specific and important dynamic in the China-Australia trade relationship. The China steel and iron ore market is particularly sensitive to USD movements, as Chinese steel mills purchase iron ore in USD-denominated contracts but operate in a yuan-denominated cost environment.

When the USD weakens, their effective cost per tonne of imported iron ore declines in yuan terms without any movement in the listed USD price. This creates a purchasing incentive that operates independently of steel demand conditions. Current inventory depletion at major Chinese steel mills has reinforced this dynamic, supporting a restocking cycle that is complementing the currency tailwind.

The supply picture adds further support. Production discipline among major iron ore exporters has sustained price floors even during periods when Chinese demand moderated. The concentrated nature of the seaborne iron ore supply chain means that marginal supply responses are slow and limited.

The Risk Scenario That Iron Ore Investors Must Monitor

The Chinese property sector remains the critical variable. A deeper-than-expected contraction in residential construction activity could reduce demand sufficiently to overwhelm both the currency tailwind and the supply discipline. The 2015-2016 episode, when iron ore prices collapsed despite a broadly stable USD environment, demonstrates that commodity fundamentals can override currency effects under conditions of genuine demand destruction.

Lithium: A Recovery Cycle With a USD Revenue Base

Lithium's situation in 2026 differs from copper and iron ore in one important structural respect: the market is recovering from an extended and severe price correction. The lithium market downturn saw prices fall dramatically through 2023 and 2024 as a wave of new supply overwhelmed demand growth.

The recovery underway in 2026 reflects a combination of supply rationalisation, as high-cost producers curtailed operations, and genuine demand acceleration as EV adoption rates in key markets continue to compound. Because the majority of lithium revenue is denominated in USD, AUD-reporting miners are direct beneficiaries of greenback weakness in the current recovery phase.

Rio Tinto's $6.7 billion acquisition of Arcadium Lithium, completed in early 2026, represents a strategic commitment to the lithium recovery cycle at precisely the inflection point where the currency environment has become maximally supportive.

The next major ASX story will hit our subscribers first

Comparing BHP, Rio Tinto, and Fortescue: Earnings Leverage and Dividend Profiles

The three largest ASX-listed miners each respond to the weak US dollar and ASX resource stocks theme in distinct ways, shaped by their commodity mix, hedging strategies, and capital return frameworks.

| Metric | BHP | Rio Tinto | Fortescue |

|---|---|---|---|

| Primary commodity exposure | Iron ore + Copper | Iron ore + Copper + Aluminium + Lithium | Iron ore (dominant) |

| USD weakness earnings sensitivity | High (copper leverage) | Very high (diversified USD commodities) | Very high (concentrated iron ore) |

| Dividend payout policy | Variable progressive framework | 60% of underlying earnings | 50%–80% of NPAT |

| Key 2026 strategic theme | Copper growth pipeline | Arcadium lithium integration | Green energy transition via Fortescue Energy |

| Dividend payment structure | Semi-annual | Semi-annual | Semi-annual, fully franked |

BHP benefits from the copper-electrification nexus more directly than its peers, with a growing project pipeline positioning the company to capture multi-year structural demand growth. The compounding effect of rising structural demand, supply constraints, and USD weakness creates conditions for a potentially durable earnings uplift in the copper division rather than a cyclical spike.

Rio Tinto offers a portfolio effect that smooths earnings volatility across the commodity cycle. Its diversification across four major USD-priced commodities means that weakness in one market is buffered by strength in others. The Arcadium integration adds lithium earnings that will begin contributing meaningfully to the revenue base through FY2026 and FY2027.

Fortescue represents the highest-conviction, most concentrated leveraged play on the weak USD and iron ore recovery combination. The fully franked dividend policy, paying out between 50% and 80% of NPAT, means the August 2026 full-year result will likely deliver a meaningful income event for shareholders if current conditions persist.

The Risk Matrix: When Currency Tailwinds Are Not Enough

A weakening USD is a powerful supportive factor for ASX resource stocks, but it is not a standalone buy signal. Investors who treat currency weakness as a sufficient condition for commodity exposure without assessing demand fundamentals are making a category error with potentially costly consequences.

Four risk factors have the capacity to neutralise or reverse the current tailwind:

Risk Factor 1: Chinese demand deterioration

- A contraction in Chinese steel production or a deepening of property sector weakness could reduce iron ore demand irrespective of currency dynamics

- The 2015-2016 iron ore collapse occurred in a period of broadly stable USD, demonstrating that demand destruction overrides currency effects

Risk Factor 2: Global growth deceleration

- A US recession or synchronised global slowdown would suppress industrial commodity demand across copper, aluminium, and iron ore simultaneously

- USD weakness driven by recession fears is categorically different from USD weakness driven by fiscal or monetary policy factors

Risk Factor 3: AUD appreciation outpacing commodity gains

- If the AUD strengthens faster in percentage terms than commodity prices rise in USD terms, the net AUD revenue impact for Australian miners could be neutral or marginally negative

- Monitoring the AUD/USD rate against commodity price movements simultaneously provides a real-time signal of net earnings direction

Risk Factor 4: Hedging program structures

- Miners with significant forward sales programs may not capture the full benefit of spot commodity price rallies during hedge book runoff periods

- Quarterly production reports and half-year financial disclosures typically contain hedging exposure data that investors should review before assuming full leverage to spot pricing

A Practical Framework for ASX Investors Navigating the Weak USD Theme

Translating macro understanding into portfolio positioning requires a structured approach:

Step 1: Establish commodity conviction by demand durability

- Copper holds the highest structural demand visibility given electrification and AI infrastructure commitments spanning decades

- Iron ore carries more cyclical sensitivity but is currently supported by restocking dynamics and supply discipline

- Lithium is a recovery-phase story with higher volatility but a compelling longer-duration demand outlook

- Gold prices and mining equities respond to USD weakness as a monetary alternative asset, relevant for precious metals-focused resource exposure

Step 2: Assess actual earnings leverage by reviewing hedging disclosures

- Unhedged production volumes determine the real earnings sensitivity to spot commodity prices

- Most major ASX miners disclose hedging positions in quarterly and semi-annual reports

Step 3: Align dividend policy with income objectives

- Fully franked distributions from Australian iron ore producers carry additional after-tax value for resident investors through the franking credit system

- Fixed payout ratios (such as Rio's 60%) provide earnings-linked predictability, while variable frameworks (such as Fortescue's 50%-80% range) can deliver higher payouts during commodity upcycles

Step 4: Monitor the four macro indicators continuously

- US Dollar Index (DXY) trajectory and rate of change

- AUD/USD exchange rate movements relative to commodity price shifts

- Chinese steel mill inventory levels and production activity data

- US Federal Reserve forward guidance on interest rate policy direction

Frequently Asked Questions: Weak US Dollar and ASX Resource Stocks

Does a weak US dollar automatically push commodity prices higher?

No. USD weakness is a supportive condition, not a deterministic one. Supply constraints, global growth expectations, and speculative positioning all exert independent influence on commodity prices. The current environment is constructive precisely because demand fundamentals are reinforcing the currency tailwind rather than working against it.

Which ASX resource stocks benefit most from a falling US dollar?

Miners with large unhedged exposure to USD-priced commodities capture the greatest benefit. Among major names, those with significant copper, iron ore, and lithium revenue streams carry the highest sensitivity. Company-level hedging disclosures are essential for calibrating the actual earnings exposure accurately.

How does AUD appreciation offset the benefit of higher commodity prices for Australian miners?

Australian producers earn revenue in USD but carry operating costs predominantly in AUD. AUD appreciation reduces the revenue conversion benefit but does not proportionally increase costs, creating a partial rather than complete offset. The net impact depends on the relative magnitude of commodity price gains versus AUD appreciation.

What is the US Dollar Index and why does it matter for resource stocks?

The DXY measures the USD against a basket of six major currencies. A declining DXY signals broad-based dollar weakness, which tends to stimulate commodity demand from non-USD buyers, support higher prices in USD terms, and amplify AUD earnings outcomes for Australian miners.

Can iron ore prices remain elevated if Chinese demand softens?

Supply-side discipline from major exporters can support price floors during periods of softer demand. However, a sustained price recovery typically requires both supply restraint and genuine demand recovery working simultaneously. Single-factor support is generally insufficient for durable price elevation.

Key Takeaways for 2026 and the August Reporting Season

The confluence of forces operating in favour of ASX resource stocks in 2026 is unusually aligned across multiple dimensions simultaneously:

- The US Dollar Index has declined more than 8% since January 2026, reaching multi-year lows and creating a broad-based commodity price tailwind across virtually every material that Australian miners produce

- Copper trading above US$13,000 per tonne reflects both structural demand acceleration from electrification and AI infrastructure, and the currency amplification effect that a weak dollar provides

- Iron ore recovering above US$100 per tonne is supported by Chinese steel mill restocking economics that become more attractive when the USD weakens, as yuan-denominated purchasing costs decline

- BHP, Rio Tinto, and Fortescue each offer distinct exposure profiles within the weak USD theme, differentiated by commodity diversification, hedging posture, and dividend policy structure

- Income-focused investors should pay particular attention to the August 2026 reporting season, when the commodity and currency tailwinds of the first half of the year are expected to crystallise into declared dividend distributions

The environment for the weak US dollar and ASX resource stocks thesis is as constructive as it has been for several years. However, disciplined investors will hold this constructive view alongside a clear-eyed assessment of the risk factors that could change the picture, most importantly the trajectory of Chinese industrial demand and the pace of AUD appreciation relative to commodity price gains.

This article contains general financial information only and does not constitute personal financial advice. Commodity prices, exchange rates, and company earnings are subject to change and past performance is not indicative of future outcomes. Investors should consider their personal circumstances and consult a licensed financial adviser before making investment decisions.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

While understanding the weak USD and its impact on ASX resource stocks provides a crucial macro framework, the real edge comes from acting on significant mineral discoveries the moment they are announced — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on high-potential discoveries across copper, lithium, iron ore, and more than 30 other commodities, so investors can position themselves ahead of the broader market. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to experience how rapid, actionable insights can complement your resource investing strategy.