June 25, 2026

Why West Africa's Gold Reserve Rankings Tell Only Part of the Story

Every few years, a government official somewhere in West Africa makes a bold claim about their country's gold wealth. In mid-2026, Guinea's President Mamadi Doumbouya asserted during a meeting with domestic gold sector stakeholders that his country holds the second-largest gold reserves in West Africa. The statement made headlines across the region. It also exposed something more fundamental about how West Africa gold reserves ranking works — and why such rankings so frequently mislead investors, policymakers, and the public alike.

The problem is not simply one of competing statistics. It is architectural. The very concept of a gold reserve means different things depending on who is using the term, which data source they are drawing from, and how recently that data was collected.

When big ASX news breaks, our subscribers know first

Three Very Different Things Called Gold Reserves

Understanding any West Africa gold reserves ranking requires first untangling a terminology problem that distorts almost every regional comparison.

Geological or mineable reserves refer specifically to the portion of a deposit that can be extracted economically, based on detailed technical work including ore grade assessment, production cost modelling, and feasibility studies. This is the figure that mining companies publish in their annual reports and that agencies such as the U.S. Geological Survey (USGS) attempt to aggregate at the national level.

Mineral resources form a broader category. These are identified gold deposits where geological evidence confirms the presence of gold, but where economic viability has not yet been fully demonstrated. Resources are frequently cited during exploration-stage projects and are commonly larger than reserve figures for the same deposit.

Central bank monetary gold is an entirely separate metric. These are gold bars held by governments as part of their foreign exchange reserves. Nations such as Algeria, which holds approximately 174 tonnes in central bank gold, and South Africa, with around 125 tonnes, frequently top lists of Africa's largest gold reserve holders — however, these gold reserve rankings refer entirely to monetary assets, not underground geology.

A country can hold vast central bank gold assets while sitting atop a relatively modest geological endowment, and vice versa. Confusing these categories produces rankings that are technically accurate but practically meaningless for investment or policy purposes.

The second layer of complexity involves data consistency. Not all West African governments commission comprehensive national geological surveys or publish standardised reserve estimates. Some national figures draw on colonial-era geological archives. Others rely on company disclosures that only capture operating mines.

International bodies like the USGS compile and standardise what data is available, but in a relatively underexplored region, the published numbers represent a floor of known endowment rather than a ceiling of total potential. As gold prices remain elevated, previously uneconomic deposits are continuously converted into classifiable reserves, meaning the rankings are not static.

West Africa's Gold Endowment in Global Context

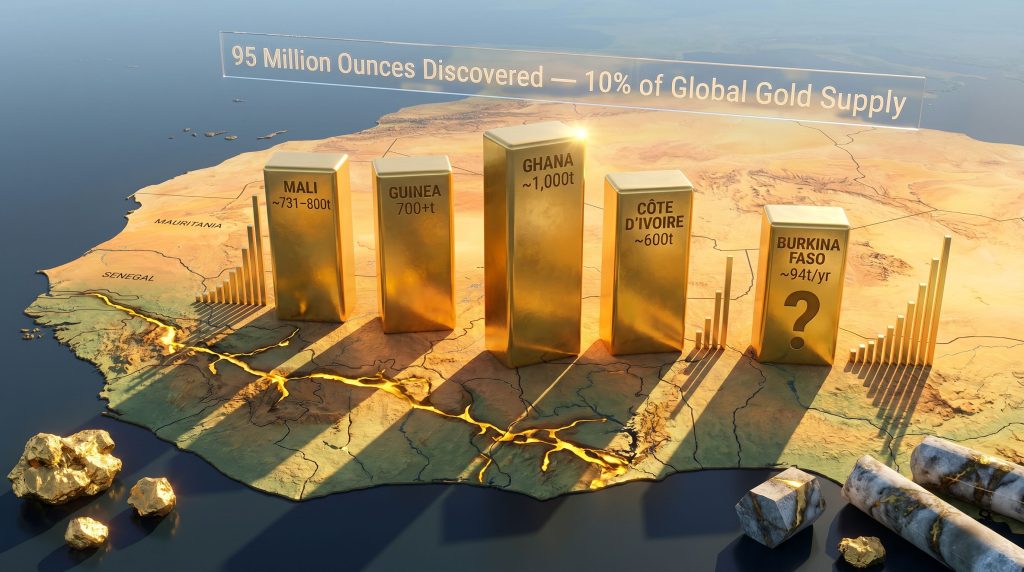

Despite the data limitations, the scale of West Africa's collective gold endowment is not in dispute. The region contributes approximately 10% of global gold supply, a figure that understates its geological significance because large portions of the region remain inadequately explored. Furthermore, gold exploration trends continue to evolve rapidly across the continent, adding further complexity to any static ranking.

Over the two decades to the mid-2020s, West Africa yielded an estimated 95 million ounces of newly discovered gold — substantially outpacing both Canada (approximately 61 million ounces) and Australia (approximately 29 million ounces) over the same period. Ghana and Mali together account for more than 57% of the region's combined historical production and geological resources.

Why Does So Much Gold Exist in West Africa?

The geological explanation for this concentration lies in the West African Craton, a Precambrian continental shield that underpins the region. Within it, the Birimian Greenstone Belt — a formation of ancient volcanic and sedimentary rocks deposited roughly 2.1 to 2.2 billion years ago — hosts the overwhelming majority of the region's gold mineralisation.

According to The Conversation, this Belt extends across Ghana, Mali, Burkina Faso, Côte d'Ivoire, Guinea, Senegal, and Mauritania. Its structural continuity explains why gold discoveries in one jurisdiction so consistently signal prospectivity in neighbouring countries. For exploration geologists, the Belt is effectively a single mineralised system divided by political borders rather than geological ones.

West Africa Gold Reserves Ranking by Country: 2026 Assessment

The table below summarises the current regional picture, combining USGS data with available company-level and government disclosures.

| Rank | Country | Est. Geological Reserves | Annual Production (approx.) | Data Confidence |

|---|---|---|---|---|

| 1 | Ghana | ~1,000 metric tonnes | ~90 metric tonnes/year | High |

| 2 | Mali | ~731–800 metric tonnes | ~67.7 metric tonnes/year | Moderate |

| 3 | Guinea | ~700+ metric tonnes | Growing rapidly | Moderate-Low |

| 4 | Côte d'Ivoire | ~600 metric tonnes | Growing | Moderate |

| 5 | Burkina Faso | Unavailable (USGS) | ~94+ metric tonnes (2025) | Low |

Rank 1 — Ghana: The Region's Undisputed Leader

Ghana's position at the top of any West Africa gold reserves ranking is the one figure in the regional dataset that carries genuine statistical confidence. USGS data places Ghana's geological gold reserves at approximately 1,000 metric tonnes, the highest in West Africa by a considerable margin.

That confidence derives from the depth and maturity of Ghana's mining sector. Decades of systematic exploration, feasibility work, and production by major international operators have produced a reserve base that is better documented than any comparable jurisdiction in the region. Active large-scale producers include Newmont, Gold Fields, AngloGold Ashanti, Perseus Mining, and Asante Gold.

Both industrial operations and formalised artisanal production contribute to Ghana's annual output of approximately 90 metric tonnes, making it Africa's largest gold producer and among the world's top six. The alignment between Ghana's reserve base and its production profile is itself a signal of reserve quality. Sustained annual output at this scale requires consistent resource-to-reserve conversion — a process that demands continued exploration investment, which Ghana has historically attracted in greater volume than any other West African nation.

Rank 2 — Mali: A Contested Position Under Structural Pressure

Mali has long occupied second place in regional gold reserve rankings, and by the numbers available, it still does. USGS 2025 data maintains a national reserve estimate of approximately 800 metric tonnes. However, figures submitted by Mali's Ministry of Mines to Reuters in 2024 revealed that commercially classified company-held reserves had declined from 881.7 metric tonnes in 2022 to 731 metric tonnes in 2024 — a reduction of roughly 17% over two years.

This divergence between national geological estimates and company-reported figures reflects a structural issue rather than a simple data discrepancy. Commercially classified reserves decline when mining companies decelerate or suspend exploration, because the conversion pipeline from resource to reserve dries up. In Mali's case, that slowdown coincides with a period of heightened tension between the government and operating companies over revenue-sharing frameworks and royalty structures.

The practical consequence is that Mali's second-place standing, while likely still accurate at the current snapshot, is directionally weakening. At the lower company-reported estimate of 731 tonnes, Guinea's official claim of more than 700 tonnes places the two countries within margin-of-error range of each other — a situation that would have seemed unlikely a decade ago.

Rank 3 — Guinea: Ambition Ahead of Verification

Guinea's government has placed its national gold reserves at more than 700 metric tonnes, concentrated in the prefectures of Siguiri, Kouroussa, Mandiana, Dinguiraye, and Kankan. At face value, this positions Guinea as a legitimate challenger to Mali's second-place status. The key qualification is data confidence, which remains lower for Guinea than for either Ghana or Mali.

Industrial production is anchored by AngloGold Ashanti's Siguiri operation, one of the region's larger producing assets. Among development-stage projects, Predictive Discovery's Bankan project has attracted considerable attention, with reported mineral resources of approximately 5.38 million ounces. A growing pipeline of new gold discoveries suggests Guinea's official reserve figures carry material upside risk — meaning the actual endowment may prove larger as technical studies mature and resource-to-reserve conversion progresses. What Guinea lacks relative to Ghana and Mali is a long track record of independent geological verification across its entire endowment.

Rank 4 — Côte d'Ivoire: The Region's Fastest-Climbing Gold Province

Côte d'Ivoire sits fourth in the current ranking with official estimates of approximately 600 metric tonnes. The more interesting story, however, is the trajectory rather than the current position. The country is experiencing an active discovery wave, with multiple deposits reporting mineral resources exceeding 100 metric tonnes of gold individually.

Key projects advancing through the development pipeline include:

- Koné, with reported mineral resources of approximately 4.01 million ounces

- Boundiali, another large-scale deposit attracting significant exploration capital

- Doropo, a project in the northeast of the country with a substantial resource base

Each of these sits firmly within the Birimian Greenstone Belt, sharing the same host geology as Ghana's most prolific mining districts. As these projects advance and as cut-off grades are reassessed at current gold prices, upward revisions to Côte d'Ivoire's classified reserve figures become increasingly probable.

Rank 5 — Burkina Faso: Prolific Producer, Invisible Reserve Base

Burkina Faso presents the most unusual case in the regional picture. It is one of the region's most active producers, with national output surpassing 94 metric tonnes in 2025. Yet the USGS 2025 dataset lists the country's national reserve figure as simply unavailable.

This is not evidence of an absence of gold. It is evidence of an absence of comprehensive national geological assessment. Company-level data fills in part of the picture: West African Resources reported combined reserves of approximately 7 million ounces (~218 metric tonnes) across its Sanbrado, Kiaka, and Toega assets in 2025. According to Mining Review Africa, aggregating equivalent figures from all major operators would provide a larger but still incomplete total, since it would exclude artisanal sites, undeveloped deposits, and early-stage exploration ground.

Burkina Faso's security environment in recent years has complicated both operations and the systematic geological survey work required to generate national reserve estimates. The data gap is real, but it likely masks a gold endowment that, if properly quantified, could materially alter the regional ranking.

What Continuously Reshapes the Regional Hierarchy

The West Africa gold reserves ranking is not a fixed table. Three primary forces drive ongoing changes:

-

Gold price movements: When gold prices rise, the economic cut-off grade for mining decreases. Deposits that were previously marginal become economically viable, and their resources can be reclassified as reserves. This mechanism can shift a country's published reserve figure substantially without any new geological discovery occurring.

-

Exploration investment cycles: Countries that attract sustained exploration capital — including drill programmes, airborne geophysical surveys, geochemical sampling, and feasibility studies — systematically convert their geological potential into bankable reserve estimates. Countries where exploration capital retreats see their reserve conversion pipeline shrink over time.

-

Regulatory and fiscal environments: Royalty disputes, mandatory state participation requirements, and uncertainty around mining codes directly influence whether operating companies invest in reserve-building exploration or defer capital to more stable jurisdictions. Mali's recent trajectory illustrates this dynamic with unusual clarity.

Political Risk and the Reserve Reporting Connection

The relationship between political risk and reserve data quality is underappreciated by casual observers of the region. When government-mining company relations deteriorate, companies respond rationally by minimising discretionary capital expenditure. Exploration drilling is typically among the first activities to be scaled back, because it is early-stage spending with deferred returns.

The consequence is a compounding effect: political tension slows exploration, which slows resource conversion, which causes company-reported reserves to decline over successive reporting periods. Mali's declining company reserve figures since 2022 reflect exactly this dynamic. Burkina Faso's data gap similarly reflects a challenging operating environment that has limited the systematic work needed to generate reliable national estimates.

For investors assessing the West Africa gold reserves ranking, this means the numbers in any given table are as much a reflection of institutional and political conditions as they are of underlying geology.

Investment Implications of the Regional Reserve Landscape

From a capital allocation perspective, the reserve rankings carry differentiated signals across the five primary jurisdictions:

-

Ghana remains the anchor market for institutional mining investment in West Africa. Its established reserve base, mature regulatory framework, and depth of operator experience mean it attracts the largest share of regional exploration and development capital. The Enchi gold project, for example, recently received a capital cost estimate of $351 million from Newcore Gold, signalling that large-scale development investment continues to flow into the country.

-

Guinea and Côte d'Ivoire represent the highest-growth reserve expansion opportunities in the current cycle. Both countries have active discovery pipelines, and both sit on Birimian geology with demonstrated capacity for large deposits. They carry higher jurisdictional risk than Ghana but also higher potential for upward reserve revisions.

-

Mali's reserve trajectory warrants monitoring over a multi-year horizon. Sustained exploration slowdowns compound over time; if the current pace of reserve decline continues, Mali's second-place standing could be overtaken within the next five to seven years.

-

Burkina Faso represents a data arbitrage opportunity. Its production scale relative to its unquantified official reserve base creates an information gap that sophisticated investors willing to conduct independent geological assessment could exploit. The underlying endowment is almost certainly larger than any currently published figure suggests.

Governments negotiating major mining agreements without comprehensive reserve assessments risk systematically undervaluing their geological assets. The economic case for closing West Africa's reserve data gaps, particularly at current gold prices, has never been more compelling.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: West Africa Gold Reserves

Which country has the largest gold reserves in West Africa?

Ghana holds the region's largest confirmed geological gold reserves, estimated at approximately 1,000 metric tonnes by the USGS. It also produces more gold annually than any other African nation, with output of approximately 90 metric tonnes per year.

Is Guinea really the second-largest gold reserve holder in West Africa?

Guinea's government has claimed a reserve position exceeding 700 metric tonnes, placing it in direct contention with Mali. However, Mali's USGS-cited estimate of approximately 800 metric tonnes, even accounting for recent company-reported declines to 731 metric tonnes, likely means Mali retains second position. Guinea's figures carry lower independent verification than Mali's.

Why doesn't Burkina Faso appear with a confirmed reserve figure despite its high production?

The USGS 2025 dataset lists Burkina Faso's national gold reserve figure as unavailable, which reflects a lack of comprehensive national geological assessment rather than a lack of gold. Significant company-level reserves are documented, but no authoritative aggregate national figure has been published.

What is the difference between West Africa's geological gold reserves and central bank gold reserves?

Geological gold reserves are underground deposits that can be economically mined. Central bank gold reserves are monetary assets held as part of foreign exchange portfolios. These metrics are entirely separate, and West African nations generally hold modest central bank gold assets relative to their substantial geological endowments.

What geological formation hosts most of West Africa's gold?

The majority of the region's gold is hosted within the West African Craton, specifically the Birimian Greenstone Belt — an ancient formation spanning Ghana, Mali, Burkina Faso, Côte d'Ivoire, Guinea, Senegal, and Mauritania. Its structural continuity across borders explains why the region functions as a single prospective gold province divided by political rather than geological boundaries.

How much of global gold production comes from West Africa?

West Africa contributes approximately 10% of global gold supply. Over the past two decades, the region has generated an estimated 95 million ounces of new gold discoveries, outpacing both Canada and Australia over the same period.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Reserve estimates cited are drawn from publicly available data sources including USGS and company disclosures, and are subject to change. Readers should conduct independent due diligence before making any investment decisions. Further coverage of West African mining sector developments is available from Ecofin Agency at ecofinagency.com.

Want to Capitalise on the Next Major Gold Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into clear, actionable investment insights — explore the historic returns major discoveries have generated to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.