June 25, 2026

Why West Africa's Gold Reserve Rankings Are Harder to Read Than They Look

Few questions in African resource economics generate more confusion than the ranking of West African nations by gold reserves. At first glance, the question seems straightforward. In practice, the West Africa gold reserves ranking opens into a complex web of geological classification systems, inconsistent national reporting standards, and the ever-shifting economics of what makes a gold deposit actually worth mining.

The challenge begins with a distinction that is critical to anyone serious about understanding this debate. The difference between resources vs reserves is fundamental: a reserve, as defined under internationally recognised frameworks including the JORC Code, NI 43-101, and SAMREC, is the economically recoverable portion of a deposit. It must be supported by technical studies, ore grade analysis, production cost modelling, and a specific gold price assumption. A resource, by contrast, is a broader category of identified mineralisation that has not yet been demonstrated to meet those economic thresholds.

Critical distinction: When a government announces its country holds hundreds of tonnes of gold, it is often citing a figure that blends reserves, resources, and sometimes geological estimates that have not been subjected to any independent technical validation. These numbers are not interchangeable, but they are routinely treated as if they are.

This definitional gap is compounded by a second problem: West Africa does not operate under a unified, government-mandated reserve reporting standard. Consequently, regional rankings frequently compare fundamentally different categories of data across different countries, making direct comparisons inherently imprecise.

When big ASX news breaks, our subscribers know first

The Geological Engine Beneath the Numbers

The West African Craton and Its Gold-Bearing Greenstone Belts

The geological foundation underpinning West Africa's gold wealth is ancient in the truest sense. The West African Craton, a stable block of Precambrian crust, formed approximately 2.2 to 2.0 billion years ago. Embedded within it are gold-bearing greenstone belts, linear zones of ancient volcanic and sedimentary rock that served as conduits for gold-rich hydrothermal fluids over geological timescales.

These greenstone belts run through Ghana, Mali, Guinea, Côte d'Ivoire, Burkina Faso, and Senegal, providing the geological backbone for the region's gold endowment. However, the belts are not uniform in quality or concentration. The Birimian-age terranes found in Ghana and the Kedougou-Kéniéba inlier shared between Mali and Senegal are particularly well-endowed, which partly explains why Ghana and Mali have historically dominated regional production rankings. For a deeper understanding of why there is so much gold in West Africa, the geological history of the craton is essential reading.

What is less commonly appreciated is how the maturity and structural complexity of these belts influences ore grade distribution. Gold mineralisation in West African greenstone belts tends to be hosted in shear zones and along lithological contacts, meaning that deposit geometry is often complex. This has significant implications for reserve estimation: two deposits containing the same total gold inventory can have dramatically different reserve-to-resource conversion ratios depending on how their geometry responds to available mining methods.

How Exploration Intensity Shapes What We Know

A further complication in any West Africa gold reserves ranking is the enormous variation in historical exploration intensity across the region. Ghana has been subject to systematic geological surveying and commercial drilling for over a century, meaning its reserve estimates benefit from a dense dataset. Countries such as Guinea and parts of Burkina Faso have seen far less systematic exploration, and their true geological endowment may be substantially larger than current estimates suggest.

Current gold exploration trends show that, with gold prices sustaining levels above $2,000 per ounce and at times exceeding $2,500/oz in recent periods, the economic viability threshold for borderline deposits has shifted materially. Ore grades that were previously sub-economic are being re-evaluated across the region, and this is creating a dynamic in which the reserve picture is genuinely in flux. For investors, this means today's ranking is a snapshot, not a verdict.

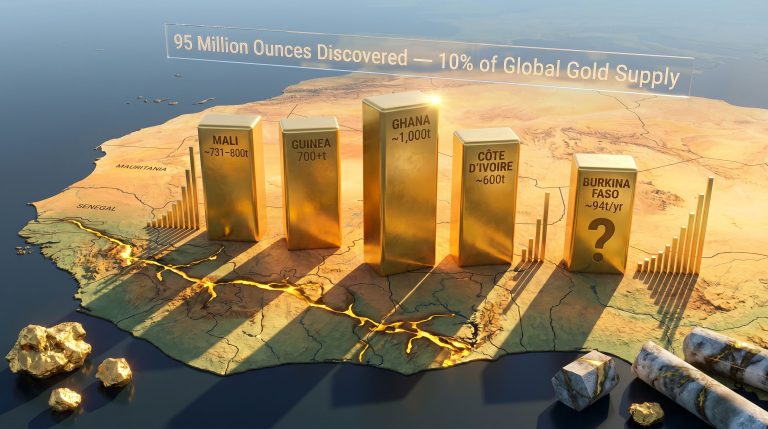

West Africa Gold Reserves Ranking by Country: The Full Breakdown

Methodology and Data Transparency

The rankings below draw primarily on USGS Mineral Commodity Summaries (2025 release), supplemented by national mining ministry disclosures and publicly reported mining company reserve statements. All figures represent estimated in-ground geological reserves measured in metric tonnes, not central bank gold holdings, which are tracked separately and follow entirely different frameworks.

Where national data is unavailable, company-level aggregate estimates are used as partial proxies, and this is noted explicitly. Readers should treat all figures as estimates subject to revision as exploration activity evolves and gold prices shift.

Summary Table: West Africa Gold Reserves Ranking (2025 Data)

| Rank | Country | Estimated Gold Reserves (Metric Tonnes) | Primary Source | Data Reliability |

|---|---|---|---|---|

| 1 | Ghana | ~1,000 | USGS 2025 | High |

| 2 | Mali | ~731–800 | USGS 2025 / Mali Ministry of Mines | Moderate (declining) |

| 3 | Guinea | ~700+ | Government estimate | Moderate (improving) |

| 4 | Côte d'Ivoire | ~600 | Official government figures | Moderate (expanding) |

| 5 | Burkina Faso | Not officially reported | USGS 2025 (unavailable) | Low (company data only) |

| 6 | Senegal | Emerging | Limited public data | Early-stage |

Ghana: West Africa's Undisputed Gold Reserve Leader

Ghana's position at the top of the West Africa gold reserves ranking is the only placement in the region that can be described as statistically robust. The USGS estimates Ghana's gold reserves at approximately 1,000 metric tonnes, a figure supported by decades of systematic exploration and a mature, well-documented industrial mining sector.

The country produces roughly 90 metric tonnes of gold annually, representing approximately 7% of global output, and holds the title of Africa's largest gold producer. Major operations are run by Newmont, Gold Fields, AngloGold Ashanti, Perseus Mining, and Asante Gold, creating a diversified production base that is not dependent on any single operator.

One aspect of Ghana's gold sector that is often underappreciated is the growing formalisation of artisanal and small-scale mining (ASM) output. A meaningful and increasing share of ASM production is now being captured through official reporting channels, which means Ghana's headline production figures are becoming more representative of total national output over time.

On the project development front, Newcore Gold's Enchi gold project has been estimated at a capital expenditure of $351 million, targeting production of approximately 104,000 ounces per year, adding further depth to Ghana's forward-looking production pipeline.

Mali: A Contested Second Place Under Measurable Pressure

Mali has long been treated as the region's second-largest gold reserve holder, but that position deserves more scrutiny than it typically receives. The USGS estimated Mali's reserves at 800 metric tonnes in its 2025 release. However, figures provided by Mali's Ministry of Mines showed that reserves held by mining companies had declined from 881.7 metric tonnes in 2022 to 731 metric tonnes by 2024, a reduction of approximately 17% in two years.

This divergence between the USGS top-down geological estimate and the ministry's bottom-up operational figure illustrates a broader problem in regional reserve tracking. The USGS figure reflects a geological interpretation that may not fully account for active depletion at operating mines, while the ministry figure captures current company-held reserve declarations but may exclude undiscovered deposits and early-stage projects.

The structural pressures on Mali's reserve base are real and worth monitoring carefully:

- Exploration activity has slowed significantly in recent years

- Tensions between the government and mining companies over revenue-sharing arrangements have created investor hesitancy

- New capital commitments required to replenish depleting reserves through fresh drilling are not materialising at the rate needed to maintain the reserve base

- The political environment in the broader Sahel region has added a risk premium that suppresses exploration investment

Investor note: A declining reserve base without active reserve replacement drilling is a structural warning sign. For any country, the long-term production trajectory is determined not by current mine output but by the rate at which new reserves are being identified to replace those extracted.

Guinea: The Rapidly Closing Gap

Guinea's government has positioned the country as the second-largest gold reserve holder in West Africa, citing official estimates of more than 700 metric tonnes. The reserve base is concentrated in key prefectures including Siguiri, Kouroussa, Mandiana, Dinguiraye, and Kankan, which form the heart of Guinea's gold-producing corridor.

The industrial anchor of Guinea's gold sector is AngloGold Ashanti's Siguiri mine, one of the region's significant long-running operations. The development pipeline is also expanding, with Predictive Discovery's Bankan project attracting growing investor attention as one of the more substantial emerging deposits in the sub-region.

Guinea's claim to second place carries some validity on trajectory, even if it has not yet been confirmed by independent technical validation. Rising gold prices are improving the economics of deposits previously considered marginal, and a sustained period of elevated prices could accelerate the conversion of Guinea's broader resource inventory into formally declared reserves.

Côte d'Ivoire: The Region's Most Dynamic Growth Story

Of all the countries in the West Africa gold reserves ranking, Côte d'Ivoire presents the most compelling growth narrative over the medium term. Official estimates place reserves at approximately 600 metric tonnes, but this figure may be conservative relative to the discovery pipeline currently advancing through the development cycle.

The country is reporting a wave of major mineral resource discoveries, with several individual deposits containing mineral resources exceeding 100 metric tonnes of gold, including:

- The Koné deposit

- The Boundiali deposit

- The Doropo deposit

These are resources rather than declared reserves at this stage, but as definitive feasibility studies progress and economic viability is confirmed under prevailing gold prices, a portion of this inventory is expected to convert into reserve declarations, potentially triggering an upward revision to Côte d'Ivoire's national reserve figure in the coming years.

Burkina Faso: High Production, Incomplete Reserve Picture

Burkina Faso represents one of the most intellectually interesting cases in the West Africa gold reserves ranking, precisely because the data gap does not reflect a lack of gold. The USGS 2025 data lists Burkina Faso's national reserve figure as unavailable, while simultaneously recording national production of more than 94 metric tonnes in 2025, making it one of the region's most prolific producers.

Company-level data provides a partial window into what the national reserve base might look like. West African Resources reported approximately 7 million ounces, or around 218 metric tonnes, across its Sanbrado, Kiaka, and Toega assets in Burkina Faso during 2025. Extrapolating this approach across all operating industrial mines would suggest a substantial aggregate reserve base, though the resulting total would still exclude artisanal mining zones, undeveloped deposits, and exploration-stage projects.

The absence of a consolidated national reserve audit in Burkina Faso reflects:

- Security challenges in parts of the country that have disrupted systematic geological survey work

- Governance and administrative capacity constraints limiting the ability to aggregate company-level data into a national figure

- The absence of a mandated public reporting requirement for consolidated national reserve disclosures

Speculative insight: If Burkina Faso were to commission and publish a comprehensive national reserve audit consolidating industrial, artisanal, and development-stage data, its position in the regional ranking could shift materially upward. The data gap is a reporting failure, not a geological one.

Senegal: An Emerging Contender

Senegal sits at the early end of the West Africa gold reserves development spectrum. Reserve estimates remain limited by the volume of systematic exploration completed to date, but the country's position on the West African Craton provides geological grounds for optimism. The Kedougou-Kéniéba inlier, which Senegal shares with Mali, is one of the craton's most gold-prospective structural zones, and junior to mid-tier exploration companies are increasingly active in the region.

The Reserve vs. Central Bank Gold Distinction: Why It Matters More Than Most Realise

A persistent source of public confusion in discussions about gold reserve rankings is the conflation of two entirely separate metrics.

| Metric | Definition | Who Tracks It |

|---|---|---|

| Geological/Mining Reserves | Economically recoverable gold in the earth's crust within a country | USGS, mining ministries, companies |

| Central Bank Gold Holdings | Physical gold held by a nation's central bank as part of foreign exchange reserves | IMF, World Gold Council |

The contrast between these two metrics is striking when examined across Africa. Ghana leads West Africa and indeed most of the continent in geological gold reserve endowment with approximately 1,000 metric tonnes in the ground, yet its central bank holds only around 18.6 tonnes of physical gold. Furthermore, when reviewing global gold reserve rankings, North African nations dominate the central bank holdings category:

- Algeria: approximately 173.6 tonnes of central bank gold

- Libya: approximately 146.6 tonnes

- Egypt: approximately 129.5 tonnes

None of these countries ranks among West Africa's top geological gold reserve holders. The divergence illustrates that resource wealth and monetary gold accumulation are driven by entirely different policy decisions and economic structures.

Four Forces That Will Reshape the Rankings Over the Next Decade

The current West Africa gold reserves ranking should be understood as a dynamic snapshot rather than a fixed hierarchy. Four forces are likely to drive meaningful changes in relative standings over the coming years.

1. Exploration Investment Cycles

Countries sustaining high levels of exploration capital deployment, particularly Ghana and Côte d'Ivoire, will see their reserve bases grow as new drilling converts geological potential into declared resources and eventually reserves. Countries experiencing reduced exploration activity face progressive depletion without replacement.

2. Gold Price Dynamics

At sustained gold prices above $2,500 per ounce, significant volumes of sub-economic resources across Guinea and Burkina Faso become viable for reserve reclassification. The reserve-to-resource conversion rate across the region is directly sensitive to the gold price assumption embedded in feasibility studies.

3. Regulatory and Fiscal Stability

Mining codes governing royalty rates, profit-sharing, and state participation directly influence investor willingness to commit exploration capital. Regulatory uncertainty, as clearly demonstrated by the slowdown in Mali, can suppress exploration activity and accelerate reserve depletion without replacement. Conversely, stable frameworks attract sustained capital and support reserve growth.

4. Geopolitical and Security Conditions

Instability across the Sahel has disrupted exploration programmes in Burkina Faso and Mali, creating a structural exploration deficit in two of the region's geologically most prospective countries. Ghana and Côte d'Ivoire, operating in more stable environments, continue to attract capital that reinforces their reserve development trajectories.

Frequently Asked Questions: West Africa Gold Reserves

Which country has the largest gold reserves in West Africa?

Ghana holds the largest estimated gold reserves in the region at approximately 1,000 metric tonnes according to USGS 2025 data. This ranking is the most statistically reliable in the region due to decades of systematic exploration and transparent industrial mining operations.

Why is the ranking below Ghana so contested?

Mali, Guinea, and Côte d'Ivoire all present valid claims depending on which data source and which definition of reserves is applied. Mali holds the second position in most independent assessments, but its reserve base is declining. Guinea is closing the gap, and Côte d'Ivoire's discovery pipeline is accelerating. The ranking below Ghana is genuinely fluid.

Why is Burkina Faso absent from official reserve rankings despite being a major producer?

The USGS 2025 data marks Burkina Faso's reserve column as unavailable, not because the country lacks gold, but because no comprehensive national reserve audit has been publicly released. The country's actual geological endowment, based on company-level data, is likely substantial.

What is the difference between a gold reserve and a gold resource?

A reserve is the economically recoverable portion of an identified deposit, validated by technical and financial analysis at a specific gold price. A resource is a broader category that includes mineralisation not yet confirmed as economically viable. All reserves were once resources, but not all resources will become reserves. Furthermore, when interpreting drill results, understanding this distinction is critical for assessing a project's true economic potential.

The next major ASX story will hit our subscribers first

Strategic Outlook for Investors and Policymakers

For investors assessing West African gold exposure, the reserve rankings carry direct implications for capital allocation:

- Ghana remains the region's lowest-risk destination for large-scale gold investment, offering reserve depth, infrastructure maturity, and regulatory track record

- Côte d'Ivoire represents the most compelling medium-term growth story, with a discovery pipeline that could drive meaningful reserve upgrades

- Guinea offers high geological upside but requires careful due diligence on reserve validation and regulatory dynamics

- Burkina Faso presents a paradox of strong production performance alongside significant data and governance uncertainty

- Mali warrants close monitoring, with declining company-held reserves and reduced exploration activity representing measurable headwinds

For policymakers seeking to improve their country's standing and attract investment, the pathway is clear. In addition, African gold reserve data published by international economic trackers provides a useful benchmark for understanding where each nation currently stands. The key steps are:

- Commission and publish consolidated national reserve audits using internationally recognised reporting standards

- Publish annual reserve updates that aggregate both industrial and artisanal sector data

- Invest in systematic national geological survey programmes to quantify broad geological potential

- Maintain stable, predictable fiscal and regulatory frameworks that support long-term exploration investment

- Consider royalty-in-kind mechanisms to build central bank gold holdings alongside geological reserve development

The West Africa gold reserves ranking is ultimately less a fixed leaderboard and more a reflection of which countries are investing systematically in understanding, developing, and transparently reporting their geological endowment. In that sense, the ranking is as much a governance indicator as it is a geological one.

This article contains forward-looking statements and estimates based on publicly available data. Reserve figures are subject to revision as exploration activity evolves, gold prices change, and new technical studies are completed. Nothing in this article constitutes financial or investment advice. Readers should conduct independent due diligence before making investment decisions.

Want to Stay Ahead of the Next Major West African Gold Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological data into actionable investment insights — explore historic discovery returns on the Discovery Alert discoveries page to understand just how substantial these opportunities can be, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.