June 10, 2026

The Resource-Revenue Architecture That Keeps Western Australia Fiscally Exceptional

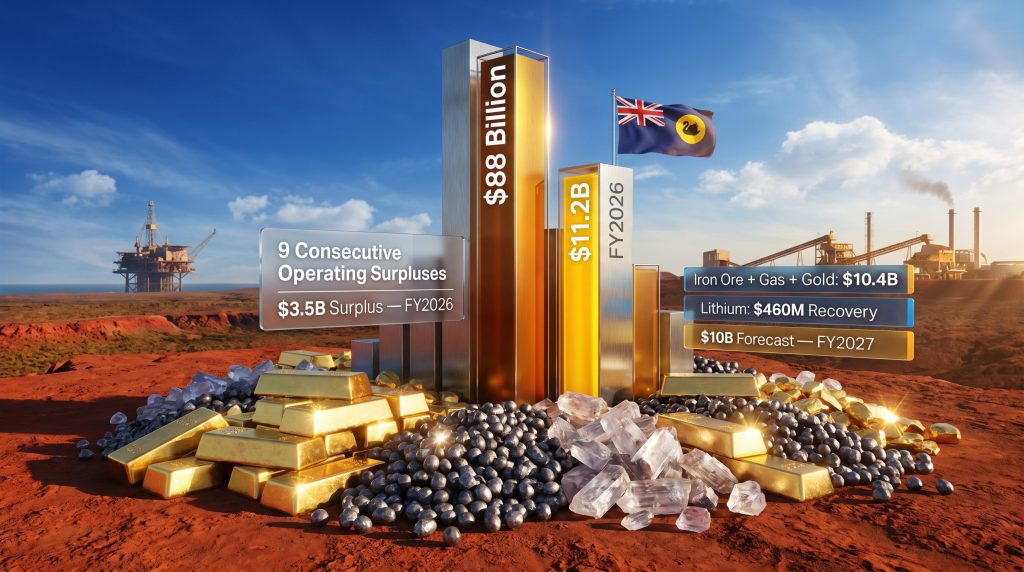

Few fiscal structures in the developed world are as deliberately engineered around a single economic force as Western Australia's. While most advanced economies construct their public finances around broad-based taxation, consumption levies, and diversified revenue streams, Western Australia has spent decades calibrating a model where the extraction of minerals and energy directly funds hospitals, schools, roads, and household relief. The result is a Western Australia mining operating surplus that has now produced eight consecutive years of positive outcomes, with a ninth firmly in sight, and a cumulative resource revenue base so large it strains conventional comparison.

Understanding how this model works, what sustains it, where its vulnerabilities lie, and how surplus revenues are being recycled into long-term productive assets requires moving beyond headline figures and into the structural mechanics underneath.

When big ASX news breaks, our subscribers know first

What $11.2 Billion in a Single Year Actually Means

In the 2026 financial year, combined royalty income and North West Shelf Grant payments delivered $11.2 billion to the Western Australian state government, according to reporting by the Chamber of Minerals and Energy of Western Australia (CME). This figure exceeded Treasury's own prior-year forecasts by approximately $2.5 billion, a variance that reflects the degree to which commodity markets outperformed institutional modelling.

The fiscal consequences of this windfall were immediate and meaningful. The royalty surge underpinned a $3.5 billion operating surplus while simultaneously enabling a $1 billion cost-of-living relief package for Western Australian households. These are not small figures for a sub-national government. The operating surplus alone would rank as a creditable fiscal outcome for many mid-sized sovereign nations, let alone a state within a federal system.

| Metric | FY2026 Result |

|---|---|

| Royalties + North West Shelf Grant Payments | $11.2 billion |

| Operating Surplus | $3.5 billion |

| Cost-of-Living Relief Funded | $1.0 billion |

| Iron Ore, Gas + Gold Combined | $10.4 billion |

| Lithium Royalty Contribution | $460 million |

| Variance vs Prior Year Treasury Forecast | +$2.5 billion |

Treasury's forward projections for FY2026/27 anticipate $10 billion in royalties and North West Shelf Grant payments, supporting a projected $2.4 billion operating surplus. If realised, this would mark nine consecutive years of operating surpluses for the state, a streak with no direct parallel among Australian states.

Furthermore, the WA resources sector impact extends well beyond government accounts, touching virtually every corner of the state's economy. Western Australia's resources sector provided more than a quarter of total state government revenue over an eight-year period spanning the COVID-19 pandemic and two global oil shocks, according to CME data, underscoring the counter-cyclical resilience embedded in the state's fiscal design.

Three Commodities Carrying the Fiscal Load

The dominant feature of Western Australia's royalty revenue profile is its concentration in three commodities that, collectively, drove $10.4 billion of the state's FY2026 royalty receipts. Each plays a structurally distinct role within the fiscal model.

Iron ore remains the single most important contributor. Western Australia supplies a substantial share of global seaborne iron ore demand, primarily directed at Asian steel manufacturing. Despite periodic price volatility, consistent production volumes from the Pilbara have maintained iron ore's position as the state's primary fiscal anchor. The iron ore demand outlook from Asian trading partners creates an element of demand inelasticity that other commodity categories cannot replicate.

Natural gas via the North West Shelf contributes through a grant mechanism that translates LNG and gas production revenues into direct state government receipts. This mechanism differs technically from standard royalty structures: rather than a simple percentage levy on production value, North West Shelf Grant payments reflect contractual arrangements between the Commonwealth and state governments regarding resource revenue sharing from offshore petroleum production. This distinction matters because it means gas revenues respond differently to price movements than iron ore royalties.

Gold adds a third pillar centred on the Goldfields region, where operations ranging from major producing mines to active exploration companies sustain high output volumes. Elevated gold prices in recent years have amplified royalty receipts from this sector considerably, adding a commodity with a different demand profile from the industrial commodities that dominate the state's revenue base.

| Commodity | FY2026 Royalty Contribution | Primary Demand Driver |

|---|---|---|

| Iron Ore + Gas + Gold (combined) | $10.4 billion | Asian industrial and energy demand |

| Lithium | $460 million | Global battery manufacturing recovery |

| All Other Minerals | Residual balance | Diversified base metals, mineral sands |

Lithium's Royalty Recovery: Understanding a Battery Metals Cycle

Among the lesser-understood dynamics within Western Australia's royalty profile is the extraordinary volatility of battery minerals revenues. Lithium's contribution of $460 million in FY2026 represents a meaningful rebound following what CME described as several difficult years for the battery-making ingredient. The lithium market downturn saw prices fall sharply from the extraordinary highs recorded during the electric vehicle supply chain scramble of 2022 and 2023.

This volatility is worth unpacking for investors and analysts tracking WA's fiscal position. Unlike iron ore, where production is dominated by a small number of very large integrated miners with long-term supply contracts, Western Australia's spodumene lithium sector includes a broader mix of producers, many of whom operate at costs that become uneconomic during price downturns. When lithium prices collapsed from their peak levels, multiple Western Australian producers curtailed or suspended operations, directly compressing royalty receipts.

The FY2026 recovery reflects stabilising demand conditions for spodumene, the hard-rock lithium ore that Western Australia produces in large quantities before conversion to lithium hydroxide or carbonate for battery applications. However, the sector's royalty contribution remains approximately 22.6 times smaller than the combined iron ore, gas, and gold royalties, illustrating how far battery minerals must scale before they materially alter the state's fiscal equation.

Battery metals contribute meaningfully to WA's royalty base, but the sector's price sensitivity and production cost structures create a fundamentally different risk profile from legacy commodities. Lithium royalties can contract by hundreds of millions of dollars in a single year during price downturns, adding a secondary layer of revenue volatility to WA's fiscal model.

The $88 Billion Cumulative Benchmark: Contextualising a Decade of Extraction

Since the 2019 financial year, Western Australia has accumulated $88 billion in combined royalty and North West Shelf Grant receipts. CME's budget commentary contextualises this figure through two structural comparisons that illuminate the scale of the resources sector's fiscal contribution in terms most citizens can appreciate.

Infrastructure comparison: The state's total Asset Investment Program across the same eight-year period totals $69.1 billion. This means the resources sector's cumulative royalty contribution theoretically exceeds the cost of every infrastructure project the Western Australian government has built over nearly a decade, by a margin approaching $19 billion.

Workforce cost comparison: The combined salary expenditure for all public sector nurses, doctors, teachers, and police officers across the same eight years totals approximately $92.6 billion, meaning royalty receipts approach, though do not quite match, the cost of funding essential services personnel entirely through commodity revenues.

| Comparison Category | Eight-Year Value |

|---|---|

| Cumulative Royalties + NWS Grants (FY2019-FY2026) | $88 billion |

| Total Asset Investment Program (same period) | $69.1 billion |

| Surplus coverage margin | ~$18.9 billion |

| Public sector essential workers salary total | $92.6 billion |

| Royalty shortfall vs salary total | ~$4.6 billion |

These comparisons are pedagogically effective but carry important caveats. The $88 billion represents gross royalty and grant receipts, not net fiscal benefit, since royalty revenues are partially offset by the state's own expenditure on resource sector enabling infrastructure, regulatory capacity, and environmental compliance.

Additionally, the operating surplus is a different metric from the public sector cash position, which incorporates capital expenditure. During periods of intensive infrastructure investment, the state can simultaneously record a strong operating surplus while running a net cash deficit. This occurred during the nine months to March 2025, when a $2.8 billion operating surplus coexisted with a $2.3 billion public sector cash deficit driven by capital commitments.

The Jobs and Strategic Export Dimension

The broader picture of WA economic contribution extends well beyond government accounts. According to CME, approximately 650,000 West Australians rely on the resources industry for their livelihoods, representing a substantial portion of the state's total workforce across direct employment, contracting, services, and supply chain roles.

The sector also functions as a strategic supplier to major Asian economies, which depend on Western Australian iron ore for steel production, LNG for power generation and industrial processes, and increasingly, battery minerals for energy transition programmes. CME's Aaron Walker, the organisation's head of economics, has characterised WA's commodities as a significant strategic asset not only for the domestic economy but for the trading partners whose industrial systems rely on uninterrupted access to these materials.

This dual role elevates the sector beyond a conventional extractive industry into what functions as sovereign economic infrastructure. When global supply chains tighten, Western Australia's position as a reliable, large-volume supplier of essential commodities becomes more, not less, commercially valuable. Consequently, this counter-cyclical dynamic reinforces the fiscal model's resilience.

Fuel security has emerged as a related policy priority. The Western Australian government has moved to establish a strategic diesel stockpile, recognising that the mining sector's operational continuity depends on uninterrupted access to fuel. Given the sector's contribution to state revenues, protecting its operating capacity is itself a fiscal policy decision.

The next major ASX story will hit our subscribers first

How Surplus Revenues Are Being Reinvested

The 2026/27 Western Australian Budget deploys resource-derived surpluses across several investment streams designed to sustain the enabling conditions for continued sector growth.

Energy Transition Infrastructure

A $1.4 billion Clean Energy Fund will support new transmission infrastructure within the South West Interconnected System (SWIS) to connect renewable energy projects to the grid. This investment is reinforced by recent power purchase agreements between Synergy, Water Corporation, and wind farm developers. The logic here is instructive: the resources sector requires reliable, cost-competitive energy, and transitioning that energy base to renewables reduces both operating costs and long-term emissions exposure.

Industrial Water Security

$651 million has been committed toward doubling the capacity of the Dampier seawater desalination plant, structured as a 50:50 joint venture with Rio Tinto. The completed facility, valued at approximately $1.1 billion, will deliver 8 gigalitres of desalinated water annually to the West Pilbara Water Supply Scheme. This directly reduces pressure on regional aquifer systems, which face increasing drawdown as mining operations deepen and processing water demand grows.

Regional Workforce Housing

$419 million from the Government Regional Office Housing programme, supplemented by $170 million in contributions from Rio Tinto, BHP, and Hancock, will deliver more than 500 additional homes for essential workers across Port Hedland, Karratha, Kalgoorlie, Bunbury, Broome, Geraldton, and Albany, with completion targeted by 2030.

Housing scarcity in regional Western Australia has historically constrained workforce availability for both mining and public sector employers. When accommodation is insufficient, workers choose not to relocate, fly-in fly-out rosters become structurally dominant, and community services suffer from chronic staffing gaps. This investment addresses a supply-side labour market constraint that both industry and government share an interest in resolving.

Industrial Precinct Development

$92 million from the Strategic Industries Fund has been allocated to land assembly and planning works across the Western Trade Coast, the Kemerton strategic industrial area, and the Boodarie strategic industrial area, including common user infrastructure and a dedicated desalination plant at Boodarie.

| Budget Initiative | State Allocation | Industry Co-contribution | Total Value |

|---|---|---|---|

| Clean Energy Fund (SWIS Transmission) | $1.4 billion | N/A | $1.4 billion |

| Dampier Desalination Expansion | $651 million | Rio Tinto (50%) | ~$1.1 billion |

| Regional Worker Housing | $419 million | $170 million (Rio Tinto, BHP, Hancock) | ~$589 million |

| Western Trade Coast / Boodarie Precinct | $92 million | N/A | $92 million |

| Cost-of-Living Relief (FY2026) | $1.0 billion | N/A | $1.0 billion |

The Structural Risks Beneath the Surplus Story

The Western Australia mining operating surplus model is compelling, but its structural dependencies deserve direct examination rather than assumption.

Revenue concentration risk is the most significant. Iron ore alone accounts for the dominant share of royalty income, creating a fiscal position that is highly sensitive to a single commodity's price trajectory. The nine months to March 2025 demonstrated this vulnerability directly: iron ore royalties declined by approximately $1.6 billion during that period, while lithium's $437 million royalty decline added a secondary contraction.

Operating versus cash surplus tensions create a second layer of complexity. The standard operating surplus metric measures revenue minus recurrent expenditure but excludes capital investment. During periods of aggressive infrastructure deployment, the state can simultaneously present a positive operating surplus and a negative cash position. Investors and policy analysts tracking fiscal sustainability need to monitor both metrics rather than relying solely on the headline surplus figure.

Commodity cycle timing adds a third dimension. The cumulative $88 billion in royalties was accumulated during a period that included the extraordinary iron ore price supercycle driven by post-pandemic infrastructure stimulus in China, elevated gas prices following European energy market disruptions, and gold's extended bull market. Whether these conditions represent a new structural floor or a cyclical high is genuinely uncertain.

Furthermore, the outlook for resource and energy exports adds another layer of uncertainty to revenue forecasting. Treasury's own forecast of declining royalties from $11.2 billion in FY2026 to $10 billion in FY2027 already reflects some mean-reversion expectations, as noted by analysts covering Western Australia's budget position.

Disclaimer: Forward-looking projections regarding commodity prices, royalty revenues, and government fiscal positions involve material uncertainty. Past surplus performance does not guarantee future outcomes. Investors and analysts should treat Treasury forecasts as central estimates within a range of scenarios rather than as reliable predictions. This article does not constitute financial advice.

What WA's Model Reveals About Resource-Backed Fiscal Policy

Western Australia's Western Australia mining operating surplus track record offers one of the clearest empirical examples of how resource revenues, when channelled through disciplined fiscal frameworks, can fund public services, infrastructure, and household relief at scale without accumulating structural debt. Indeed, reporting from the ABC highlights how the state's budget has become a model of resource-backed governance that other jurisdictions study closely.

The model rests on three reinforcing pillars:

-

Royalty calibration that captures a meaningful share of commodity windfalls without deterring the investment required to generate future production.

-

Commodity diversification across iron ore, gas, gold, and emerging battery minerals, reducing single-point exposure while each commodity cycle peaks and troughs at different intervals.

-

Productive reinvestment of surplus revenues into water security, energy infrastructure, workforce housing, and industrial precincts, sustaining the enabling conditions for continued sector operation rather than simply banking windfall revenues.

The critical limitation is that this architecture functions exceptionally well under conditions of sustained Asian commodity demand and stable production volumes. A scenario involving simultaneous price weakness across iron ore, gas, and gold would test the model's limits in ways not yet experienced during the current surplus streak. The state's fiscal planners, and the investors who depend on WA's economic health, would consequently be well served by monitoring the commodity price assumptions embedded in each successive budget alongside the headline surplus figures themselves.

Readers seeking additional context on Western Australia's fiscal position and mining sector performance may find value in reviewing publicly available budget documentation from the Western Australian Department of Treasury and industry analysis published by the Chamber of Minerals and Energy of Western Australia.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex mineral data into actionable insights for both short-term traders and long-term investors. Explore historic examples of extraordinary discovery returns and begin your 14-day free trial today to position yourself at the forefront of Western Australia's next major resource opportunity.