June 21, 2026

The Hidden Leverage Point: Why Yttrium Oxide Became the Sharpest Tool in China's Trade Arsenal

Most discussions of rare earth supply chains focus on materials powering electric vehicles and wind turbines. Neodymium, dysprosium, and cobalt dominate the policy conversation, attracting billions in diversification investment and generating endless headlines about the energy transition. But beneath this visible layer of critical mineral risk sits a quieter, more technically specialised category of materials whose disruption carries consequences that extend directly into national security infrastructure.

Yttrium oxide sits in this category. It is not a material that features prominently in green energy narratives. It does not power EV motors or store grid-scale electricity. Instead, it performs a more fundamental industrial function: it keeps jet engines and gas turbines from destroying themselves under extreme operating temperatures. When China yttrium oxide exports to the US were effectively halted through export licensing controls in April 2025, the consequences for aerospace and semiconductor manufacturing were both immediate and extraordinarily difficult to resolve.

Understanding why requires examining not just the trade policy decision itself, but the material science, supply chain architecture, and geopolitical calculation that made yttrium oxide a uniquely effective pressure point.

When big ASX news breaks, our subscribers know first

What Makes Yttrium Oxide Technically Irreplaceable

Yttrium oxide (Y₂O₃) is a white crystalline powder classified as a rare earth compound, though yttrium itself is relatively abundant in the earth's crust compared to many other rare earth elements. Its commercial value derives not from geological scarcity but from a specific combination of chemical and physical properties that make it exceptionally well-suited for high-temperature industrial applications.

The compound's primary industrial role is as a constituent of yttrium-stabilised zirconia (YSZ), the dominant material system used in thermal barrier coatings applied to turbine blades, combustion chambers, and other hot-section components in jet engines and power generation turbines. These coatings operate under conditions that would rapidly degrade unprotected metal alloys, allowing turbine inlet temperatures to exceed the melting point of the underlying metal substrate.

Without functional thermal barrier coatings, aircraft cannot fly safely. This is not a commercial inconvenience — it is an engineering reality that makes yttrium oxide functionally non-negotiable for the aerospace industry in the near term.

The semiconductor application is distinct but equally constrained. During plasma etching processes used in chip fabrication, the chamber walls and components are exposed to highly corrosive plasma environments. Yttrium oxide ceramic coatings provide resistance to this plasma erosion, protecting both the chamber and the silicon wafer being processed. Because these coatings degrade with use and require periodic replacement, semiconductor fabs face ongoing demand for yttrium oxide that cannot be simply paused or batched.

Application Profile and Substitutability Assessment

| Application Sector | Specific Function | Substitution Difficulty |

|---|---|---|

| Aerospace turbines | Thermal barrier coatings via YSZ | Very high, multi-year re-certification required |

| Power generation turbines | High-temperature protective layers | Very high |

| Semiconductor fabrication | Plasma etch chamber linings | High, alternative ceramics under development |

| Phosphors and displays | Luminescent activation | Moderate, alternatives commercially available |

| Optical glass | Refractive index modification | Moderate |

The critical distinction between yttrium oxide and most other rare earth elements is the nature of its end-use concentration. Unlike neodymium, which serves a broad market spanning EVs, wind turbines, consumer electronics, and industrial motors, yttrium oxide's dominant applications cluster specifically in aerospace, defence-adjacent manufacturing, and advanced semiconductor production. This concentration means supply disruptions hit the most strategically sensitive segments of US industrial capacity first.

The Architecture of a Supply Shock: How China's Export Controls Unfolded

The April 2025 decision by China to impose export licensing requirements on yttrium and six additional rare earth materials did not emerge in isolation. It arrived at the peak of an escalating US-China trade confrontation, and was widely read by industry analysts and trade policy researchers as a calibrated countermeasure to US tariff pressure. Furthermore, China's rare earth export restrictions were interpreted as a deliberate strategic response rather than a routine regulatory adjustment.

What followed was not a gradual tightening but an effective cessation of yttrium oxide exports to the United States. While other rare earth materials subject to the same April 2025 controls saw partial export resumption following a late-2025 bilateral trade truce, yttrium shipments remained largely blocked well into 2026, according to Reuters reporting via Mining.com.

This selective retention is analytically significant. It suggests that Beijing was not applying export controls uniformly across rare earth categories but was making deliberate, material-specific decisions about where restrictions would be maintained. Analysts cited by Reuters noted that the close relationship between aerospace manufacturing and defence production may have contributed to China's particular reluctance to restore yttrium oxide flows, even as diplomatic pressure mounted.

A Reconstructed Timeline of the Supply Disruption

| Period | Development |

|---|---|

| April 2025 | China imposes export licensing requirements on yttrium and six other rare earth materials |

| Mid-2025 | US yttrium oxide imports effectively halt; production stoppages begin at aerospace and semiconductor firms |

| Late 2025 | Partial US-China trade truce restores some rare earth flows; yttrium remains restricted |

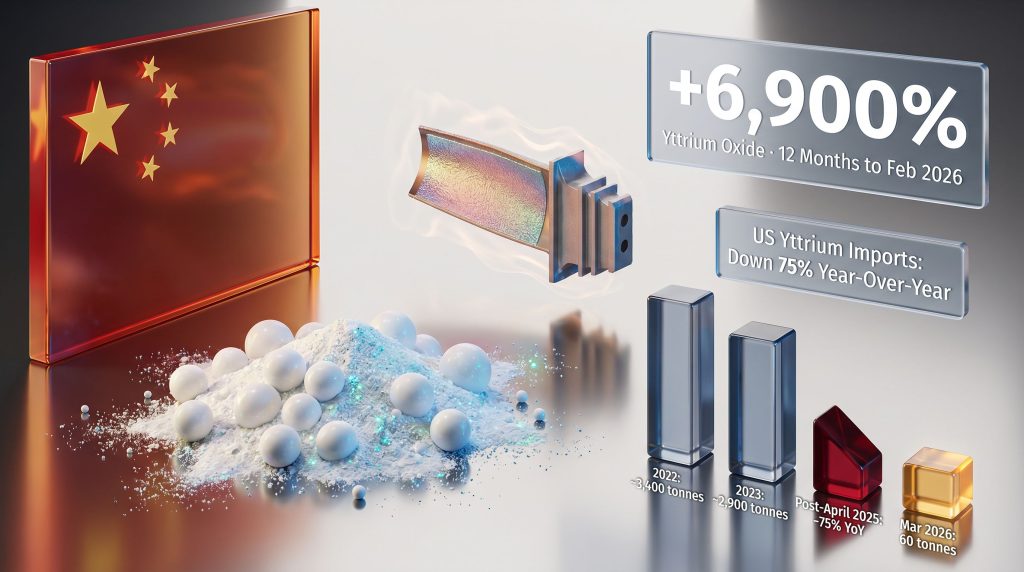

| February 2026 | China's global yttrium exports reach 20 tonnes, the highest post-control monthly volume but still well below pre-restriction baselines |

| March 2026 | A 60-tonne yttrium oxide shipment is approved for export to the United States |

| April 2026 | Cumulative US yttrium imports over the prior 12 months remain 75% below the equivalent prior-year period (Reuters/Mining.com, April 30, 2026) |

The timeline reveals a pattern that goes beyond a simple trade dispute. The durability of yttrium restrictions through a broader diplomatic thaw indicates that China viewed this material as occupying a different strategic category than other controlled rare earths. The longer controls held, the more the disruption compounded for manufacturers with no alternative sourcing pathway.

Quantifying the Damage: Price Surge and Volume Collapse

The market response to China's yttrium oxide controls produced one of the most extreme commodity price dislocations recorded in the modern rare earth sector. According to Reuters reporting published via Mining.com on April 30, 2026, yttrium oxide prices rose approximately 6,900% in the 12 months to February 2026. European markets, though geographically distant from the US-China trade conflict, experienced a parallel surge of approximately 4,400% from January 2025 baseline levels, reflecting the global concentration of Chinese refined yttrium oxide supply.

These figures deserve careful interpretation. A price increase of this magnitude does not represent normal commodity market volatility, cyclical demand fluctuation, or speculative trading pressure. It reflects a structural removal of dominant supply from the market combined with demand that remained essentially inelastic in the short term. Aerospace manufacturers cannot reduce their consumption of thermal barrier coating materials without grounding aircraft. Semiconductor fabs cannot defer chamber maintenance without losing production capacity.

Industry Note: Yttrium oxide is not traded on major commodity exchanges with standardised contracts and transparent pricing. Pricing is largely determined through direct negotiation between producers and industrial buyers, often under multi-year supply agreements. When those agreements cannot be fulfilled, spot market pricing can move with extreme volatility in ways that do not occur in exchange-traded commodity markets.

Volume Data: Mapping the Export Collapse

| Metric | Data Point | Source |

|---|---|---|

| US yttrium imports over 12 months post-controls | Down 75% year-over-year | Reuters/Mining.com, April 30, 2026 |

| March 2026 single shipment volume | 60 tonnes | Reuters/Mining.com, April 30, 2026 |

| March 2026 shipment relative to prior period | 50% larger than all US-bound yttrium since April 2025 | Reuters/Mining.com, April 30, 2026 |

| February 2026 global Chinese yttrium exports | 20 tonnes, highest post-control monthly volume | Reuters/Mining.com, April 30, 2026 |

| Rare earth magnet exports to US (Jan-Feb 2026) | 994 tonnes, down 22.5% year-over-year | Reuters/Mining.com, April 30, 2026 |

The volume data illustrates a critical asymmetry that investors and policymakers often overlook. Even at the February 2026 peak of 20 tonnes per month of global yttrium exports from China, volumes remained far below the levels required to restore pre-restriction US supply access. The fact that a single 60-tonne shipment in March 2026 represented more yttrium oxide than had reached the US in the entire preceding year underscores the completeness of the supply interruption.

A less commonly understood aspect of yttrium oxide trade is the distinction between yttrium metal, yttrium compounds, and yttrium oxide specifically. The Reuters report noted that there were no shipments of other yttrium compounds or metals to the US in March 2026, meaning the partial resumption was confined to the oxide form most immediately relevant for aerospace coatings. This specificity suggests a targeted and limited approval rather than a broad relaxation of yttrium trade restrictions.

Decoding the March 2026 Shipment: Signal or Anomaly?

The approval of a 60-tonne yttrium oxide shipment to the US in March 2026 is significant as a data point, but its meaning is contested among those tracking the rare earth trade landscape. Three distinct analytical interpretations deserve consideration.

1. A Diplomatic Concession Within Active Negotiations

The timing of the shipment approval, occurring within a period of ongoing US-China trade engagement, is consistent with the interpretation that Beijing authorised the export as a calculated gesture within bilateral negotiations. Under this reading, the shipment represents a tangible deliverable offered to demonstrate goodwill without constituting a formal policy reversal or a commitment to sustained export normalisation.

2. A Response to Documented Industrial Pressure

Multiple affected US aerospace and semiconductor companies mounted formal lobbying campaigns directed at the US government during the period of supply restriction, with the explicit goal of securing diplomatic intervention to restore yttrium oxide access. The March 2026 shipment approval followed this sustained pressure campaign, suggesting that coordinated government-industry engagement created sufficient bilateral urgency to unlock a one-off export authorisation.

3. The Beginning of a Selective Easing

A more optimistic reading holds that the March approval signals the start of a gradual restoration of yttrium oxide trade flows, potentially linked to reciprocal trade accommodations made by the US. Under this interpretation, the 60-tonne shipment is the first instalment of a broader normalisation.

Critical Caveat: Even incorporating the March 2026 shipment into the cumulative data, US yttrium oxide imports over the trailing 12 months remain 75% below prior-year levels. A single large shipment does not constitute supply chain normalisation. Analysts and procurement officers should not interpret this event as evidence that the structural vulnerability has been resolved.

What makes the March approval analytically interesting is a detail that receives little attention: the shipment was composed exclusively of yttrium oxide, with no accompanying yttrium metal or other compounds. This specificity argues against a blanket policy relaxation and suggests individual export licence approvals are being made at the compound level, implying that China retains full capacity to restrict or resume flows with surgical precision.

Downstream Consequences: Who Actually Absorbs the Shock?

The industrial consequences of the yttrium oxide supply disruption were not abstract. Aerospace manufacturers and semiconductor fabrication facilities both experienced documented production impacts during the period of restricted supply, as US News reported on the broader aerospace implications of the trade controls.

For aerospace manufacturers, the constraint was both technical and regulatory. Thermal barrier coatings must meet stringent aviation authority certification standards, and the substitution of alternative coating materials requires a complete re-certification process for affected components. This is not a matter of finding a comparable product on the market — it requires demonstrating to regulatory bodies such as the FAA or EASA that alternative materials meet the same safety and performance specifications under all operating conditions. The timeline for such re-certification is measured in years, not quarters. For manufacturers facing immediate production requirements, this timeline renders substitution commercially non-viable.

The semiconductor industry faced a different but equally acute version of the same problem. Plasma etch chamber coatings degrade incrementally during normal operation and require periodic replacement on a schedule driven by manufacturing throughput. Unlike a component that can simply be stockpiled when supply is available, the need for chamber coating replacement is tied directly to production volume. Fabs running at high utilisation rates consume coating materials on predictable schedules, meaning supply interruptions translate with minimal lag into production capacity constraints.

Why Yttrium Oxide Is Harder to Diversify Than Most Rare Earths

| Diversification Factor | Current Status |

|---|---|

| Alternative refined yttrium oxide producers outside China | Limited at commercial scale |

| US domestic yttrium oxide processing capacity | Essentially non-existent at the time of controls |

| Technically viable substitute materials for aerospace coatings | Not available without multi-year re-certification |

| Government strategic stockpile adequacy | Insufficient for extended supply interruptions |

| Allied supply chain alternatives (Japan, Australia, EU) | Dependent on Chinese refined oxide or early-stage alternatives |

A less commonly understood supply chain dynamic relates to the distinction between yttrium ore resources and refined yttrium oxide production. Yttrium occurs in nature primarily in monazite and xenotime mineral deposits, found across a geographically diverse range of countries including Australia, Canada, Brazil, India, and parts of Africa. The existence of yttrium-bearing mineral resources outside China is not, however, the same as having alternative supply of refined yttrium oxide. Converting raw ore into the high-purity oxide required for aerospace-grade coating applications requires processing infrastructure that China has developed over decades and that other countries have not yet replicated at commercial scale.

This gap between geological resource availability and refined production capacity is the central structural vulnerability. China's dominance is not primarily a geological accident — it reflects sustained investment in rare earth processing capability that created a concentration of refining expertise and infrastructure without close parallel elsewhere in the world.

The next major ASX story will hit our subscribers first

Yttrium Oxide in the Broader Critical Minerals Contest

The yttrium oxide episode illuminates a strategic dynamic that extends well beyond this single material. The broader critical minerals demand surge has amplified the stakes considerably, as China's selective approach to export controls demonstrates a sophisticated understanding of where supply chain leverage is most asymmetric and most durable.

Materials that serve aerospace and defence-adjacent applications occupy a uniquely sensitive position in trade leverage calculations. Disrupting these supply chains carries not just economic consequences but direct national security implications, creating a form of pressure that governments must treat with urgency regardless of their preferred trade policy posture. This is qualitatively different from restricting supply of materials used primarily in consumer electronics or renewable energy hardware.

The US policy response has acknowledged this reality. The $12 billion Project Vault initiative, reported by Mining.com on April 30, 2026, includes provisions for purchasing critical minerals from China as an interim measure while longer-term domestic production capacity is developed. The Export-Import Bank has indicated that this plan would later shift to a replenishment model prioritising domestic production. The inclusion of Chinese sourcing in the interim framework is a frank acknowledgment that domestic supply chain development cannot occur fast enough to address vulnerabilities that already exist. In addition, the US critical minerals tariff landscape continues to shape how these emergency procurement frameworks are designed and funded.

Comparative Positioning of Export-Controlled Rare Earths

| Rare Earth | Primary Industrial Application | Post-April 2025 Export Status | Price Response |

|---|---|---|---|

| Yttrium oxide | Aerospace coatings, semiconductor chambers | Remained tightly restricted through early 2026 | Approximately +6,900% over 12 months to February 2026 |

| Neodymium/Praseodymium | EV motors, wind turbines | Partially resumed post late-2025 truce | Elevated but less extreme |

| Dysprosium | High-performance magnets | Partially resumed | Elevated |

| Terbium | Magnets, phosphors | Partially resumed | Elevated |

Rare earth magnet exports to the US in January and February 2026 totalled 994 tonnes, down 22.5% year-over-year, indicating that broader rare earth trade tensions remain unresolved despite the late-2025 diplomatic engagement. The yttrium oxide situation therefore exists within a wider context of continuing rare earth trade friction rather than representing an isolated anomaly.

What Supply Chain Resilience for Yttrium Oxide Would Actually Require

Constructing genuine supply chain resilience for yttrium oxide is a more complex and time-consuming undertaking than is typically acknowledged in policy discussions. The challenge spans multiple distinct phases of the value chain, each requiring separate investment, regulatory approval, and capability development. Consequently, America's rare earth supply chain faces structural gaps that cannot be closed through diplomacy alone.

At the geological end of the chain, yttrium-bearing mineral deposits need to be identified, characterised, and brought into production. Countries including Australia, Canada, and several African nations host yttrium resources in commercially relevant concentrations. However, mineral resource availability does not automatically translate into permitted, funded, and operational mines. The permitting timeline for new mining operations in many western jurisdictions spans years, and the capital requirements for rare earth projects create financing challenges that are not trivially resolved.

Beyond mining, the most critical investment gap is in separation and refining infrastructure. Yttrium must be separated from the mixed rare earth concentrates produced by mining, purified to the specific purity grades required for aerospace-grade applications, and converted to the oxide form. Each of these steps requires chemical processing expertise, physical infrastructure, and process chemistry knowledge that China has accumulated over decades of rare earth processing investment. Replicating this capability requires deliberate policy support, patient capital, and realistic timelines measured in years rather than months.

Potential Policy Levers for Accelerating Diversification

-

Strategic stockpiling of yttrium oxide at government level to create buffer inventory against future supply interruptions, similar to the approach taken for petroleum through the Strategic Petroleum Reserve

-

Government-backed offtake agreements that reduce the commercial risk for investors in non-Chinese yttrium processing facilities, enabling project financing at scale

-

Allied supply chain development through coordination with Japan, Australia, and European nations that face comparable yttrium dependencies, potentially enabling shared processing infrastructure investment

-

Re-certification funding programmes that support aerospace manufacturers in testing and certifying alternative thermal barrier coating materials, reducing the multi-year timeline for substitution pathways

-

Domestic processing incentives through tax credits, loan guarantees, or direct investment in rare earth separation and refining facilities built to process North American and allied-nation ore concentrates

A speculative but analytically interesting possibility involves the role of recycling and secondary recovery in long-term yttrium supply. Yttrium oxide in spent turbine components and used semiconductor chamber linings is not permanently consumed — it can theoretically be recovered through material recycling processes. While yttrium recycling infrastructure is not currently developed at commercial scale in the US, investment in end-of-life material recovery could gradually reduce the intensity of primary yttrium oxide demand relative to industrial output. This pathway is likely a decade-scale development rather than a near-term solution.

Frequently Asked Questions: China Yttrium Oxide Exports to the US

What is yttrium oxide used for in aerospace?

Yttrium oxide is the primary input for producing yttrium-stabilised zirconia, the dominant material used in thermal barrier coatings applied to jet engine turbine blades and combustion components. These coatings allow engines to operate at temperatures that would otherwise rapidly destroy metallic components, making them essential for both commercial aviation and military aerospace systems. Without functional thermal barrier coatings applied to specification, aircraft certification requirements cannot be met.

Why did yttrium oxide prices increase so dramatically in 2025 and 2026?

China's April 2025 export licensing requirements effectively removed the world's dominant producer of refined yttrium oxide from accessible trade flows. Because no alternative suppliers exist at comparable scale, and because aerospace and semiconductor applications cannot substitute alternative materials without regulatory re-certification processes spanning multiple years, buyers competed for extremely limited available stock. Reuters reporting via Mining.com recorded a price increase of approximately 6,900% in the 12 months to February 2026.

Does the March 2026 shipment indicate the supply crisis has ended?

Not conclusively. While the 60-tonne March 2026 shipment represented the largest single China yttrium oxide export event in the post-controls period, cumulative US imports over the preceding 12 months remained 75% below prior-year levels even after this shipment was included. No other yttrium compounds or metals were shipped to the US in March 2026, suggesting the approval was specifically targeted rather than reflecting a broad policy relaxation.

Why is the US so dependent on Chinese yttrium oxide specifically?

The dependency reflects the difference between geological resource occurrence and refined production capacity. While yttrium-bearing minerals exist in multiple countries, China developed the processing infrastructure required to convert ore into aerospace-grade refined oxide over several decades of investment. The US had no significant domestic yttrium oxide processing capacity at the time controls were imposed, making import dependency structurally unavoidable in the short term.

Are other rare earths still restricted by China?

Broader rare earth trade flows partially resumed following a late-2025 US-China trade engagement, but yttrium remained among the most persistently restricted. Rare earth magnet exports to the US in January and February 2026 were still 22.5% below prior-year levels, indicating that the broader rare earth trade dispute had not been fully resolved even as some individual material flows resumed.

Key Takeaways

-

China yttrium oxide exports to the US declined approximately 75% year-over-year even after including the March 2026 partial resumption, representing one of the most severe critical mineral supply disruptions in recent US industrial history

-

The 6,900% price surge recorded in the 12 months to February 2026 reflects structural supply removal rather than demand-side pressure, with aerospace and semiconductor manufacturers unable to reduce consumption or substitute materials in the short term

-

China's selective retention of yttrium export restrictions, even while relaxing controls on other rare earth materials following a late-2025 trade truce, demonstrates deliberate material-level calibration of export leverage targeted at defence-adjacent industrial applications

-

The March 2026 60-tonne shipment should be interpreted as an individual diplomatic or commercial gesture rather than as evidence of sustained supply normalisation, given that it was confined to yttrium oxide alone and represented only a fraction of prior-year baseline volumes

-

Genuine supply chain resilience requires investment across the full yttrium oxide value chain, from mining through separation and refining to oxide production — a process involving realistic timelines measured in years and requiring coordinated government, industry, and allied-nation engagement

-

The yttrium oxide episode provides a template for how China may deploy precision export controls on other niche critical minerals with defence-adjacent applications in future trade disputes, making proactive supply chain diversification a strategic imperative rather than an optional policy enhancement

Disclaimer: This article contains forward-looking analysis, market interpretations, and scenario projections that involve assumptions and uncertainties. Price data referenced is sourced from Reuters via Mining.com (April 30, 2026). Readers should conduct independent research before making any investment or procurement decisions. Historical supply and price data may be subject to revision as customs statistics and commodity pricing records are updated.

Want To Stay Ahead Of The Next Critical Mineral Supply Shock?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including the rare earth and critical mineral sectors now at the centre of global supply chain disruption. Explore historic discoveries and their market returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the market.