May 15, 2026

Copper's New Geopolitical Reality: Why Mineral-Rich States Are Demanding a Bigger Seat at the Table

The copper beneath Zambia's soil has always been valuable. But in the context of a global economy scrambling to electrify everything from passenger vehicles to national power grids, that value has been fundamentally repriced. Each electric vehicle requires roughly 83 kilograms of copper. Every megawatt of solar capacity demands approximately 4.5 tonnes. Wind turbines, grid-scale storage systems, and transmission infrastructure all consume the metal at rates that dwarf traditional industrial applications. Against this backdrop, the governments of mineral-rich African nations are no longer content to watch that value flow predominantly to foreign shareholders.

This is the structural reality shaping the strategy of Zambia's state investment company, ZCCM Investments Holdings (ZCCM-IH), as it pursues a deliberate campaign to raise its equity positions across the country's mining sector. The Zambia state investment firm boost stakes in mines approach being taken is commercially sophisticated, diplomatically careful, and strategically timed to coincide with a period of peak critical minerals demand growth for the metals Zambia holds in abundance.

Understanding what ZCCM-IH is doing, how it is doing it, and what it means for the foreign mining groups operating across the Copperbelt requires both a technical grasp of mining governance and a clear-eyed view of the economic logic driving the push.

When big ASX news breaks, our subscribers know first

Understanding ZCCM-IH: Structure, Mandate, and Portfolio Scope

ZCCM-IH is not a regulator. It does not set royalty rates, grant exploration licences, or enforce environmental compliance. Its role is fundamentally commercial: to hold equity stakes in mining operations on behalf of the Zambian state and to generate returns from those positions through dividends, royalties, and capital appreciation.

The company's current portfolio spans a wide range of equity positions, from as low as 10% in some operations to 30% in others. Counterparties include some of the most significant names in global mining, among them China Nonferrous Metal Mining Group, Canada's First Quantum Minerals, and India's Vedanta Resources. The diversity of those relationships reflects decades of deal-making across different political eras, copper price cycles, and investment climates.

What makes the current moment distinct is that ZCCM-IH's leadership has articulated a clear directional intent: the minority stakes it currently holds are a floor, not a ceiling. The ambition is to move toward what the company's CEO, Kakenenwa Muyangwa, has described as significant minority positions, a threshold that carries governance implications far beyond the symbolic.

Why Stake Size Matters Beyond Percentages

In corporate governance terms, there is a meaningful distinction between a 10% position and a 25–30% position. Small minority shareholders are typically entitled to financial reporting and little else. Significant minority shareholders, by contrast, often cross thresholds that unlock board representation rights, veto powers over major capital expenditure decisions, and access to operational data that smaller shareholders are routinely excluded from.

For ZCCM-IH, moving from a 10% position to a 25–30% stake is therefore not a purely quantitative exercise. It is a qualitative shift in influence over how mines are operated, how capital is allocated, and how revenue is distributed. In a sector where operational decisions can span decades and involve billions of dollars in capital commitments, that influence carries enormous long-term value.

The Mechanics of ZCCM-IH's Ownership Strategy

Commercial Negotiation, Not Compulsion

The single most important signal in ZCCM-IH's stated approach is its explicit commitment to pursuing stake increases through commercial terms rather than forced acquisitions. This distinction matters enormously to the foreign capital that finances Zambia's mines. Furthermore, according to Mining Weekly, retrospective interference with ownership structures is the form of resource nationalism that most reliably destroys investment climates, as evidenced by the Democratic Republic of Congo's 2018 Mining Code reforms, which triggered significant operational disruptions and investor uncertainty across that country's copper sector.

Zambia's approach positions itself at the opposite end of that spectrum. By anchoring its ownership strategy to negotiated commercial frameworks, ZCCM-IH preserves credibility with international capital markets while still advancing the state's economic interests.

The Development-Stage Focus

ZCCM-IH has been explicit about where its ownership ambitions are concentrated: assets under development rather than operating mines. This is not simply a tactical choice but reflects a structural advantage the company possesses in pre-production negotiations.

At the development stage, mining projects are capital-hungry and commercially uncertain. The mining permit holder has significant leverage over the terms under which new partners are admitted. When ZCCM-IH holds the mining licence for a given deposit, it is entitled to negotiate a free carry stake before contributing any capital to project development.

Breaking Down the Free Carry Principle

A free carry stake is an equity interest granted to one party without requiring that party to contribute upfront capital proportionate to its ownership share. In practice, it means the licence holder can participate in project economics from the outset while the development partner funds the initial capital requirements.

ZCCM-IH has indicated that a free carry range of 5% to 15% represents an appropriate benchmark, with the precise level determined through negotiation on a case-by-case basis. This structure provides the company with meaningful equity exposure to new projects without depleting its own capital reserves, a particularly important consideration given ZCCM-IH's stated plans to raise external financing for its broader expansion programme.

Free Carry Stake Framework at a Glance:

| Scenario | ZCCM-IH Position | Free Carry Range |

|---|---|---|

| ZCCM-IH holds the mining licence | Entitled to equity before contributing capital | 5% to 15% |

| Third-party licence holder | Commercial negotiation required | Case-by-case |

| Existing minority stake in operating mine | Gradual increase via commercial terms | Varies by asset |

Recent Transactions: What ZCCM-IH Has Already Delivered

Strategic intent is meaningful only when paired with execution. ZCCM-IH's ownership push is not merely aspirational; it has already produced concrete results across two significant transactions.

Lubambe Copper Mines: A 50% Stake Increase

When Australian private equity firm EMR Capital exited its majority position in Lubambe Copper Mines in 2024, selling to China's JCHX Mining, ZCCM-IH used the shareholder transition as an opportunity to renegotiate its own position. The company raised its stake from 20% to 30%, a move that materially altered its governance standing within the operation and set a precedent for how shareholder transitions can be leveraged to advance the state's ownership interests.

Mingomba Mining: A KoBold Metals Partnership in Progress

The second active transaction involves Mingomba Mining, a development-stage copper project backed by KoBold Metals, the AI-driven mineral exploration company with prominent US investor backing. The government confirms that ZCCM-IH is currently in the process of raising its stake from 20% to 25%, a transaction that signals the company's willingness to engage with frontier technology-oriented mining investors on equal terms.

KoBold Metals has attracted significant attention for deploying machine learning algorithms across geological, geophysical, and geochemical datasets to identify copper deposits that traditional exploration methods may have overlooked. Its involvement in Zambia underscores both the country's geological prospectivity and the appeal of development-stage partnerships where state co-investment frameworks can be established early.

Recent ZCCM-IH Equity Movements:

| Asset | Previous Stake | New / Target Stake | Counterparty Context |

|---|---|---|---|

| Lubambe Copper Mines | 20% | 30% | EMR Capital exit; JCHX Mining acquires majority (2024) |

| Mingomba Mining | 20% | 25% (in progress) | KoBold Metals-backed development project |

The Royalty-to-Revenue Model: A Structurally Superior Cash Flow Architecture

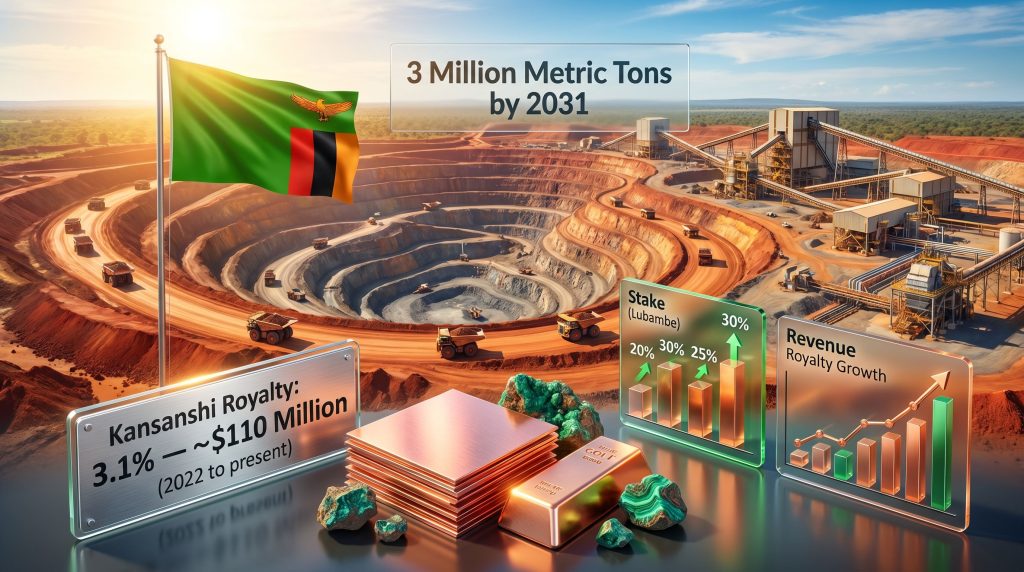

Perhaps the most technically innovative element of ZCCM-IH's strategy is its shift away from traditional dividend income toward revenue-based royalty arrangements. The model was pioneered at Kansanshi Mine in partnership with First Quantum Minerals, and its financial performance has been compelling enough to position it as a replicable template across other operations.

How the Kansanshi Model Works

Under the Kansanshi arrangement, ZCCM-IH holds a 20% equity stake and receives a 3.1% royalty on mine revenue in lieu of traditional equity dividends. Since 2022, this structure has delivered approximately $110 million to ZCCM-IH, representing a dependable income stream that has remained resilient through periods of copper price volatility and cost inflation.

The critical distinction between revenue royalties and dividends lies in where each sits within the financial waterfall of a mining operation. Dividends are paid after all operating costs, capital expenditures, interest payments, and tax obligations have been deducted from revenue. During periods of cost inflation or capital intensity, dividend payments to minority shareholders can be deferred, reduced, or eliminated entirely, even when the mine is generating substantial revenue at the top line.

Revenue royalties, by contrast, are calculated against gross mine revenue before any cost deductions. This means ZCCM-IH receives its 3.1% regardless of whether the mine's operating costs have risen, whether a capital expansion programme is underway, or whether the operator has chosen to retain earnings rather than distribute them as dividends.

A revenue royalty functions as a gross participation mechanism. The state investment vehicle receives cash flow based on what comes out of the ground and the price at which it is sold, not based on what the operator chooses to report as profit after managing its cost base. For a minority shareholder with limited operational control, this represents a fundamentally more secure income architecture than dividend dependency.

Kansanshi Royalty Model Performance Snapshot:

| Metric | Detail |

|---|---|

| ZCCM-IH Equity Stake | 20% |

| Revenue Royalty Rate | 3.1% of mine revenue |

| Cumulative Revenue Generated | Approximately $110 million (2022 to present) |

| Key Structural Advantage | Insulated from operating cost inflation |

| Dividend Relationship | Replaces traditional equity dividend distributions |

Why This Model Works in High-Inflation Mining Environments

The mining sector has faced persistent cost inflation since 2021, driven by elevated energy prices, labour cost increases, and supply chain disruptions affecting equipment and reagent procurement. In this environment, mines that are technically profitable at a revenue level may report compressed net margins that result in minimal or zero dividend distributions.

For a minority shareholder like ZCCM-IH, which has limited ability to influence cost management decisions, this creates an inherent tension between equity participation and actual cash receipt. The royalty model resolves this tension structurally, ensuring that the state captures value from production activity irrespective of the operator's cost management outcomes.

Capital Raising and the Road to Scaling the Model

ZCCM-IH has confirmed it is seeking to appoint a financial adviser to support capital raising for its expansion projects. This signals that the company intends to move beyond organic stake accumulation toward a more proactive investment strategy that requires external financing. The royalty-to-revenue model, with its predictable and inflation-protected cash flows, provides exactly the kind of stable revenue base that debt and equity capital markets look for when assessing a borrower's or issuer's capacity to service obligations.

Implications for Foreign Mining Investors Operating in Zambia

Mapping the Affected Operators

The mining groups most directly affected by ZCCM-IH's ownership push span three of the world's largest mining nations. China Nonferrous Metal Mining Group, Canada's First Quantum Minerals, and India's Vedanta Resources all have existing ZCCM-IH co-ownership arrangements that could be subject to gradual stake increases under the commercial negotiation framework. For each of these groups, the relevant question is not whether ZCCM-IH will seek to increase its position, but on what terms and under what timeline.

The Investor Sensitivity Matrix

Different aspects of ZCCM-IH's strategy carry different risk implications for foreign operators, and it is worth mapping these carefully. The copper supply crunch adds further urgency to how mining geopolitics plays out across the Copperbelt:

| Factor | Implication for Foreign Operators |

|---|---|

| Stake increase via commercial terms | Manageable; priceable into deal structures |

| Free carry demands on new licences | Reduces effective equity for development partners |

| Royalty-over-dividend model adoption | Reduces operator cash flow flexibility at the revenue line |

| No forced acquisition of operating mines | Positive signal for investment climate stability |

| Focus on development-stage assets | Higher negotiation exposure for new market entrants |

Negotiated Dilution vs. Regulatory Expropriation

The conceptual distinction between negotiated dilution and regulatory expropriation is not semantic. It maps directly to how international arbitration tribunals and risk-rating agencies assess a country's investment climate. Zambia's explicit commitment to commercial negotiation frameworks, its track record of honouring existing contracts, and its focus on pre-production assets rather than retrospective interference with producing mines all contribute to a materially different risk profile compared to jurisdictions that have pursued more confrontational approaches.

For capital allocators assessing exposure to Zambian copper projects, the relevant benchmark is not the DRC's 2018 Mining Code experience but rather Botswana's Debswana model, where state co-ownership through commercial partnership has coexisted with consistent foreign investment inflows and long-term contract stability. Consequently, understanding mining geopolitics is essential for investors seeking to navigate these dynamics effectively.

The next major ASX story will hit our subscribers first

Zambia's 3 Million Metric Ton Ambition: What It Actually Requires

The Scale of the Production Challenge

Zambia currently produces approximately 750,000 metric tons of copper annually, positioning it as Africa's second-largest copper producer behind the Democratic Republic of Congo. The Zambia copper production forecast targets 3 million metric tons by 2031, implying more than a quadrupling of output over approximately five years — a rate of expansion that has few historical precedents in the global copper industry.

For context, Chile, the world's largest copper producer, required four decades to build the infrastructure, processing capacity, and water management systems needed to sustain production above 5 million metric tons annually. Zambia is attempting to achieve a comparable proportional expansion in a fraction of that timeframe.

What Tripling Output Demands

Meeting the 2031 target requires simultaneous progress across multiple fronts:

- Power generation capacity of an estimated 1,200 additional megawatts to support expanded mine operations and processing facilities

- Transportation and logistics infrastructure, including rail upgrades and port access improvements to handle significantly higher copper concentrate and refined copper volumes

- Water resource management frameworks capable of sustaining expanded SX-EW (solvent extraction-electrowinning) and flotation processing operations in a region increasingly subject to climate variability

- Technical workforce development at scale, with particular demand for process engineers, metallurgists, and automation specialists

- Foreign direct investment of an estimated $6 to $8 billion across new and expanded operations over the target period

ZCCM-IH as a Capital Mobiliser

Within this framework, ZCCM-IH's role extends beyond passive equity participation. By establishing credible commercial co-investment structures, developing replicable revenue-sharing models, and demonstrating governance competence through executed transactions at Lubambe and Mingomba, the company is positioning itself as a legitimate partner that can attract and retain the foreign capital needed to fund Zambia's production ambitions.

Zambia's production target is not simply an industrial aspiration. It is a statement about where the country intends to position itself within the global critical minerals supply chain as clean energy demand accelerates. ZCCM-IH's ownership strategy is the institutional mechanism through which Zambia intends to ensure that the economic returns from that position accrue meaningfully to the Zambian state rather than exclusively to foreign shareholders.

Frequently Asked Questions: Zambia State Investment Firm Boosting Stakes in Mines

What is ZCCM-IH and what role does it play in Zambia's mining sector?

ZCCM-IH, or ZCCM Investments Holdings, is Zambia's state investment company with equity positions across numerous copper and related mineral operations. Unlike a regulatory body, it functions as a commercial shareholder, holding minority stakes and generating returns through dividends, revenue royalties, and capital appreciation. Its mandate includes both financial return generation for the Zambian state and the broader objective of ensuring Zambia captures greater economic value from its mineral resources.

Is Zambia forcing mining companies to give up equity stakes?

No. ZCCM-IH has explicitly confirmed that all stake increases are pursued through commercial negotiation rather than forced sales or regulatory compulsion. The company has also stated it has no intention of taking ownership of operating mines in which it currently holds no shareholding. The focus is entirely on commercially agreed arrangements, primarily targeting assets still in the development phase.

What is the royalty-to-revenue model and how does it benefit ZCCM-IH?

The royalty-to-revenue model replaces traditional equity dividend distributions with a percentage royalty calculated against gross mine revenue. At Kansanshi, ZCCM-IH receives 3.1% of revenue in exchange for its 20% equity stake, generating approximately $110 million since 2022. The structural benefit is that royalty payments are made before operating costs are deducted, protecting the state's income stream during periods of cost inflation or capital-intensive investment cycles when dividends might otherwise be reduced or suspended.

Which mines are currently subject to ZCCM-IH stake increases?

Two active transactions have been confirmed. Lubambe Copper Mines has already seen ZCCM-IH increase its position from 20% to 30% following EMR Capital's exit in 2024. Mingomba Mining, backed by KoBold Metals, is currently the subject of an ongoing stake increase from 20% to 25%.

What is a free carry stake and when does ZCCM-IH claim one?

A free carry stake is an equity interest granted to a party without requiring that party to contribute proportionate upfront capital. ZCCM-IH asserts this right in situations where it already holds the mining licence for a deposit being developed in partnership with a third-party investor. In these cases, the company considers itself entitled to a free carry position of between 5% and 15% before any capital contributions are required, with the precise level determined through negotiation.

How does Zambia's resource ownership strategy compare to other African nations?

Zambia's approach occupies a relatively measured position on the spectrum of African resource nationalism. It prioritises commercial negotiation over regulatory compulsion, focuses on pre-production assets rather than retrospective interference with producing operations, and maintains existing contractual frameworks with current mine operators. In addition, those considering copper investment strategies will find Zambia's model presents a meaningfully different risk profile compared to more confrontational approaches seen elsewhere on the continent.

Key Takeaways: What ZCCM-IH's Ownership Push Signals for Zambia's Mining Sector

The Zambia state investment firm boost stakes in mines strategy delivers a clear set of signals for investors, operators, and policymakers alike. Furthermore, as the broader sector grapples with supply constraints, understanding this framework becomes increasingly critical:

- Commercial, not coercive: All stake increases are being pursued through negotiated commercial frameworks, preserving Zambia's investment climate standing with international capital markets

- Revenue model innovation: The royalty-over-dividend structure at Kansanshi has generated over $110 million since 2022 and is being actively positioned as a replicable template for other operations

- Development-stage leverage: ZCCM-IH is concentrating its equity push on pre-production assets where licence ownership provides a structural negotiating advantage, including a free carry range of 5% to 15%

- Executed transactions: Stake increases at Lubambe (20% to 30%) and Mingomba (20% to 25% in progress) demonstrate the company's ability to convert strategic intent into completed deal outcomes

- Scale ambition: The 3 million metric ton copper output target by 2031 frames ZCCM-IH's ownership expansion as a national industrial policy instrument, not merely a financial portfolio management exercise

- Investor signal: The explicit rejection of forced acquisition from operating mines represents a deliberate effort to balance the state's economic interests with the foreign direct investment environment required to fund Zambia's production ambitions

This article is for informational purposes only and does not constitute financial, investment, or legal advice. Readers should conduct independent due diligence before making any investment decisions related to mining companies, critical mineral markets, or Zambian equities. Production targets, financial projections, and royalty figures cited are based on publicly reported information and are subject to change.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model instantly alerts subscribers to significant ASX mineral discoveries across 30-plus commodities, turning complex geological data into clear, actionable investment insights — explore how historic mineral discoveries have delivered extraordinary returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the market.