June 19, 2026

The Infrastructure Equation Rewriting Africa's Critical Minerals Future

For decades, the prevailing assumption in development economics was that agricultural investment and industrial resource extraction existed on separate policy tracks, requiring separate funding streams, separate institutions, and separate timelines. That assumption is now being systematically dismantled across sub-Saharan Africa, where the Zambia US agricultural grant critical minerals supply chain has become a focal point for rethinking how development finance can serve multiple strategic objectives simultaneously.

Zambia sits at the epicentre of this rethink. The country's most productive farming regions and its most valuable mining provinces share many of the same rural road networks, the same logistics chokepoints, and the same export bottlenecks. Recognising this structural reality, both the Zambian government and its American development finance partners have moved to formalise what the terrain has always implied: that a road built to move maize can also move copper concentrate.

Furthermore, the economics of both improve dramatically when that dual-use potential is deliberately engineered into project design from the outset. The growing critical minerals demand driven by the global energy transition has made this convergence not just sensible but strategically urgent.

When big ASX news breaks, our subscribers know first

Rethinking the MCC Compact: From Farm-to-Market to Mine-to-Port

The Millennium Challenge Corporation (MCC) Zambia Compact II, valued at $491.75 million, was formally signed in 2024 and originally structured to address persistent weaknesses in Zambia's agricultural productivity and market access. Its foundational pillars targeted the specific friction points that keep smallholder farmers disconnected from buyers:

- Rural road rehabilitation to reduce haulage times and post-harvest losses

- Irrigation infrastructure upgrades to improve yield reliability

- Post-harvest storage and cold-chain logistics to extend the commercial life of perishable crops

- Agro-processing equipment and facilities to capture more value domestically

- Agricultural policy reform and institutional capacity strengthening

The MCC operates on a performance-based disbursement model, which distinguishes it fundamentally from conventional foreign aid. Recipient governments must meet and sustain governance, anti-corruption, and policy benchmarks throughout the compact's lifespan. The fact that Zambia qualified for a second compact of this scale reflects a substantive assessment of the country's institutional trajectory rather than a routine diplomatic gesture.

What changed in 2025 and 2026 was not the compact's budget or its governance framework, but the spatial targeting of its infrastructure components. Zambia's Ministry of Finance confirmed an agreement with the MCC to redirect portions of the road rehabilitation funding toward corridors in the Copperbelt and North-Western provinces that serve overlapping agricultural and mineral export functions.

This is a co-investment logic rather than a diversion: the same kilometre of rehabilitated road that reduces a farmer's journey to market also lowers the haulage cost per tonne of copper concentrate moving toward a rail connection.

This model of deliberate infrastructure convergence represents a meaningful evolution in how development finance institutions are beginning to think about return on investment across multiple economic sectors simultaneously, rather than optimising for a single-sector outcome in isolation.

The Lobito Corridor: Why $6 Billion Is Flowing Into One Transport Route

Understanding why the MCC compact realignment matters requires understanding the broader infrastructure ecosystem it is designed to plug into. The Lobito Corridor is a transcontinental multimodal transport route that connects the mineral-rich interiors of Zambia and the Democratic Republic of Congo to Angola's Atlantic-facing port of Lobito.

For landlocked copper and cobalt producers, the corridor offers something that has historically been extraordinarily difficult to achieve: reliable, lower-cost access to ocean freight routes serving European and North American buyers. Global financial commitments to Lobito Corridor infrastructure have now surpassed $6 billion, drawn from a diverse consortium including Western governments, multilateral development banks, and private sector infrastructure partners.

| Infrastructure Metric | Detail |

|---|---|

| Total corridor commitments | Over $6 billion |

| Primary minerals transported | Copper, cobalt, manganese |

| Terminal port | Lobito, Angola (Atlantic Ocean) |

| Primary beneficiary nations | Zambia, DRC, Angola |

| Railway expansion financial close target | Q4 2027 (African Finance Corporation) |

The African Finance Corporation (AFC) is spearheading the railway expansion segment that would connect Zambia's Copperbelt directly into the broader corridor network. The AFC has indicated it is targeting financial close for this railway component in Q4 2027, a timeline that aligns closely with the MCC compact's implementation phases.

Why the Corridor Has Become a Geopolitical Priority

The Lobito Corridor's strategic importance extends well beyond logistics efficiency. Western governments and corporations have watched with growing concern as Chinese state-owned enterprises and sovereign wealth vehicles have embedded themselves deeply into African mineral supply chains. This cobalt supply rivalry between the US and China has intensified dramatically, often through preferential rail access, port concessions, and long-term offtake arrangements that effectively route strategic minerals through Chinese-controlled infrastructure before they reach global commodity markets.

The corridor represents the most credible Western-backed alternative to this architecture. Copper and cobalt moving through Lobito can reach Atlantic shipping lanes without passing through any Chinese-controlled logistics node, giving Western buyers a degree of supply chain sovereignty that current routing arrangements frequently cannot provide.

These metals are not discretionary inputs. They are structurally essential for:

- Electric vehicle battery cathodes and current collectors

- Grid-scale energy storage systems supporting renewable power expansion

- Consumer electronics, industrial motors, and defence electronics

- Offshore wind turbine generators and subsea power cables

The USTDA Parallel Track: Moving From Infrastructure to Processing

The MCC compact is not the only American instrument operating in Zambia's critical minerals space. The U.S. Trade and Development Agency (USTDA) has separately awarded approximately $1.4 million to fund a feasibility study for expanding the copper and cobalt processing capacity of Metalex Africa Zambia Limited. While the MCC investment addresses the logistics layer of the supply chain, the USTDA grant targets the extraction and processing layer directly.

If the feasibility study progresses favourably toward full development, the expanded facility could contribute up to 25,000 additional metric tons of copper and cobalt concentrates annually. The USTDA has framed this investment explicitly as a mechanism to diversify American access to critical mineral inputs and reduce dependency on supply chains that route through geopolitically concentrated processing infrastructure.

Comparing the Two Active U.S. Instruments in Zambia

| Programme | Agency | Value | Primary Focus | Minerals Relevance |

|---|---|---|---|---|

| MCC Zambia Compact II | Millennium Challenge Corporation | $491.75 million | Agriculture, rural roads, logistics | Indirect via shared infrastructure |

| Metalex Feasibility Study | U.S. Trade and Development Agency | ~$1.4 million | Copper/cobalt processing expansion | Direct supply chain diversification |

The simultaneous deployment of these two instruments across different layers of the same value chain reflects a coordinated approach by Washington to establish durable economic footholds in Zambia's resource economy. Infrastructure and processing capacity are the two most capital-intensive barriers to supply chain participation, and American development agencies are now addressing both in parallel.

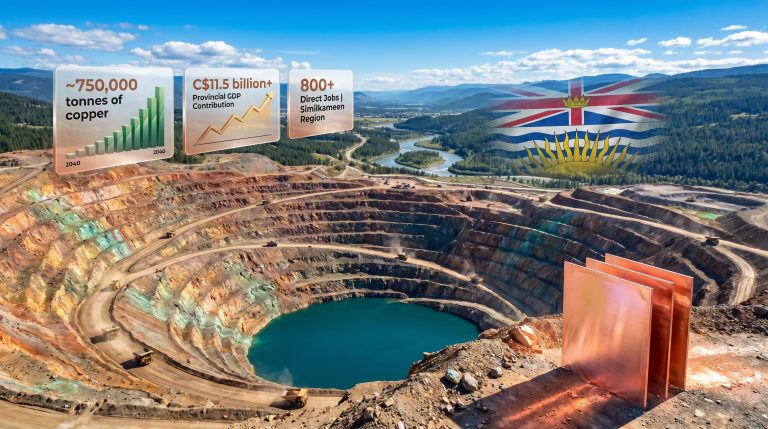

Zambia's Copper Geology and Why Grade Matters

A dimension of this story that rarely receives adequate attention in policy discussions is the underlying geological quality of Zambia's copper deposits. Zambia sits within the Central African Copperbelt, a sediment-hosted stratiform copper province stretching across the border into the DRC that ranks among the highest-grade copper-bearing geological formations on Earth.

Zambia copper production statistics consistently demonstrate ore grades significantly above the global average for open-pit copper mines. While global average copper grades for new mines have been declining steadily over recent decades as high-grade resources are depleted, Zambia's established mining districts and several emerging operations in the North-Western Province maintain grades that support competitive economics even in lower copper price environments.

This geological endowment has a direct bearing on the infrastructure investment thesis. Higher-grade deposits generate more copper per tonne of ore processed, which means the economic return on each kilometre of road, each rail connection, and each port slot is structurally higher in Zambia than in many competing copper jurisdictions. Infrastructure investment in Zambia is not just unlocking access to copper; it is unlocking access to high-quality copper at scale.

Cobalt, produced as a by-product of copper mining across this geological province, adds a further dimension of value. The Copperbelt's cobalt co-production profile means that infrastructure investments are effectively monetising two critical minerals simultaneously, improving the financial case for corridor development well beyond what a copper-only analysis would suggest.

Zambia's Sovereignty Stance and the New African Negotiating Posture

One of the more significant, and underreported, aspects of Zambia's engagement with Western development finance is the firmness with which the government has defended its resource sovereignty. Zambia has explicitly rejected any framework that would grant American firms or institutions preferential access to its mineral resources as a condition of receiving infrastructure finance or technical cooperation.

Reports have also surfaced suggesting that Washington explored potential linkages between health-related aid mechanisms and mineral access discussions, a conditionality approach that Zambia pushed back against publicly. The government's position is that critical minerals cooperation must preserve national control over resource allocation decisions and avoid creating the kind of asymmetric dependency relationships that characterised earlier eras of African engagement with external powers.

This stance is not unique to Zambia. It reflects a broader pattern emerging across resource-rich African nations, where governments are increasingly sophisticated in distinguishing between welcome capital and unwelcome conditions, and in leveraging competitive interest from multiple great powers to extract better terms from all of them.

Consequently, Zambia currently sits at the intersection of competing U.S., Chinese, and European strategic interests. The broader mining geopolitics reshaping the global resources sector are acutely visible here, where China maintains deep operational ties to the Zambian mining sector through state-owned enterprise investments and long-term offtake agreements built up over multiple decades.

The U.S. is deploying concessional finance and development grants rather than equity stakes as its primary engagement tool, a model that avoids the ownership friction that has complicated Chinese investment relationships in several African countries. As Western demand for copper intensifies in the run-up to peak electric vehicle production volumes expected through the late 2020s and 2030s, Zambia's negotiating leverage is structurally increasing.

The next major ASX story will hit our subscribers first

The Dual-Benefit Infrastructure Model in Practice

Road network improvements in Zambia's key provinces create value that compounds across multiple economic actors simultaneously. The financial logic of dual-purpose infrastructure is straightforward but frequently underappreciated in conventional development finance assessments.

Agricultural beneficiaries of improved road networks:

- Smallholder farmers reduce journey times to markets, lowering fuel costs and improving margins on low-value-per-kilogram crops

- Post-harvest loss rates decline as perishable produce reaches buyers before spoilage thresholds are reached

- Agro-processors can source raw materials from a wider geographic catchment, improving plant utilisation rates

- Rural communities gain improved access to health services, schools, and financial institutions, generating social return on investment

Mining and minerals beneficiaries of the same road improvements:

- Copper and cobalt concentrates can be transported to rail connections more quickly and at lower per-tonne cost

- Reduced haulage costs improve project economics for lower-grade or marginal mining operations that might otherwise be uneconomic

- Improved road access accelerates greenfield exploration timelines by making drill sites accessible in wet seasons

- Junior mining companies, which typically have less capital for private road construction, gain access to deposits that were previously too remote to develop

Scenario Analysis: What a Fully Integrated Corridor Means by 2030

If the AFC railway expansion achieves its targeted financial close in Q4 2027, and MCC-funded road upgrades across the Copperbelt and North-Western provinces are completed on schedule, the cumulative infrastructure effect by approximately 2030 would be material. The anticipated copper supply crunch makes these timelines particularly consequential for global commodity markets:

- Copper export volumes increase as transport cost reductions improve the economics of mines currently constrained by logistics rather than geology

- Agricultural exports gain corridor access, allowing North-Western Province producers to compete in Atlantic-facing commodity markets for the first time

- Western buyers secure diversified supply, reducing reliance on Chinese-controlled logistics for copper and cobalt sourcing

- Zambia's fiscal position strengthens as mining royalties and corporate taxes grow on higher throughput volumes

- Greenfield development accelerates as infrastructure risk, one of the primary deterrents to junior mining investment in landlocked jurisdictions, is substantially reduced

Disclaimer: The scenario above represents an analytical projection based on publicly available infrastructure timelines and economic assumptions. Actual outcomes will depend on execution timelines, commodity price movements, geopolitical developments, and financing conditions that cannot be predicted with certainty. This article does not constitute financial or investment advice.

Key Takeaways: What the Zambia US Agricultural Grant Critical Minerals Expansion Signals

The deliberate broadening of the MCC compact's mandate carries implications that extend well beyond Zambia's borders. Several structural signals are worth noting:

- Development finance is evolving. The co-design of agricultural and industrial infrastructure objectives within a single compact represents a meaningful departure from the sector-siloed models that have dominated multilateral development banking for decades.

- Zambia is playing a sophisticated long game. By positioning shared infrastructure as the point of leverage rather than resource concessions, the government is extracting maximum investment value while preserving sovereign control over mineral allocation that domestic politics increasingly demands.

- The Lobito Corridor ecosystem is approaching critical mass. With over $6 billion committed and a railway financial close targeted for 2027, the corridor is transitioning from a strategic concept to an operational reality.

- The USTDA feasibility study is a seed investment, not a ceiling. A $1.4 million grant funding 25,000 additional metric tons of potential annual concentrate output represents an extraordinarily high return on public investment if the project advances to full development.

- Africa's negotiating posture is permanently changed. Zambia's willingness to accept U.S. development finance while rejecting preferential access conditions signals a new baseline for how resource-rich African governments will engage with all external partners seeking supply chain alignment in the critical minerals era.

Further context on U.S.-Africa critical minerals policy and the Lobito Corridor's development trajectory is available through Business Insider Africa at africa.businessinsider.com.

Want to Track ASX Discoveries in the Critical Minerals Driving This Global Supply Chain Race?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, instantly translating complex geological and commodity data into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their remarkable returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.