May 16, 2026

The Industrial Policy Logic Reshaping Global Mineral Supply Chains

For decades, the prevailing assumption in global commodity markets was straightforward: resource-rich developing nations would mine it, and industrialised nations would refine it. That assumption is now under sustained attack. From Southeast Asia to Latin America to sub-Saharan Africa, mineral-endowed governments are deploying export restrictions not as protectionist gestures but as calculated instruments of industrial policy, designed to capture the value-added margins that have historically flowed elsewhere.

Zimbabwe's decision to immediately prohibit the export of unbeneficiated minerals and raw lithium concentrates, announced on February 25, 2026, sits squarely within this broader global realignment. The Zimbabwe lithium export ban is particularly consequential not because of the policy itself — which follows a template established most visibly by the indonesia nickel boom — but rather because of the country's specific position within the lithium supply chain that underpins global battery manufacturing.

When big ASX news breaks, our subscribers know first

Zimbabwe's Mineral Endowment and the Scale of Its Leverage

Zimbabwe holds a mineral portfolio that extends well beyond lithium, encompassing platinum group metals (PGMs), diamonds, chrome, and coal. Yet it is lithium, specifically spodumene, the hard-rock lithium mineral that dominates battery-grade chemical production, where Zimbabwe's geopolitical weight is most pronounced.

According to the Minerals Marketing Corporation of Zimbabwe (MMCZ), Zimbabwe supplies roughly 15% of the spodumene concentrate imported into China, the world's dominant lithium chemical processor and battery manufacturer. That figure is significant. China processes the overwhelming majority of the world's battery-grade lithium chemicals, and its domestic lithium resources, while substantial, cannot independently satisfy the demand generated by its battery manufacturing industry. Zimbabwe therefore occupies a structurally meaningful node in a supply chain with very little slack.

A 15% share of China's spodumene import volume is not peripheral exposure. For a supply chain operating with limited geographic redundancy, it represents a genuine concentration risk, and Zimbabwe's policymakers appear to understand this leverage precisely.

It is important, however, to distinguish between geological endowment and operational capacity. Zimbabwe's lithium reserves are real and commercially extractable, but the infrastructure required to convert spodumene ore into battery-grade lithium hydroxide or lithium carbonate — the compounds that battery manufacturers actually require — remains underdeveloped domestically. The export ban is, in one sense, a policy forcing function designed to close this gap through foreign direct investment and partnership arrangements.

What the Export Ban Actually Prohibits and How It Works

The Zimbabwe lithium export ban is not sector-specific. It applies to all unbeneficiated minerals, meaning raw or minimally processed ore that has not undergone meaningful value-addition on Zimbabwean soil. Lithium concentrate, the product most directly affected, is the output of crushing, grinding, and froth flotation of spodumene-bearing ore, producing a concentrate typically grading between 5% and 7% lithium oxide (Li₂O). This concentrate is what China's chemical processors import and convert into battery-grade compounds.

The processing stages between raw ore and a usable battery input are worth understanding in some detail:

- Mining and crushing of spodumene-bearing pegmatite ore

- Flotation concentration to produce spodumene concentrate (typically 5–7% Li₂O)

- Calcination and acid roasting to convert alpha-spodumene to beta-spodumene

- Leaching and purification to produce lithium sulphate solution

- Conversion to lithium carbonate (Li₂CO₃) or lithium hydroxide monohydrate (LiOH·H₂O)

- Battery-grade refinement to achieve the purity specifications required by cell manufacturers

Zimbabwe's export ban intervenes at stage two, prohibiting the export of spodumene concentrate and requiring that downstream processing occurs domestically before product can be sold internationally. Export exemptions may be granted under specific conditions, with MMCZ serving as the primary regulatory and compliance authority.

The policy was accelerated significantly from its original January 2027 implementation date, with the government citing concerns about alleged mineral leakages, export surges ahead of the deadline, and stockpiling behaviour by producers seeking to maximise concentrate shipments before restrictions took effect. Furthermore, Reuters reported that Zimbabwe would introduce export quotas alongside stringent conditions for any resumption of shipments, adding another layer of regulatory complexity for international buyers.

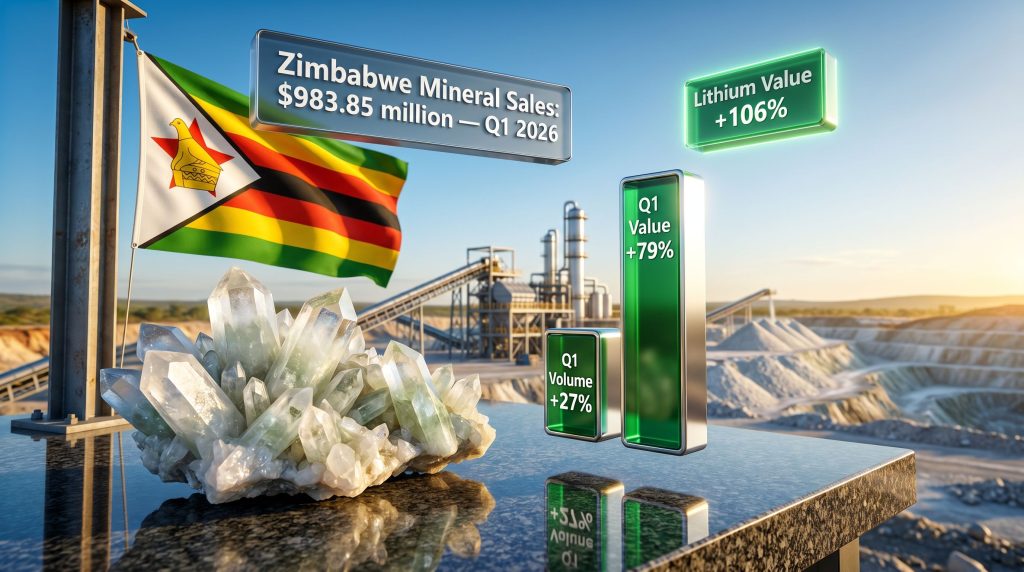

Q1 2026 Performance Data: The Numbers Behind the Policy

The first quarter of 2026 produced the earliest empirical test of whether the Zimbabwe lithium export ban was achieving its intended objectives. The results, as reported by the MMCZ and published by Business Insider Africa, were striking.

| Metric | Q1 2026 | Year-on-Year Change |

|---|---|---|

| Total mineral sales volume | 1,288,761 tonnes | +27% |

| Total mineral sales value | $983.85 million | +79% |

| Lithium sales volume | 240,826 tonnes | +2% |

| Lithium sales value | $178.64 million | +106% |

| PGM export earnings | $543.97 million | Significant increase |

The most analytically revealing figure in this dataset is not the headline revenue number but the divergence between volume and value growth in lithium. A 2% increase in volume accompanied by a 106% surge in value is not primarily a price story. It reflects a fundamental change in what Zimbabwe is selling. When raw concentrate is replaced by semi-processed or processed lithium compounds, the per-tonne revenue increases dramatically because the value addition has occurred within Zimbabwe's borders rather than in a Chinese refinery.

This is the economic logic of beneficiation made tangible in a single quarter's data.

PGMs contributed $543.97 million in export earnings, with concentrate volumes nearly doubling despite a decline in matte volumes — a bifurcation that reflects the prioritisation of concentrate processing over smelted output in the near term. Steel products, coal, and coke also recorded strong gains, consistent with broader regional demand improvement and the policy's value-addition emphasis across the mineral sector.

The one meaningful outlier was diamonds, which remained under pressure due to weaker global prices and intensifying competition from laboratory-grown stones. This structural challenge in the diamond sector is worth examining closely, because it offers a cautionary analogy for lithium policy planning.

The Diamond Sector as a Cautionary Analogy

Could Synthetic Substitution Undermine Zimbabwe's Lithium Strategy?

Zimbabwe's diamond industry faces a problem that export bans cannot solve: synthetic substitution. Laboratory-grown diamonds, produced through chemical vapour deposition or high-pressure high-temperature processes, have compressed natural diamond prices substantially over recent years. The value of a geological monopoly erodes rapidly when the product can be manufactured at industrial scale.

This raises a legitimate, if speculative, question for Zimbabwe's lithium strategy. Battery chemistry is not static. Sodium-ion batteries, solid-state architectures, and lithium-free chemistries are all progressing through various stages of commercial development. If any of these technologies achieves cost-competitive mass deployment within the next decade, the lithium demand growth profile for spodumene-derived lithium compounds could face structural pressure analogous to what natural diamonds have experienced.

This does not undermine the near-term logic of Zimbabwe's export ban, but it does argue for urgency in converting policy leverage into physical processing infrastructure before the demand window is fully open.

Global Precedents: What Other Resource Nationalism Cases Reveal

Zimbabwe's policy did not emerge in isolation. It is part of a recognisable and accelerating pattern across mineral-endowed developing nations.

| Country | Mineral | Policy Type | Year Introduced | Key Outcome |

|---|---|---|---|---|

| Indonesia | Nickel | Full export ban on raw ore | 2020 | Domestic processing investment surge; WTO dispute filed by EU |

| Chile | Lithium | State participation mandate | 2023 | Strategic partnership model with private operators |

| Democratic Republic of Congo | Cobalt | Export levies and processing incentives | Ongoing | Mixed results constrained by infrastructure gaps |

| Zimbabwe | All unbeneficiated minerals | Immediate export ban | February 2026 | 79% Q1 revenue increase; supply chain disruption |

Indonesia's experience is the most studied precedent. Its nickel ore export ban generated a wave of foreign investment in domestic smelting and processing capacity, particularly from Chinese firms seeking to protect their supply positions. The European Union challenged the ban at the WTO, arguing it constituted an unfair trade restriction, though Indonesia largely prevailed in maintaining its policy framework. The key lesson for Zimbabwe is that the policy can attract downstream capital, but only when the geological endowment is sufficiently attractive and the regulatory environment sufficiently stable to justify long-horizon investment decisions.

The next major ASX story will hit our subscribers first

Supply Chain Disruption and China's Exposure

The immediate market consequence of the Zimbabwe lithium export ban was supply chain disruption. Minerals already in transit at the time of the February 25 announcement were caught by the policy, creating short-term sourcing gaps for Chinese battery-grade chemical producers who had been operating on the assumption of continued spodumene concentrate flows. In addition, Benchmark Mineral Intelligence noted that any resumption of exports would come with stringent conditions, further complicating near-term supply planning for downstream buyers.

Industry price reporting service Fastmarkets assessed that the ban was expected to reduce spot spodumene availability and tighten near-term supply for Asian processors, consistent with what one would expect when a supplier representing roughly 15% of China's import volume abruptly changes the terms of its exports.

MMCZ General Manager Dr. Nomusa Moyo characterised the policy's medium-term objective clearly: while acknowledging the short-term disruption to global spot supplies, she noted that the ban has consolidated Zimbabwe's strategic influence over the global battery supply chain by incentivising domestic processing, and reiterated Zimbabwe's position as a critical partner for leading battery manufacturers given its material share of China's spodumene import volumes. (Business Insider Africa, Solomon Ekanem, 17 May 2026)

The question for downstream buyers is whether to wait for Zimbabwean processing capacity to develop, renegotiate supply terms, or accelerate sourcing from alternative spodumene producers in Australia, Canada, and Brazil. Each option carries cost and timeline implications. Consequently, the pressure on critical minerals demand planning has intensified considerably across both Asian and Western markets.

The Infrastructure Gap: Where Policy Ambition Meets Physical Reality

The most significant structural challenge facing Zimbabwe's beneficiation mandate is the mismatch between the policy's ambition and the country's current processing infrastructure. Converting spodumene concentrate into battery-grade lithium hydroxide requires specialised chemical processing facilities, stable power supply, water access, technical expertise, and logistics infrastructure — none of which exist at meaningful scale in Zimbabwe today.

The risks this creates are threefold:

- Production gaps: Mining operations may slow or stockpile if export channels are blocked and domestic processing cannot absorb output

- Investment uncertainty: Foreign capital required to build processing capacity may be deterred by governance, currency, and sovereign risk perceptions

- Revenue timing misalignment: The Q1 2026 value surge partly reflects the transition period; sustaining it requires processing investment that has not yet fully materialised

This is not an argument against the policy, but a reminder that the gap between regulatory intent and physical capacity is the critical variable determining whether Zimbabwe's bet on beneficiation pays off over a five to ten year horizon. Innovations such as direct lithium extraction technology could, however, offer a pathway to accelerate domestic processing timelines if adopted at scale.

Western Critical Mineral Strategies and Zimbabwe's Position

How Does Zimbabwe Fit Into Western Supply Chain Frameworks?

The United States, European Union, and Japan are each advancing frameworks to secure supply chains for battery materials outside of China-dominated channels. The US Inflation Reduction Act (IRA), for example, contains provisions that favour battery materials sourced from free trade agreement partners or domestically processed. The EU's Critical Raw Materials Act establishes strategic stockpiling and diversification objectives.

Zimbabwe's sovereign policy choices, including the export ban, create a complex dynamic for Western supply chain planners. On one hand, processed Zimbabwean lithium compounds would be more compatible with Western downstream manufacturing requirements than raw concentrate. On the other hand, Europe's critical minerals supply chain planners face governance risk perceptions that complicate Zimbabwe's integration into Western-aligned corridors. The EU's Carbon Border Adjustment Mechanism (CBAM) adds another layer of complexity, as the carbon intensity of Zimbabwean processing infrastructure will influence the competitiveness of its exports in European markets.

Q2 2026 Outlook and the Risks Ahead

The MMCZ has signalled a mixed outlook for the second quarter of 2026, citing geopolitical tensions and energy market disruptions as the primary variables influencing global commodity prices, particularly for critical minerals used in industrial and defence applications. This cautious framing reflects genuine uncertainty.

Several risk factors warrant monitoring:

- Commodity price volatility for spodumene and lithium chemicals, which have already experienced significant cycles

- Buyer diversification by Chinese processors toward Australian and Latin American supply

- Processing investment timelines and whether announced downstream projects proceed on schedule

- Broader macroeconomic conditions affecting battery demand growth and electric vehicle adoption rates

FAQ: Zimbabwe Lithium Export Ban

What minerals does Zimbabwe's export ban cover?

The ban applies to all unbeneficiated minerals, including raw lithium concentrates. Processed and semi-processed outputs remain exportable subject to MMCZ compliance conditions.

When did the ban take effect?

It was implemented immediately on February 25, 2026, applying even to minerals already in transit, representing a nearly two-year acceleration from the originally planned January 2027 date.

What has been the financial impact so far?

Q1 2026 total mineral sales reached $983.85 million, up 79% in value year-on-year. Lithium sales specifically surged 106% in value to $178.64 million on a volume increase of just 2%, reflecting the margin-capture effect of processing mandates.

What is spodumene and why does it matter?

Spodumene is a lithium-bearing pyroxene mineral found in granitic pegmatites. It is the primary hard-rock source of battery-grade lithium chemicals, processed into lithium hydroxide and lithium carbonate for use in lithium-ion battery cathodes.

Will the ban affect global lithium prices?

Near-term spot market tightening is expected, particularly for spodumene concentrate. Medium-term price impact depends on the pace of Zimbabwe's domestic processing ramp-up and the speed at which buyers develop alternative sourcing arrangements.

Key Takeaways

Zimbabwe's lithium export ban represents a deliberate and data-supported industrial policy intervention, not a reactive trade restriction. The Q1 2026 results confirm that the volume-to-value transformation is already underway:

- A 79% revenue increase on 27% volume growth validates the beneficiation logic in the near term

- Zimbabwe's 15% share of China's spodumene imports gives the policy genuine leverage over a strategically critical supply chain

- The long-term outcome hinges on closing the gap between policy intent and processing infrastructure capacity

- Synthetic substitution risk in battery chemistry, while speculative, should inform the timeline urgency of Zimbabwe's processing investment push

- Western supply chain frameworks create both opportunity and complexity for Zimbabwe's integration into non-China battery material corridors

Zimbabwe's export ban is ultimately a calculated wager that the energy transition's structural demand for battery materials will compel downstream processors to follow the ore to its source rather than waiting for ore to flow freely to established processing hubs elsewhere. Whether that wager succeeds depends less on policy design than on the speed and scale of the processing infrastructure that must follow it.

This article incorporates data from the Minerals Marketing Corporation of Zimbabwe as reported by Business Insider Africa (Solomon Ekanem, 17 May 2026) and market assessments from Fastmarkets. Forward-looking statements, projections, and scenario analysis are provided for informational purposes only and do not constitute financial or investment advice. Readers should conduct independent due diligence before making any investment decisions related to companies or assets discussed in this article.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Zimbabwe's lithium export ban illustrates just how rapidly supply chain dynamics can shift the investment landscape — and how quickly informed investors must act when significant discoveries are announced. Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across lithium, PGMs, and more than 30 other commodities, so subscribers can position themselves ahead of the broader market — explore how historic discoveries have generated extraordinary returns and begin a 14-day free trial today.