July 8, 2026

The Battery Minerals Arms Race Is Reshaping How Nations Think About Rock

For most of modern industrial history, lithium was an obscure soft metal used in ceramics, lubricants, and mood-stabilising pharmaceuticals. Few outside specialist geology circles paid it serious attention. That calculus changed dramatically as the world pivoted toward electrification, and it changed again when policymakers in Washington concluded that dependency on a single nation for the processing of a defence-critical input was no longer a tolerable strategic condition. The US-China minerals competition is not primarily a trade dispute. It is a structural contest over which nations control the physical inputs that power both military systems and civilian energy infrastructure in the twenty-first century.

Against that backdrop, Zimbabwe lithium exports to the US have emerged as a topic of serious strategic interest, even if the path from geopolitical aspiration to actual cargo ships is considerably more complicated than most reporting acknowledges.

When big ASX news breaks, our subscribers know first

The $300 Million Signal: What the DLA Contract Actually Communicates

The US Defense Logistics Agency issued a procurement solicitation in July 2026 seeking fixed-price supplier bids for battery-grade lithium carbonate. The contract parameters are substantial:

- Minimum spend: $1 million

- Maximum ceiling: $300 million

- Target volume: approximately 36 million pounds (roughly 16,000 metric tonnes) of battery-grade lithium carbonate

- Delivery window: five years

- Bid deadline: July 17, 2026

The DLA's choice of a fixed-price bid structure is itself analytically significant. Commercial buyers typically negotiate on price, seeking the lowest cost per tonne. A fixed-price procurement framework prioritises supply certainty over cost optimisation, a hallmark of strategic stockpiling logic rather than routine commodity purchasing.

The contract's existence is less important as a single purchasing event and more important as a demand signal confirming that Washington intends to institutionalise its appetite for non-Chinese battery-grade lithium across a multi-year horizon.

China currently controls an estimated 60 to 70 percent of global lithium refining and processing capacity. Even where lithium is mined elsewhere, a significant proportion of global concentrate has historically been shipped to Chinese facilities for conversion into battery-grade carbonate or hydroxide. The DLA contract is a direct attempt to fund an alternative. Consequently, shifts in the global lithium market are now being shaped as much by defence strategy as by commercial demand.

Zimbabwe's Lithium Sector: Production Reality vs. Export Complexity

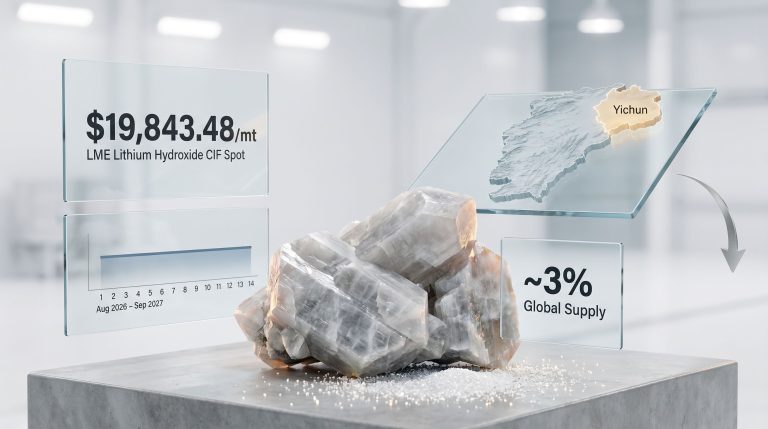

Zimbabwe is Africa's largest lithium producer, and its output trajectory is genuinely impressive. The country exported 586,197 metric tonnes of spodumene concentrate in the first half of 2025, representing a 30 percent increase from the 451,824 metric tonnes shipped in the equivalent period of 2024. Projections suggest Zimbabwe could reach approximately 160,000 tonnes of lithium carbonate equivalent (LCE) in annual production capacity by 2030.

| Metric | Data Point |

|---|---|

| H1 2025 lithium concentrate exports | 586,197 metric tonnes |

| H1 2024 lithium concentrate exports | 451,824 metric tonnes |

| Year-on-year export growth | ~30% |

| Projected annual production by 2030 | ~160,000 tonnes LCE |

| Primary export destination (pre-ban) | China (~85% of shipments) |

However, framing Zimbabwe as a near-term supplier for US defence procurement requires confronting several structural realities that the headline production figures obscure.

The Export Ban That Changes Everything

On February 25, 2026, Zimbabwe implemented an indefinite ban on lithium exports, covering all raw lithium ore, spodumene concentrate, and unrefined mineral products. Enforcement was immediate, including halting shipments already in transit. The policy rationale is straightforward: rather than exporting raw rock for Chinese facilities to convert into value-added products, Zimbabwe's government wants mining operators to build processing infrastructure domestically before any exports resume.

A case-by-case exception mechanism exists for companies holding valid mining titles, but publicly reported applications have been minimal. The practical effect is that Zimbabwe currently exports zero lithium in any form to any buyer, including China.

This distinction matters enormously. Much of the coverage around Zimbabwe lithium exports to the US treats the country as a ready-to-activate supply source. It is not, at least not yet.

The Sanctions Layer Most Analysis Skips

Compounding the export ban is a separate regulatory barrier that receives insufficient attention: the United States and European Union maintain active sanctions regimes targeting Zimbabwe. Any formal supply arrangement between Zimbabwean mining operators and US government agencies would require navigating both the domestic export policy framework and the international sanctions architecture simultaneously.

This dual constraint structurally distinguishes Zimbabwe from the US procurement system's most accessible suppliers, including Australia, Canada, and Chile. Furthermore, given the rising critical minerals demand globally, these distinctions are becoming increasingly consequential for policymakers.

Understanding Battery-Grade Lithium: Why Processing Is the Whole Game

A crucial piece of technical context is often missing from mainstream discussion of the lithium trade: not all lithium outputs are interchangeable.

What battery-grade actually means: Battery-grade lithium carbonate must achieve a minimum purity of 99.5% Li₂CO₃ to meet electric vehicle and defence application specifications. Spodumene concentrate, which constitutes the bulk of Zimbabwe's current exports, typically grades at around 5 to 6 percent Li₂O and requires substantial chemical processing before it approaches battery-grade purity thresholds. Lithium sulphate, while a more advanced intermediate, requires further refining before qualifying as battery-grade carbonate or hydroxide.

Zimbabwe recently shipped its first-ever consignment of locally processed lithium sulphate from the Arcadia lithium project near Harare, marking Africa's first such export milestone. This is symbolically significant and strategically directional, but it represents an early processing step rather than a completed journey to battery-grade output.

The DLA contract specifies battery-grade lithium carbonate. Zimbabwe is not yet producing that at industrial scale. Innovations such as direct lithium extraction technology may eventually accelerate processing timelines, but widespread commercial deployment remains in progress.

Three Scenarios for Zimbabwe Reaching the US Market

Rather than treating US-Zimbabwe lithium trade as either imminent or impossible, a scenario-based framework offers more analytical precision.

Scenario 1: The Processed Minerals Route

This is the most structurally coherent pathway but also carries the longest timeline. If Zimbabwe successfully scales domestic processing from lithium sulphate intermediates to battery-grade carbonate using Western-compatible technology, it could theoretically supply material meeting DLA procurement specifications. The Arcadia milestone demonstrates the directional intent exists.

Key obstacles include:

- Industrial-scale lithium processing plants require years of capital investment and commissioning

- Zimbabwe faces significant constraints in reliable power infrastructure, a prerequisite for energy-intensive chemical processing

- Technical expertise for battery-grade production at scale requires either Western technology partnerships or years of domestic capability building

- A realistic supply window sits at post-2028 at the very earliest, contingent on simultaneous resolution of infrastructure, sanctions, and trade framework challenges

Scenario 2: The Sanctions Carve-Out Pathway

A targeted sanctions waiver or bilateral minerals agreement between Washington and Harare could unlock a formal supply relationship. Precedent exists: the US has negotiated critical minerals agreements with the Democratic Republic of Congo and Zambia as part of broader supply chain diversification. However, Zimbabwe presents additional political complexity.

President Mnangagwa's recent legislative extension of his tenure through 2030 adds a dimension of governance uncertainty that Western policymakers will factor into any diplomatic engagement. Furthermore, Chinese capital is deeply embedded in Zimbabwe's upstream mining sector, meaning that even a diplomatically normalised relationship would not automatically translate into Western-aligned supply chains.

Scenario 3: The Chinese Processing Intermediary Problem

Prior to the February 2026 export ban, approximately 85 percent of Zimbabwe's lithium concentrate was shipped directly to China for processing. This created a situation where Zimbabwean rock ultimately re-entered global supply chains as Chinese-processed material, ineligible for US defence procurement under supply chain origin requirements.

This scenario illustrates why Zimbabwe's domestic processing ambition is not merely an economic development goal but a geopolitical prerequisite for any meaningful Western supply relationship. Chinese-backed processing plants, if they are the first to be built at scale within Zimbabwe, could inadvertently replicate the same supply chain origin problem that the export ban was partly designed to address.

Comparative Supply Chain Readiness: Where Zimbabwe Actually Sits

| Supplier Country | Processing Capacity | US Trade Alignment | Export Readiness | Sanctions Risk |

|---|---|---|---|---|

| Australia | High | Strong (FTA partner) | Immediate | None |

| Chile | Moderate-High | Moderate | Near-term | None |

| Canada | Developing | Strong (CUSMA partner) | Medium-term | None |

| Argentina | Moderate | Moderate | Near-term | Low |

| Zimbabwe | Early-stage | Low (sanctions active) | Long-term | High |

In the near term, the DLA contract's fixed-price structure is likely to favour suppliers with established, Western-aligned processing infrastructure. Australian operators such as Albemarle and Pilbara Minerals, along with Chilean producers, are best positioned to submit competitive bids for the initial contract period. Australia's critical minerals sector, in particular, benefits from strong trade alignment and immediate export readiness.

Chile's lithium strategy, meanwhile, positions it as another well-placed near-term competitor, given its established processing infrastructure and moderate trade alignment with Washington. Zimbabwe's long-term production scale, however, at a projected 160,000 tonnes LCE annually by 2030, combined with the geographic diversification value it offers as a non-Australian, non-South American source, gives it a structural argument for inclusion in future US procurement architecture that is too significant to dismiss.

The next major ASX story will hit our subscribers first

China's Embedded Position: The Conflict of Interest Inside Zimbabwe's Mining Sector

Chinese investment in Zimbabwe's lithium mining sector runs into the billions of dollars. Beijing's strategic approach has been consistent globally: secure upstream mineral supply while simultaneously controlling downstream processing, creating a vertically integrated critical minerals position that is difficult for competitors to displace.

Within Zimbabwe, this creates a structural tension that has no easy resolution. Chinese-backed or Chinese-financed processing plants built within Zimbabwe in response to the export ban could produce battery-grade material that is technically Zimbabwean in origin but economically and logistically tied to Chinese supply chains. Under US defence procurement rules focused on supply chain traceability, such material would likely face eligibility questions.

The export ban was intended to force value addition within Zimbabwe. Whether that value addition serves Zimbabwe's economic interests, China's supply chain interests, or Western buyers' diversification interests depends almost entirely on which investors build the processing plants, on what terms, and with what technology.

What the DLA Contract Tells Long-Term Investors and Policymakers

The $300 million lithium procurement contract carries implications that extend well beyond its five-year delivery window.

- For investors in Zimbabwe's lithium sector: The contract validates sustained Western demand for non-Chinese battery-grade lithium but underscores that processing capability, not raw output, determines market access

- For Zimbabwe's policymakers: The export ban's success depends on attracting Western technology partnerships, not just any capital, to build processing infrastructure aligned with international procurement standards

- For US supply chain strategists: The DLA contract is a medium-term buffer, not a long-term solution. Diversifying away from Chinese-processed lithium at scale requires building allied-nation processing capacity over a decade-plus timeline

- For the broader critical minerals sector: The contract's existence confirms that government-to-government minerals frameworks, rather than purely commercial supply agreements, will increasingly define how lithium moves around the world

This article contains forward-looking analysis based on publicly available procurement data, production projections, and geopolitical assessments. It does not constitute financial advice. Projections regarding Zimbabwe's lithium production, US procurement timelines, and sanctions resolution are subject to material uncertainty and should not be relied upon as predictions of specific outcomes.

Key Structural Barriers to US-Zimbabwe Lithium Trade

| Barrier | Nature | Estimated Resolution Timeline |

|---|---|---|

| Export ban on raw concentrates | Domestic policy | Ongoing by design |

| Absence of battery-grade processing capacity | Infrastructure gap | 3 to 5+ years |

| US and EU sanctions | Bilateral regulatory | Uncertain, requires diplomacy |

| Chinese investment entanglement | Structural/geopolitical | Long-term |

| Bilateral trade framework | Diplomatic prerequisite | Requires sanctions resolution first |

The structural case for Zimbabwe lithium exports to the US is real and grounded in genuine resource scale. The operational case, however — given current export policy, sanctions architecture, processing infrastructure gaps, and Chinese capital entrenchment — remains a multi-year project rather than a near-term reality. Washington's $300 million commitment has done something important regardless: it has placed an unmistakable demand signal in the market, one that Zimbabwe's investors, policymakers, and mining operators would be strategically unwise to ignore.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across lithium, battery metals, and more than 30 other commodities — translating complex geological data into clear, actionable insights for investors at every level. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.