June 19, 2026

The Infrastructure Gap Standing Between Zimbabwe and Lithium Wealth

Across the global battery metals landscape, a quiet but consequential shift is underway. Resource-rich nations are no longer content to serve as raw material exporters while offshore refiners and manufacturers capture the bulk of the economic value. From central Africa to southern Africa, governments are rewriting the rules of mineral extraction, demanding that processing, refining, and value-addition occur within their own borders. Zimbabwe sits at the sharpest edge of this transition, and the pressure is mounting.

Zimbabwe is Africa's largest lithium producer, yet for years its mineral wealth has departed the country in its least refined form, as spodumene concentrate loaded onto trucks and ships bound for Chinese processing facilities. The country's government has moved decisively to change this arrangement, setting an ambitious policy timeline that is now colliding with the physical realities of industrial construction. Zimbabwe lithium miners ask for more time to build processing plants has become the defining story of this collision.

When big ASX news breaks, our subscribers know first

Zimbabwe's Lithium Export Economy: The Numbers Behind the Policy Pressure

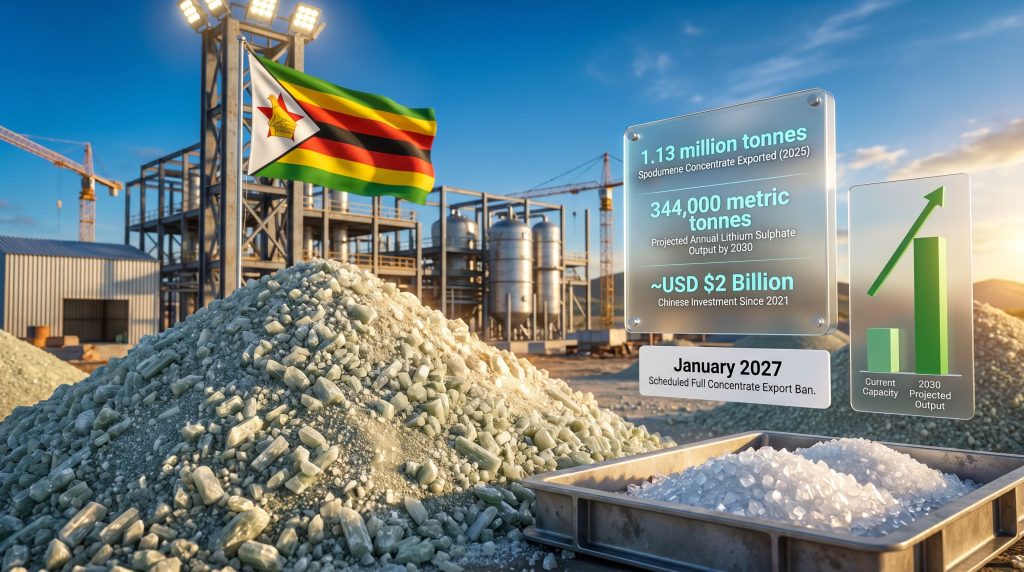

The scale of Zimbabwe's role in global lithium supply flows makes this domestic debate far more than a local regulatory story. In 2025, the country exported 1.13 million tonnes of lithium-bearing spodumene concentrate, with the vast majority destined for China. That volume represented approximately 15% of China's total lithium concentrate imports for the year, making Zimbabwe a meaningful node in the global EV battery supply chain.

Chinese firms have deployed approximately USD $2 billion into Zimbabwe's lithium sector since 2021, consolidating ownership across several of the country's most significant operations. This capital concentration reflects both Zimbabwe's geological endowment and China's strategic interest in locking up upstream battery metal supply. Furthermore, understanding the lithium mining process helps contextualise just how capital-intensive this upstream investment truly is.

| Metric | Data Point |

|---|---|

| Lithium spodumene concentrate exported (2025) | 1.13 million tonnes |

| Share of China's lithium concentrate imports | ~15% |

| Chinese investment since 2021 | ~USD $2 billion |

| Projected annual lithium sulphate output by 2030 | 344,000 metric tonnes |

Despite this activity, virtually all of the refining and chemical conversion value has been captured outside Zimbabwe's borders. The government's beneficiation mandate is a direct response to this structural imbalance.

How Zimbabwe's Beneficiation Policy Works in Practice

Understanding the Processing Mandate

Spodumene extraction, the form in which Zimbabwe has historically exported lithium, is the raw upstream product of hard-rock lithium mining. Converting it into battery-grade lithium sulphate or lithium carbonate requires chemical processing infrastructure that generates substantially higher revenue per tonne and creates domestic industrial employment.

Zimbabwe's policy framework has applied escalating pressure to achieve this shift through a sequence of regulatory interventions:

- A temporary ban on raw lithium concentrate shipments was imposed in February 2026, citing concerns about mineral leakages from the sector.

- Export quotas on lithium concentrate were subsequently introduced alongside a 16% tax on concentrate exports, functioning as a financial penalty on unprocessed shipments.

- A proposed additional 5% levy on lithium concentrates has been flagged by the industry as a further constraint on already compressed operating margins.

- A full ban on lithium concentrate exports is scheduled to take effect in January 2027, representing the hard deadline that miners are now formally requesting to extend.

- The industry body has submitted a formal appeal seeking a deadline extension to approximately June 2027, allowing plants currently under construction to reach commissioning stage.

The 16% export tax functions as an intermediate enforcement mechanism, designed to make raw concentrate exports economically punishing even before the outright ban arrives. The policy logic is sound in theory, but it simultaneously drains the operating cash flows that miners would otherwise direct toward processing plant construction.

Where Zimbabwe's Processing Plants Actually Stand

Project Status Across the Pipeline

The Zimbabwe Lithium Producers' Association has confirmed that major producers across the country are at varying stages of processing infrastructure development. The picture that emerges is one of a sector in genuine transition, but one where the finish line remains out of reach for most participants before the current deadline.

| Operation | Operator | Processing Status | Current Stage |

|---|---|---|---|

| Zhejiang Huayou Cobalt facility | Zhejiang Huayou Cobalt (China) | Fully operational | Exporting lithium sulphate |

| Bikita Minerals | Sinomine (China) | Under construction | Active build phase |

| Kamativi Mine | Sichuan Yahua (China) | Under construction | Active build phase |

| Sandawana Mine | State-owned (Zimbabwe) | Feasibility study | Pre-development |

The Zhejiang Huayou Cobalt facility is the only operation that has crossed the finish line, functioning as the sector's benchmark for what full beneficiation looks like in practice. Bikita Minerals, one of Zimbabwe's most historically significant lithium operations with decades of mining history, is actively building its lithium sulphate plant under Sinomine's ownership. Sichuan Yahua's Kamativi operation is similarly in the construction phase.

Perhaps the most telling entry in this table is Sandawana Mine, the state-owned operation, which remains at feasibility study stage. This means the government itself controls an asset that is furthest from compliance with its own policy mandate.

The Hidden Infrastructure Constraints Slowing Zimbabwe's Transition

Why Capital Alone Cannot Solve the Problem

Processing lithium spodumene concentrate into battery-grade lithium sulphate is a chemically intensive industrial process. It is not simply a matter of constructing buildings and importing equipment. Several enabling infrastructure requirements must be in place before any plant can operate reliably, and Zimbabwe currently faces structural gaps across multiple dimensions.

Power supply is the most fundamental constraint. Chemical and electrolytic processing operations require consistent, high-voltage electricity. Zimbabwe's national grid has experienced significant reliability challenges, and remote mine locations compound this problem further.

Sulphuric acid availability is a critical and often underappreciated bottleneck. Lithium sulphate production consumes large volumes of sulphuric acid, which must be either imported or produced domestically at industrial scale. Neither pathway is straightforward given current logistics and chemical manufacturing capacity in Zimbabwe.

Industrial gas supply represents an additional constraint, with processing operations requiring gases that are not yet widely available in the regions where Zimbabwe's lithium deposits are concentrated.

Water access and logistics infrastructure in remote mining areas create further complexity for establishing the supply chains that processing operations depend on.

Even with sufficient capital committed, the physical build-out of processing infrastructure is governed by supply chain lead times, engineering procurement cycles, and utility commissioning schedules. These are not variables that money alone can compress beyond certain physical limits.

The Financial Squeeze: Why Lithium Prices Make This Harder

Depressed Prices, Rising Costs, and a Financing Paradox

Global lithium prices experienced a severe correction following the extraordinary peaks reached in 2022 and 2023. The collapse in spot prices for lithium carbonate and spodumene concentrate compressed margins across the entire supply chain, from miners to converters to battery manufacturers. Consequently, the lithium carbonate market has become an increasingly complex environment for producers attempting to fund large capital projects simultaneously.

For Zimbabwe's lithium producers, this price cycle has arrived at the worst possible moment. Miners are simultaneously facing:

- Compressed revenue from depressed lithium commodity prices.

- The 16% export tax reducing cash flows from concentrate sales.

- Capital expenditure requirements for large-scale processing plant construction.

- A proposed additional 5% levy that the industry argues must be deferred until refineries reach commercial operation.

The industry's position is that the taxes designed to penalise raw exports are directly undermining the financial capacity to build the processing facilities that would eliminate the need for those exports. This circular constraint creates what can be described as a beneficiation financing paradox that requires a policy response if the 2030 output targets are to remain achievable.

Zimbabwe's 2030 Production Ambition in Context

The Zimbabwe Lithium Producers' Association has projected 344,000 metric tonnes of annual lithium sulphate output by 2030. Achieving that target requires not just completing the plants currently under construction, but commissioning them with sufficient lead time to ramp up to full production capacity. In addition, the broader lithium market downturn has made financing timelines even more unpredictable for operators across the region.

| Policy Scenario | Likely Outcome |

|---|---|

| Extension granted to June 2027 | Construction pipeline completes; 2030 targets remain achievable |

| January 2027 deadline enforced strictly | Partial compliance; operational disruption risk; investor uncertainty |

| No extension and strict enforcement | Potential mine curtailments; possible investment redirection by Chinese firms |

| Extension plus targeted infrastructure investment | Optimal outcome; full beneficiation pipeline operational by 2028 to 2029 |

The next major ASX story will hit our subscribers first

Geopolitical Dimensions: Chinese Dominance and Western Exposure

Who Controls Zimbabwe's Battery Metal Future

The approximately USD $2 billion in Chinese investment since 2021 has created a situation where the beneficiation transition in Zimbabwe is not purely a bilateral story between Harare and its mining sector. The operational timelines of Sinomine, Sichuan Yahua, and Zhejiang Huayou Cobalt are integral to whether Zimbabwe meets its policy targets, meaning Chinese corporate strategy and Chinese financing conditions are embedded in the outcome.

From a supply chain diversification perspective, the critical insight is that even a fully successful beneficiation transition would not fundamentally alter the downstream concentration of Zimbabwe's lithium within Chinese battery manufacturing ecosystems. The product would shift from spodumene concentrate to lithium sulphate, but the customer would remain largely the same.

Western battery supply chain strategies, particularly from the European Union and the United States, currently have limited direct exposure to Zimbabwean lithium at either the concentrate or the chemical product stage. This represents both an underappreciated supply chain vulnerability for Western EV manufacturing ambitions and a potential opportunity for development finance engagement.

How Zimbabwe's Approach Compares Across Africa

Regional Benchmarking on Beneficiation Policy

Zimbabwe is not operating in isolation. Across Africa, resource nationalism and beneficiation mandates have become defining features of the critical minerals policy landscape. However, as Global Witness has reported, a rush for lithium across the continent also risks fuelling corruption and failing citizens if governance frameworks do not keep pace with extraction ambitions:

- The DRC has applied export restrictions to cobalt and copper, encountering familiar infrastructure challenges in translating policy into processing reality.

- Namibia is pursuing an integrated model that combines processing mandates with direct government infrastructure investment, particularly in the green hydrogen and critical minerals space.

- Tanzania has navigated resistance from international mining companies through negotiated compromise frameworks rather than rigid enforcement.

What distinguishes the most successful African beneficiation programmes is the combination of mandatory processing requirements with direct state investment in enabling infrastructure, particularly power and chemical supply chains. Zimbabwe's current framework relies heavily on the private sector to deliver both the processing plants and the supporting infrastructure, without equivalent government investment in the grid reliability and acid supply systems that those plants depend on.

What a Pragmatic Path Forward Looks Like

Conditions for a Successful Transition

A conditional deadline extension, tied to verifiable construction milestones rather than a blanket deferral, would allow the government to maintain policy credibility while acknowledging physical realities. Furthermore, direct lithium extraction technologies may offer complementary pathways for value-addition as Zimbabwe's processing infrastructure matures. Several additional measures would strengthen the transition framework:

- Phased tax relief for miners actively building processing capacity, with relief tapering as plants approach commissioning.

- Direct government investment in power infrastructure and sulphuric acid supply chains serving Zimbabwe's key lithium mining regions.

- Transparent progress reporting from the industry to build regulatory confidence in the extension request.

- Joint infrastructure models that allow multiple operations to share the cost of enabling utilities rather than each project bearing the full burden independently.

- Multilateral development finance engagement to access concessional capital for processing infrastructure in a low-lithium-price environment.

The 2030 target of 344,000 tonnes of annual lithium sulphate output is not unrealistic, but it is contingent on policy flexibility meeting infrastructure investment in a way that Zimbabwe's current framework has not yet fully delivered.

Frequently Asked Questions

Why are Zimbabwe lithium miners asking for more time to build processing plants?

Most processing plants are still under construction and will not reach operational status before the January 2027 concentrate export ban takes effect. Compounding this is a difficult pricing environment for lithium globally, which has reduced cash flows and made it harder to fund and accelerate construction simultaneously.

How many lithium processing plants are currently operational in Zimbabwe?

As of mid-2026, only one facility, operated by Zhejiang Huayou Cobalt, has completed construction and is actively exporting lithium sulphate. Two additional plants are in active construction, and the state-owned Sandawana operation remains at feasibility study stage.

What infrastructure gaps are creating the biggest delays?

Reliable power supply, sulphuric acid availability at industrial scale, industrial gas supply, and logistics access to remote mine locations represent the primary structural constraints limiting how quickly processing infrastructure can be brought online.

What is Zimbabwe's lithium production target for 2030?

The Zimbabwe Lithium Producers' Association projects annual lithium sulphate output of 344,000 metric tonnes by 2030, assuming the current processing plant construction pipeline is completed and commissioned within a workable timeframe.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts and projections referenced reflect industry association estimates and are subject to material change based on commodity prices, regulatory developments, and construction timelines. Readers should conduct independent research before making any investment decisions related to lithium markets or mining equities.

Want to Capitalise on the Next Major Battery Metals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including the battery metals driving the global EV transition — so subscribers can act on actionable opportunities ahead of the broader market. Explore historic discoveries and their returns to understand the scale of what early positioning can mean, then begin your 14-day free trial at Discovery Alert to secure your market-leading edge.