July 13, 2026

The Structural Forces Driving Europe's Position as the World's Leading Aluminium Scrap Exporter

Recycled aluminium is quietly becoming one of the most strategically significant materials in the global industrial economy. Producing secondary aluminium consumes roughly 95% less energy than smelting primary metal from bauxite, making scrap a resource of exceptional economic and environmental value. Yet despite growing political pressure to retain this material within European borders, the data tells a clear story: Europe continues to drive Europe aluminium scrap exports at accelerating volumes, and the forces underpinning that trend run far deeper than policy debate alone.

Understanding why Europe aluminium scrap exports persist at record levels requires looking beyond individual transactions and examining the structural mechanics of how the continent's scrap economy actually functions.

When big ASX news breaks, our subscribers know first

How Europe Became the World's Dominant Aluminium Scrap Supplier

Europe's role as the leading global exporter of aluminium scrap is not accidental. It reflects decades of industrial development across automotive manufacturing, aerospace, construction, and consumer packaging sectors, all of which generate substantial end-of-life aluminium volumes. The EU-27's mature collection infrastructure enables consistent, large-scale scrap recovery that few other regions can match.

The critical dynamic, however, is the gap between scrap generation and domestic processing capacity. Even with some of the world's most sophisticated secondary aluminium industries operating across Germany and Italy, the total volume of scrap collected across the continent routinely exceeds what can be absorbed by European remelters. This structural imbalance is the foundational reason why export surpluses persist.

Critically, this is not simply a matter of market preference. Lower-grade and mixed-composition post-consumer scrap streams often lack viable domestic remelting pathways, particularly when European energy costs make processing economically marginal. The result is a consistent outward flow of material toward overseas secondary smelters in Asia and the Middle East, where lower operational costs make mixed-grade scrap commercially viable.

Q1 2026 Trade Data: A Quarter of Accelerating Outflows

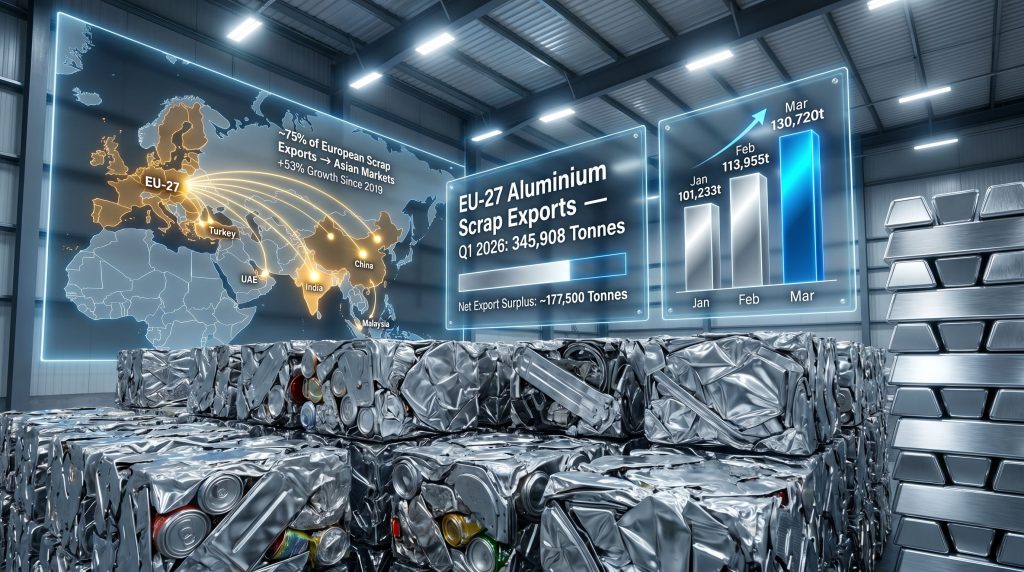

Eurostat data compiled under the HS/CN 7602 classification reveals the scale of Europe's export dominance during the first quarter of 2026. The numbers show not just a surplus, but a widening one.

| Month | Exports (tonnes) | Imports (tonnes) | Net Position (tonnes) |

|---|---|---|---|

| January 2026 | 101,233 | 54,817 | +46,416 |

| February 2026 | 113,955 | 54,658 | +59,297 |

| March 2026 | 130,720 | 58,870 | +71,850 |

| Q1 Total | 345,908 | 168,346 | +177,562 |

What stands out beyond the raw surplus figure is the directional asymmetry. Import volumes remained essentially flat across the quarter, hovering around 54,000 to 58,000 tonnes per month, while exports climbed sharply from 101,233 tonnes in January to 130,720 tonnes in March. That sequential monthly acceleration, with each month outperforming the last, reflects genuine demand momentum from overseas buyers rather than a one-off logistical event.

The net export surplus of approximately 177,500 tonnes across just three months illustrates the structural weight of Europe's position in global secondary aluminium supply chains.

Destination Markets: Asia's Commanding Grip on European Scrap Flows

Approximately 75% of Europe's aluminium scrap exports are absorbed by Asian markets, a concentration that creates both commercial dependency and potential geopolitical exposure for European recyclers and traders.

India and Turkey consistently rank as the largest individual receiving nations, leveraging extensive secondary smelting capacity to convert European scrap into finished aluminium for domestic manufacturing. China and Hong Kong recorded estimated import growth of approximately 12% and 15% respectively year-to-date as of early 2026, reflecting rising demand from Chinese secondary producers. India alone registered approximately 8% growth in European scrap receipts, driven by expanding foundry and extrusion capacity.

Other significant destinations include:

- Malaysia and Pakistan, which operate as both end-use consumers and redistribution intermediaries

- The United Arab Emirates, which serves as a logistics gateway for onward flows into South and Southeast Asian markets

- Several Southeast Asian nations building secondary aluminium production bases to serve regional electronics and automotive supply chains

The economic logic underpinning Asian demand is straightforward. Lower labour costs, less stringent environmental compliance burdens relative to EU standards, and rapidly growing domestic aluminium demand create a compelling arbitrage for overseas processors willing to import European scrap at globally competitive prices.

An additional structural demand driver emerged from US trade policy. US aluminium tariffs on aluminium imports created a diversion effect in global trade flows, redirecting Asian secondary producers toward European scrap as a substitute feedstock. These trade diversion effects effectively amplified demand for European material in Asian markets as an indirect consequence of American trade measures.

Europe's Internal Scrap Economy: A Fragmented Value Chain

The European aluminium scrap market operates as a network of differentiated national roles rather than a unified industrial system. Each major member state contributes differently to the overall value chain.

| Country | Primary Role | Key Scrap Grades / Sectors |

|---|---|---|

| Germany | Processing and secondary production hub | Extrusion, cast, wheel, and mixed grade scrap |

| Italy | Secondary aluminium consumption | Foundry and extrusion sector feedstock |

| Netherlands | Trading and logistics gateway | Multi-origin aggregation via Port of Rotterdam |

| Belgium | Collection and redistribution centre | Non-ferrous scrap sorting and re-export |

| France | Industrial scrap generation | Automotive and manufacturing residues |

| Poland | Emerging secondary production | Automotive-linked Central and Eastern European scrap |

| Sweden and Finland | Clean industrial scrap supply | Highly automated recovery systems |

Germany hosts major recycling operators including TSR Recycling, Scholz Recycling, and EMR, all of which handle significant volumes of extrusion scrap, cast scrap, wheel scrap, and mixed grades. The country feeds both domestic remelters and international export channels, functioning simultaneously as a processor and a logistics originator.

Italy's foundry and extrusion sectors make it a net consumer of scrap within Europe, absorbing large quantities as feedstock and making the country both a recycler and an active buyer of material from other EU member states.

The Netherlands and Belgium occupy a fundamentally different position. Rather than transforming scrap, these countries aggregate, sort, and redistribute material. The Port of Rotterdam in particular functions as Europe's primary non-ferrous scrap export gateway, channelling collected material from across the continent toward overseas buyers. This logistics intermediary role is essential but often mischaracterised as passive; in practice, these hubs determine the operational efficiency of European scrap exports.

The Long-Term Export Trajectory: Five Years of Structural Expansion

The Q1 2026 data does not represent an anomaly. It reflects a sustained multi-year acceleration in Europe aluminium scrap exports that has reshaped global secondary aluminium supply dynamics.

| Period | Estimated Export Volume | Primary Driver |

|---|---|---|

| 2019 baseline | ~850,000 metric tonnes | Organic industrial scrap generation |

| 2025 full year | ~1.3 million metric tonnes (record) | Asian demand surge and US tariff diversion |

| 2026 YTD (April) | ~3% above 2025 pace | Continued Asian demand and EU policy delay |

| Growth since 2019 | +53% | Structural shift toward secondary aluminium |

Export volumes have grown by more than half since 2019, reaching a record approximately 1.3 million metric tonnes in 2025. The 2026 trajectory, running approximately 3% above that record pace as of April, suggests the structural drivers are intensifying rather than plateauing.

The next major ASX story will hit our subscribers first

EU Policy Measures: What Is Actually Being Considered and Why It Has Stalled

European policymakers have characterised aluminium scrap as a critical material for the bloc's low-carbon industrial transition. The EU's recycled aluminium sector currently supplies approximately 40% of domestic aluminium demand, and policymakers have identified a theoretical feedstock pool of roughly 5 million tonnes of recyclable aluminium that could potentially be retained within Europe rather than exported.

Several policy instruments are under active consideration:

| Policy Instrument | Description | Industry Reaction |

|---|---|---|

| Export duties | Tariff of approximately 15% on outbound scrap shipments | Opposed by traders and recyclers |

| Export licensing | Mandatory authorisation system for all scrap shipments | Viewed as administratively complex |

| Recycled-content mandates | Minimum recycled aluminium requirements for EU manufacturers | Supported by primary aluminium producers |

| Trade surveillance system | Real-time tracking of scrap flows, launched mid-2025 | Broadly accepted as a preliminary step |

The original policy finalisation target was set for spring 2026, but implementation has been pushed back to September 2026. According to reporting by Reuters, the delay reflects the genuine complexity of the political economy at play. Primary aluminium producers advocate strongly for retention measures, while recyclers and traders argue that export barriers without corresponding investment in domestic processing capacity would distort markets, strand lower-grade scrap, and potentially trigger retaliatory trade responses from key partner nations.

Furthermore, European supply chain security concerns have become increasingly central to the policy debate, with the Critical Raw Materials Act framing scrap retention as a strategic industrial priority. As a result, Q1 2026 trade flows were largely unaffected by the pending measures, with the surveillance system launched in mid-2025 representing the only active instrument in place during the quarter.

The CBAM Gap: A Critical Structural Flaw in Carbon Border Policy

One of the least-discussed but most consequential policy issues surrounding Europe aluminium scrap exports involves the Carbon Border Adjustment Mechanism. Post-consumer aluminium scrap is currently excluded from CBAM's embedded carbon calculations.

This creates a significant asymmetry. Overseas processors can import European scrap, produce secondary aluminium at lower environmental compliance costs outside the EU, and potentially re-export finished aluminium products back into the European market. The carbon pricing logic that CBAM was designed to enforce is effectively circumvented in this pathway.

European producers increasingly cite closing this CBAM gap as a prerequisite for any export retention strategy to function as intended. Without accounting for the embedded carbon in exported scrap flows, export duties or licensing requirements alone may prove insufficient to redirect material back into domestic processing chains. The CBAM asymmetry problem therefore sits at the intersection of trade policy, climate regulation, and industrial strategy in ways that remain unresolved heading into the September 2026 implementation window.

Russia's Negligible and Largely Irrelevant Scrap Position

Despite periodic speculation about Russian re-entry into European commodity supply chains, the data is unambiguous. Russia's contribution to European aluminium scrap trade flows is statistically marginal.

| Quarter | Russian Aluminium Scrap Exports (tonnes) |

|---|---|

| Q1 2022 | 2,795 |

| Q1 2023 | 251 |

| Q1 2024 | 1,526 |

| Q1 2025 | 535 |

| Q1 2026 | 1,938 |

While Q1 2026 volumes represent a year-on-year recovery from the depressed Q1 2025 levels, the absolute figure of 1,938 tonnes represents well under 1% of total EU-27 external scrap trade volumes. Russia's presence is insufficient to meaningfully influence European scrap pricing, supply availability, or the design of trade policy instruments. The European scrap market's structural dynamics are defined entirely by the EU-27 recycling network and the global demand forces acting upon it.

External Variables: Freight Costs, Energy Prices, and Trade Diversion

Beyond the structural supply-demand dynamics, several external variables shaped Q1 2026 scrap trade patterns. Shipping disruptions across Middle East trade corridors elevated freight costs during the quarter. However, Asian buyers with strong secondary aluminium demand demonstrated willingness to absorb elevated shipping costs, sustaining trade flows at elevated volumes despite higher logistics costs.

European energy prices remained elevated throughout the period, which simultaneously reinforced the economic case for using recycled rather than primary aluminium domestically and made European scrap more price-competitive internationally. Recycled aluminium's approximately 95% energy input advantage over primary smelting becomes more commercially significant as energy costs rise, amplifying the feedstock value of European scrap in global markets. Broader interest in aluminium sector investment has consequently intensified across both primary and secondary production channels.

The Retention vs. Restriction Debate: Why There Are No Easy Answers

The policy debate around Europe aluminium scrap exports ultimately reflects a genuine tension between two legitimate industrial goals. Retaining scrap domestically would reduce EU dependence on imported primary aluminium, support decarbonisation targets, and align with Critical Raw Materials Act objectives around supply chain sovereignty. A closed-loop European aluminium economy would also reduce exposure to commodity price volatility in global markets.

However, the counterarguments from the recycling and trading industry carry real weight. European industry representatives have outlined several key concerns, and furthermore, Europe's critical minerals supply chain remains under considerable strain across multiple material categories:

- Europe currently lacks sufficient processing capacity for all scrap grades it generates, particularly low-value post-consumer mixed streams.

- Restricting exports without first building capacity risks creating domestic scrap price distortions and stranding material that cannot be processed locally.

- Export restrictions could provoke retaliatory measures from key trading partners, complicating EU trade relationships with India, Turkey, and Southeast Asian economies.

- Investment incentives to expand domestic secondary aluminium capacity represent a more economically coherent long-term solution than trade barriers imposed on an inadequate infrastructure base.

In addition, Europe's critical minerals supply chain challenges extend well beyond aluminium alone, meaning that any policy framework must be calibrated carefully to avoid unintended consequences across interconnected material flows. The September 2026 implementation deadline for EU measures will test whether policymakers can navigate these competing interests effectively, or whether the structural reality of Europe's processing capacity gap will once again delay meaningful action.

Disclaimer: This article contains forward-looking statements, forecasts, and policy analysis based on data available as of mid-2026. Trade volumes, policy timelines, and market conditions are subject to change. The information presented is intended for educational and informational purposes and does not constitute financial, investment, or legal advice. Readers are encouraged to consult primary data sources and qualified advisers before making decisions based on the material presented here.

Want to Stay Ahead of Major Mineral Discoveries Shaping Global Commodity Markets?

As structural shifts in aluminium, critical minerals, and broader commodity supply chains continue to reshape investment landscapes, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, translating complex data across 30-plus commodities into clear, actionable insights. Explore historic discoveries and their remarkable returns on Discovery Alert's dedicated discoveries page, or start your 14-day free trial today to position yourself ahead of the market.