May 17, 2026

Global Critical Mineral Dependencies Drive Strategic Resource Development

Modern technological advancement relies heavily on a narrow set of critical minerals that power everything from renewable energy infrastructure to advanced defense systems. The global transition toward electrification, clean energy technologies, and sophisticated manufacturing has created unprecedented demand for rare earth elements, creating both opportunities and vulnerabilities for nations worldwide. This fundamental shift in resource requirements has transformed geological assets into strategic advantages, particularly for countries positioned to develop comprehensive Vietnam rare earth supply chain strategy capabilities.

Understanding the transformation of mineral resources into industrial capacity requires examining the complex interplay between geological endowment, technological capability, regulatory frameworks, and international partnerships. Countries with substantial rare earth reserves face distinct choices about how to monetise these assets whilst navigating geopolitical considerations, environmental responsibilities, and long-term economic development objectives. Furthermore, energy transition security considerations have made mineral resource development increasingly urgent for maintaining industrial competitiveness.

When big ASX news breaks, our subscribers know first

Vietnam's Geological Foundation and Strategic Reserve Position

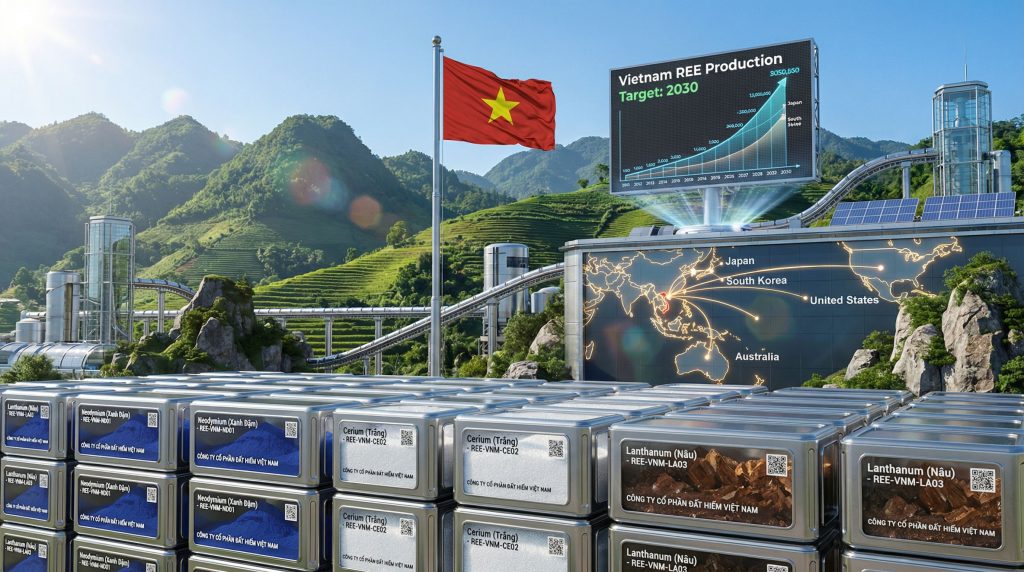

Vietnam's rare earth element endowment represents one of the world's most significant untapped resources, with geological surveys indicating reserves potentially reaching 22 million tonnes. This substantial mineral wealth positions Vietnam among the top global reserve holders, alongside China, Brazil, and India. The concentration of these deposits primarily in northern provinces, particularly Yen Bai and Thai Nguyen regions, creates both opportunities for focused development and challenges for infrastructure coordination.

The geological characteristics of Vietnamese deposits include both light rare earth elements such as lanthanum, cerium, praseodymium, and neodymium, and heavy rare earth elements including dysprosium, terbium, yttrium, and europium. This diverse elemental composition provides strategic flexibility for serving different market segments, from permanent magnet production to specialised electronics applications. Moreover, understanding global rare earth reserves distribution patterns helps contextualise Vietnam's competitive position within international markets.

Current Production Limitations and Market Context

Despite substantial reserves, Vietnam's actual rare earth production remained minimal in 2023, with output estimated at approximately 600 tonnes of rare earth oxides. This figure contrasts sharply with global production patterns, where China produced approximately 644,000 tonnes (70% of global output), Myanmar contributed roughly 5%, and Australia generated around 24,000 tonnes according to USGS data.

The dramatic gap between Vietnam's geological potential and current production illustrates the fundamental challenge of transforming mineral resources into market-relevant industrial capacity. This transformation requires addressing multiple constraints simultaneously: technological capabilities, processing infrastructure, regulatory frameworks, environmental compliance, and market access.

Vietnam's production constraints reflect broader patterns observed across emerging mining economies, where geological advantages do not automatically translate to competitive market positions without substantial intermediate investments in technology, infrastructure, and institutional capacity. Consequently, successful Vietnam rare earth supply chain strategy implementation requires coordinated development across multiple sectors.

Strategic Policy Framework and Downstream Value Capture

Vietnam's approach to rare earth development emphasises state-led coordination and downstream value retention rather than raw material export. This strategy reflects lessons learned from resource-dependent economies that have struggled to capture economic value from commodity exports. The policy framework prioritises domestic processing capabilities and manufacturing integration over maximising short-term mining revenues.

The regulatory approach treats rare earth elements as strategic resources requiring licensing controls, national security screening, and coordination between civilian and defence ministries. This governance structure aims to balance foreign investment attraction with strategic resource control, reflecting policy models implemented in countries like Mongolia with copper and India with rare earth processing. Additionally, critical minerals strategy considerations influence how Vietnam positions itself within global supply chains.

Phased Development Strategy and Timeline

Vietnam's development strategy follows a structured timeline designed to build capabilities sequentially rather than attempting simultaneous advancement across all value chain segments:

Phase 1 (2024-2030): Infrastructure Foundation

- Primary ore concentration facility development

- Basic processing capability establishment

- Workforce training and technology acquisition

- Environmental compliance framework implementation

- Strategic partnership formation with technology providers

Phase 2 (2031-2050): Market Integration and Expansion

- Advanced separation technology deployment

- High-purity product manufacturing capabilities

- Market penetration in key regional and global markets

- Industrial cluster development supporting downstream manufacturing

- Technology indigenisation and innovation capacity building

This extended development horizon acknowledges the complexity of rare earth processing technology and the time required to build sustainable competitive capabilities. The 26-year timeline reflects realistic expectations for developing industrial capacity comparable to established global suppliers.

International Partnership Strategy and Technology Acquisition

Vietnam's technology acquisition strategy focuses on partnerships with Japan, South Korea, Australia, and the United States rather than relying solely on Chinese technology and equipment. This diversification approach aims to build technological capabilities whilst maintaining strategic autonomy and access to non-Chinese supply chains.

Japan represents the most advanced partner in rare earth separation technology and high-performance magnet manufacturing. Japanese companies including Showa Denko and Sumitomo Corporation maintain sophisticated separation capabilities that could accelerate Vietnam's technological development through licensing agreements, joint ventures, or equipment supply arrangements.

South Korea's experience developing integrated rare earth magnet production capabilities provides a model for combining domestic processing with advanced manufacturing applications. South Korean industrial clustering strategies demonstrate how processing capacity can support broader industrial development in electronics and automotive sectors. In addition, Vietnam's rare earth export restrictions create additional complexity for international partnerships.

Trade Agreement Leverage and Market Access

The European Union-Vietnam Free Trade Agreement (EVFTA), which entered force August 1, 2020, and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), effective for Vietnam since January 14, 2019, provide preferential market access that supports non-Chinese supply chain integration.

These agreements eliminate or reduce tariffs on rare earth products, improving the price competitiveness of Vietnamese suppliers relative to Chinese competitors. However, preferential tariff treatment alone does not guarantee market penetration; Vietnamese products must also achieve quality standards, supply reliability, and cost competitiveness alongside tariff advantages.

The trade agreements serve as enabling infrastructure for market access rather than automatic market share guarantees. Success requires Vietnamese suppliers to meet the technical specifications, delivery schedules, and quality standards demanded by international customers in electronics, automotive, renewable energy, and defence sectors. Furthermore, rare earth supply chain dynamics are increasingly influenced by geopolitical considerations.

Critical Technological and Infrastructure Challenges

Vietnam's rare earth ambitions face substantial technological constraints that must be addressed through strategic investments and international partnerships. Current processing limitations prevent the production of high-purity rare earth oxides exceeding 95% purity required by advanced manufacturing applications.

Separation Technology Gaps

Rare earth separation represents the most technically challenging and economically valuable stage of processing. Current Vietnamese facilities lack the advanced solvent extraction and ion-exchange chromatography capabilities required to produce individual rare earth elements at commercial purity levels. Recovery rates at existing operations reportedly fall below 50%, compared to 85-95% achieved by established international facilities.

The technology gap extends beyond processing equipment to include specialised expertise in:

- Multi-stage solvent extraction processes

- Ion-exchange chromatography systems

- Purification and crystallisation techniques

- Quality control and analytical capabilities

- Waste treatment and environmental compliance

Infrastructure Development Requirements

Northern province deposits require substantial logistics infrastructure to support large-scale operations. Current limitations include:

- Transportation Networks: Limited road and rail capacity for moving heavy materials between mining sites and processing facilities

- Power Infrastructure: Insufficient reliable electricity supply for energy-intensive separation processes

- Industrial Clustering: Lack of supporting industries for equipment maintenance, chemical supply, and technical services

- Port Facilities: Limited specialised handling capacity for rare earth product exports

- Workforce Development: Insufficient technical training programmes for specialised rare earth processing skills

These infrastructure constraints require coordinated development across multiple sectors and government levels, creating complex planning and financing challenges for comprehensive capability building. However, modern mine reclamation innovations can help address environmental concerns whilst supporting sustainable development.

Environmental Compliance and Social License Challenges

Rare earth extraction and processing present significant environmental risks that require robust monitoring and mitigation systems. The industry's history of environmental incidents in various countries has created heightened awareness among international partners and investors about operational standards and long-term sustainability.

Environmental Risk Management Framework

Key environmental challenges include:

- Acid Mine Drainage: Preventing contamination of groundwater and surface water systems

- Heavy Metal Contamination: Managing toxic byproducts from processing operations

- Radioactive Material Handling: Safely managing naturally occurring radioactive elements associated with rare earth deposits

- Waste Management: Developing secure storage and treatment systems for processing residues

- Air Quality Protection: Controlling dust and chemical emissions from mining and processing operations

Vietnam's environmental compliance framework must meet international standards to maintain credibility with global partners and avoid operational disruptions. This requirement extends beyond regulatory compliance to include transparent monitoring, community engagement, and continuous improvement in environmental performance.

The next major ASX story will hit our subscribers first

Competitive Analysis and Global Market Positioning

Vietnam's entry into global rare earth markets requires competing with established suppliers whilst building technological capabilities and market relationships simultaneously. The competitive landscape includes both state-controlled Chinese producers and private companies in Australia, the United States, and other jurisdictions.

| Country | Reserve Estimates | 2023 Production | Processing Capability | Key Competitive Advantages |

|---|---|---|---|---|

| Vietnam | 22 million tonnes | 600 tonnes | Limited separation | Large reserves, strategic location, government support |

| China | 44 million tonnes | 644,000 tonnes | Dominant processing | Complete value chain, technological leadership, cost efficiency |

| Australia | 4.1 million tonnes | 24,000 tonnes | Moderate processing | Established operations, stable governance, Western partnerships |

| United States | 1.5 million tonnes | 15,000 tonnes | Advanced separation | Technology leadership, defence applications, domestic market |

| Brazil | 21 million tonnes | 5,000 tonnes | Basic processing | Large reserves, growing industrial base |

Market Differentiation Strategy

Vietnam's competitive positioning emphasises several potential advantages:

- Geographic Proximity: Strategic location for serving Asian electronics and automotive manufacturing hubs

- Cost Structure: Lower labour costs compared to developed country competitors

- Government Support: State commitment to strategic development and infrastructure investment

- Trade Access: Preferential market access through EVFTA and CPTPP agreements

- Partnership Flexibility: Ability to work with multiple technology partners rather than single-source dependence

However, these advantages must be developed and maintained through consistent policy implementation, sustained investment, and technological capability building over extended timeframes. Consequently, effective Vietnam rare earth supply chain strategy development requires long-term commitment.

Financial Projections and Economic Impact Assessment

Vietnam's potential to capture 10% of global rare earth market share could generate approximately $2 billion in annual revenue, based on current market valuations and projected demand growth. This projection assumes successful execution of processing capacity development, quality standard achievement, and market penetration strategies across multiple geographic markets.

The economic impact extends beyond direct revenue to include:

- Employment Creation: Direct employment in mining and processing operations plus indirect employment in supporting industries

- Technology Transfer: Knowledge spillovers to related industries including electronics, metallurgy, and chemical processing

- Industrial Development: Foundation for downstream manufacturing in permanent magnets, catalysts, and specialised alloys

- Export Diversification: Reduced dependence on traditional export sectors whilst building higher-value industrial capacity

Investment Requirements and Capital Intensity

Developing comprehensive rare earth processing capabilities requires substantial capital investment across multiple phases:

- Mining Infrastructure: $200-500 million for large-scale mining operations including equipment, roads, and processing facilities

- Separation Technology: $100-300 million for advanced processing facilities capable of producing high-purity individual elements

- Environmental Systems: $50-150 million for waste treatment, monitoring, and remediation capabilities

- Workforce Development: $20-50 million for training programmes, technical education, and expertise acquisition

These capital requirements necessitate patient investor approaches and government support for long-term industrial development rather than short-term profit maximisation. For investors, understanding investment strategy insights becomes crucial for navigating this complex sector.

Risk Assessment and Mitigation Strategies

Vietnam's rare earth development strategy faces multiple risk categories that could affect implementation success and long-term viability.

Technology Acquisition and Transfer Risks

Dependence on foreign technology partners creates potential vulnerabilities if geopolitical relationships change or partners restrict technology access. Advanced rare earth separation technology remains closely guarded by existing producers, making technology transfer negotiations complex and potentially unstable.

Mitigation strategies include:

- Diversifying technology partnerships across multiple countries and companies

- Investing in domestic research and development capabilities

- Building indigenous technical expertise through education and training

- Developing technology licensing agreements with clear long-term access provisions

Market Competition and Pricing Pressures

China's dominant position in rare earth processing creates ongoing competitive pressure through both cost advantages and potential supply manipulation. Chinese producers can potentially use pricing strategies to discourage market entry by new competitors or limit the economic viability of alternative suppliers.

Vietnam's response requires building sustainable cost advantages through efficient operations, preferential market access, and differentiated product offerings that create customer value beyond price competition. Therefore, Vietnam's rare earth industry development must focus on technological advancement and operational efficiency.

Environmental and Social License Risks

Environmental incidents or social conflicts could disrupt operations, damage international reputation, and limit access to foreign investment and technology partnerships. The global rare earth industry's environmental track record creates heightened scrutiny for new operations.

Risk mitigation emphasises proactive environmental management, transparent community engagement, and continuous monitoring systems that exceed minimum regulatory requirements.

Long-term Strategic Implications and Future Scenarios

Vietnam's rare earth development success would establish the country as a significant alternative supplier in global markets whilst building technological capabilities that support broader industrial development objectives. Achievement of stated goals would reduce global dependence on Chinese supply chains whilst creating economic opportunities for Vietnam's transition toward higher-value manufacturing.

Scenario Analysis: Success Factors

High Success Scenario requires:

- Successful technology transfer and capability development

- Consistent regulatory implementation and environmental compliance

- Sustained government support and investment coordination

- Market acceptance and customer relationship development

- Global demand growth for supply chain diversification

Moderate Success Scenario involves:

- Partial technology acquisition with continued foreign dependence

- Limited market penetration concentrated in regional Asian markets

- Basic processing capabilities without advanced separation technology

- Continued raw material export alongside modest value-added production

Low Success Scenario includes:

- Technology transfer failures or partner withdrawal

- Environmental incidents or regulatory enforcement problems

- Market access limitations due to quality or reliability issues

- Continued dependence on raw material exports with minimal value capture

Investment Implications for Stakeholders

Investors evaluating Vietnam's rare earth potential must consider the extended development timelines, substantial capital requirements, and execution risks against potential returns from successful market entry. The investment opportunity spans equipment suppliers, technology providers, processing companies, and integrated rare earth enterprises with Vietnamese operations or partnerships.

Risk-adjusted return considerations include:

- Timeline Risk: 26-year development horizon requiring patient capital

- Technology Risk: Dependence on foreign partners for critical capabilities

- Market Risk: Competition with established, cost-efficient suppliers

- Political Risk: Regulatory changes or policy reversals affecting operations

- Environmental Risk: Compliance costs and potential operational disruptions

Successful Vietnam rare earth investments likely require deep industry expertise, long-term capital availability, and comprehensive understanding of both technological and political risk factors affecting implementation.

The transformation of Vietnam's geological assets into industrial capabilities represents one of the most ambitious rare earth development projects outside China. Success would reshape global supply chain patterns whilst failure would reinforce existing market concentration and strategic vulnerabilities for consuming nations seeking supply diversification.

Disclaimer: This analysis contains forward-looking projections and assessments based on available information and industry analysis. Actual outcomes may differ significantly from projections due to market conditions, technological developments, regulatory changes, or other factors not fully predictable at the time of publication. Investment decisions should be based on comprehensive due diligence and professional financial advice.

Considering Strategic Investment Opportunities in Critical Minerals?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, instantly identifying actionable opportunities in critical minerals and strategic resources before broader market recognition. Begin your 30-day free trial today to position yourself ahead of evolving global supply chain dynamics and secure your competitive investment advantage.