May 22, 2026

The Industrial Metal Most Exposed to War: Why Gulf Aluminium Output Is in Freefall

Few industrial materials reveal the fragility of globalised supply chains quite like primary aluminium. Unlike oil, which benefits from diverse extraction geographies and deep strategic reserve systems, aluminium smelting is an extraordinarily capital-intensive, energy-hungry, and geographically concentrated process. When a major producing region faces sustained disruption, the market cannot simply pivot overnight. Smelters take months to restart after curtailment.

Feedstock pipelines are long and specialised. And the buyers who depend on regional supply often have limited short-term alternatives.

That structural reality is now playing out in real time across the Gulf Cooperation Council. The ongoing conflict in the Middle East has pushed gulf aluminium output falls as Middle East crisis disrupts smelters to levels not seen in over a decade, triggering a cascade of consequences that extends far beyond the region itself and into the import frameworks of economies as distant as Japan and the United States.

When big ASX news breaks, our subscribers know first

The Gulf's Rise as a Global Aluminium Powerhouse

Over the past two decades, the GCC transformed itself into one of the world's most significant primary aluminium producing regions. The formula was straightforward: abundant and historically cheap energy, sovereign wealth capable of funding billion-dollar smelting infrastructure, and deep-water port access that made export logistics competitive on a global scale.

The UAE, Bahrain, Saudi Arabia, and Qatar each developed smelting capacity during this period, with the UAE and Bahrain emerging as the dominant producers. Emirates Global Aluminium in the UAE grew into one of the largest single-site aluminium producers anywhere on earth. Aluminium Bahrain, known as Alba, expanded through successive potline additions to become a globally significant operation with capacity exceeding 1.5 million tonnes per year.

The numbers that resulted from this development are striking in their scale and in their implications for global trade. Furthermore, understanding who the top aluminium producers are globally helps contextualise the Gulf's outsized role in international supply:

| Metric | Value |

|---|---|

| Gulf share of global primary aluminium output | ~8-9% |

| Gulf share of Japan's aluminium imports | ~28% |

| Gulf share of U.S. aluminium imports | ~21% |

| Global primary aluminium output (April 2026) | 5.92 million tonnes |

| Gulf output (April 2026) | 330,000 tonnes |

| Gulf output decline (April 2026 vs. April 2025) | -35% year-on-year |

| GCC output in Q1 2026 | 1.49 million tonnes (4-year low) |

The Gulf's role in aluminium trade is not peripheral. It is structurally embedded in the procurement architecture of major industrial economies. A sustained contraction in regional output does not simply remove volume from the market; it forces buyers to dismantle and rebuild sourcing strategies that took years to construct.

Why the Middle East Conflict Is Dismantling Gulf Smelter Operations

The Continuous-Process Vulnerability of Aluminium Smelting

Aluminium production is fundamentally different from most industrial manufacturing in one critical respect: it cannot be paused. Electrolytic reduction cells, which convert alumina into molten aluminium through the Hall-Heroult process, must operate continuously. If a cell is allowed to cool, the molten bath solidifies into a form of aluminium fluoride compound that is extremely difficult and expensive to remove.

Restarting a curtailed potline typically requires months of preparation, significant capital expenditure, and a stable energy and feedstock supply that conflict zones rarely provide.

This continuous-process requirement means that geopolitical disruption hits aluminium smelters disproportionately hard. A logistics interruption that might merely delay a steel mill for a few weeks can force an aluminium smelter into months of curtailment, with restart timelines that extend the production loss well beyond the initial disruption event.

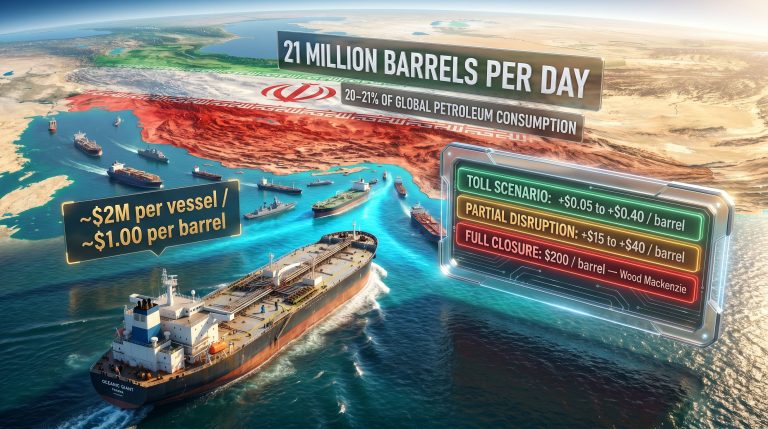

The Strait of Hormuz: A Chokepoint Tightening on Both Ends

The Strait of Hormuz carries an outsized role in the aluminium supply chain that is rarely appreciated outside specialist circles. The waterway serves simultaneously as the export corridor for Gulf primary aluminium and as the inbound route for alumina, the refined feedstock from which aluminium is produced. Every tonne of primary aluminium requires approximately 1.93 tonnes of alumina to produce, meaning that feedstock flows are nearly double the volume of finished metal output.

When conflict-related shipping disruption tightens the Hormuz corridor, it creates a dual squeeze. Finished metal cannot leave the region efficiently, and raw material cannot enter. The downstream consequence of this squeeze became visible in March 2026 data: alumina imports into the Middle East fell 63% year-on-year, a figure that functions as an early warning signal for the smelter output collapse that followed in April.

Producers have responded by attempting to secure overland transport alternatives, but these routes carry significant cost premiums, face capacity constraints, and cannot replicate the volume flexibility of maritime shipping. The logistics pivot is a stopgap, not a solution. For further context on how aluminium supply crisis scenarios are developing around Hormuz, the picture remains deeply uncertain.

Facility-Level Damage and the Curtailment-Versus-Loss Distinction

Reported operational disruptions at major Gulf smelting facilities, including assets operated by Emirates Global Aluminium and Aluminium Bahrain, have compounded the feedstock problem. Assessing damage in an active conflict zone is inherently imprecise, and industrial reporting from such environments carries embedded uncertainty.

The distinction that analysts are focused on is the difference between temporary curtailment and structural capacity loss. A curtailed smelter can theoretically be restarted within a defined timeframe. A smelter that has sustained physical infrastructure damage, particularly to its potlines, busbar systems, or rectifier equipment, may face multi-year recovery timelines. The investment required to rebuild such systems is substantial, and lenders willing to commit capital to conflict-adjacent industrial reconstruction are a limited pool.

Quantifying the Shock: Reading the Production Data

The April 2026 IAI Data in Context

Preliminary data released by the International Aluminium Institute confirmed that Gulf output reached 330,000 tonnes in April 2026, representing a 35% year-on-year decline and the lowest regional production figure in more than a decade. This figure did not arrive without warning. Q1 2026 GCC output had already recorded a 4-year low of 1.49 million tonnes, establishing a deteriorating trend that April accelerated sharply.

The critical analytical point is trajectory. Q1 weakness had already signalled structural stress in Gulf operations. The April data represents a further step down, and analysts warn that April may not represent the floor of the decline cycle given the ongoing nature of the conflict and the feedstock constraints already evident in March alumina import data.

Global Output: The Gulf's Disproportionate Weight

| Region | April 2026 Output | Year-on-Year Change |

|---|---|---|

| Global Total | 5.92 million tonnes | -2.1% |

| China | 3.68 million tonnes | +1.5% |

| Gulf Region | 330,000 tonnes | -35% |

Global primary aluminium output fell 2.1% year-on-year in April 2026, and the Gulf contraction is the primary driver of that decline. China, by contrast, expanded production by 1.5% to 3.68 million tonnes, providing a partial offset to the global volume shortfall.

However, Chinese output cannot functionally substitute for Gulf supply in Japan and the United States. The global metals tariff impacts from successive rounds of trade policy tightening create significant cost barriers to Chinese aluminium entering these markets. Logistical factors compound the challenge, and buyer preference issues — including quality specifications and long-standing commercial relationships — mean that Gulf supply disruption creates a genuine supply gap rather than a simple reallocation problem.

Market Response: Prices, Premiums, and the Surplus-to-Deficit Risk

LME Price Movement and Forward Positioning

LME aluminium prices have risen approximately 13.67% as Gulf supply tightened, approaching 2-year highs. This price movement reflects both current physical tightness and forward uncertainty. Futures markets are increasingly pricing in the possibility that Gulf smelter outages will persist beyond Q2 2026, which would transform a supply disruption into a sustained structural deficit.

It is worth noting that aluminium price discovery on the LME incorporates not only spot supply fundamentals but also financing positions, currency movements, and speculative positioning. The 13.67% rise reflects a market that has moved from treating the Gulf disruption as a temporary event to treating it as an ongoing structural risk. Developments in aluminum and alumina markets globally are further amplifying this uncertainty.

Import Market Exposure: Japan and the United States

The two economies with the sharpest direct exposure to Gulf supply disruption are Japan and the United States. Japan sources approximately 28% of its aluminium imports from the Gulf region, making it the most heavily exposed major importing economy. Japanese buyers, who operate under long-term bilateral supply agreements and quarterly premium pricing mechanisms, are facing acute spot market pressure as Gulf deliveries fall short.

The United States sources approximately 21% of its aluminium imports from the Gulf. US aluminium tariffs have already reshaped procurement strategies, and American downstream manufacturers — including automotive, aerospace, and packaging producers — are absorbing higher input costs as both domestic supply constraints and Gulf import shortfalls converge. European buyers face a more complex picture, with Gulf supply disruption compounding existing uncertainty generated by trade policy changes on both sides of the Atlantic.

Scenario Alert: If Gulf smelter outages persist beyond Q2 2026 and alumina feedstock flows through the Strait of Hormuz remain constrained, the global aluminium market — previously projected in modest surplus — could shift toward deficit conditions. The speed of this transition depends heavily on the duration of operational disruption at major UAE and Bahrain facilities.

Inventory Buffers and the Backstop Question

LME-registered aluminium inventories have historically served as a buffer against short-term supply disruptions. However, inventory levels entering the current crisis were not exceptionally elevated, limiting the capacity of exchange stocks to absorb extended Gulf underperformance. Off-exchange inventory, held in consumer and trader warehouses, adds additional buffer but is more opaque in its availability and accessibility.

Chinese export capacity theoretically provides a further backstop, but the trade barriers described above mean that Chinese material cannot flow freely into deficit markets. The backstop is real but structurally imperfect, and its efficacy diminishes the longer the Gulf disruption persists.

Strategic Dimensions: Aluminium as a War-Economy Resource

Why Aluminium's Strategic Status Is Frequently Underestimated

Aluminium is consumed in quantities that make it the second most widely used metal on earth after steel, yet its strategic significance is consistently underappreciated in public discourse relative to rarer materials like lithium, cobalt, or rare earth elements. The metal's applications in aerospace structures, defence manufacturing, automotive lightweighting, electrical transmission infrastructure, and grid-scale energy storage make it a foundational industrial material in both peacetime and conflict economies.

Analysis published by the Modern War Institute at West Point has examined aluminium's role as what researchers describe as a foundational metal of war, noting the intersection of Gulf conflict geography and American strategic vulnerability given that approximately 21% of U.S. aluminium imports originate from the region. The defence-policy dimension of this supply disruption extends well beyond commodity market dynamics.

The Hormuz Exposure Differs Fundamentally from Oil Disruption

Historical comparisons between Hormuz disruption scenarios for oil and aluminium reveal an important asymmetry. An oil field that is disrupted can often resume production relatively quickly once the disruption is resolved. An aluminium smelter that is forced into curtailment faces a technically complex and financially costly restart process that may extend the production loss by six months to a year beyond the initial disruption event.

This asymmetry means that even a resolution of the underlying conflict does not automatically restore Gulf aluminium output on a short timeline. The damage already done to production continuity, feedstock inventory levels, and potentially to physical smelter infrastructure will require sustained remediation effort regardless of when geopolitical conditions improve.

The next major ASX story will hit our subscribers first

Three Forward Scenarios for Gulf Aluminium Recovery

The range of plausible outcomes for Gulf aluminium production spans from relatively rapid stabilisation to multi-year structural impairment. The scenario framework below captures the key variables and market implications of each pathway.

Scenario 1: Rapid Stabilisation (3-6 Months)

- Conflict de-escalation or ceasefire restores Hormuz shipping lane functionality

- Alumina feedstock flows normalise; smelters resume operations at reduced but recovering capacity

- LME price premium partially unwinds as buyers regain confidence in Gulf supply continuity

- Japan and U.S. spot market premiums ease; long-term supply contracts resume normal delivery schedules

Scenario 2: Prolonged Disruption (6-18 Months)

- Conflict persists; facility damage at EGA and Alba proves more extensive than initial assessments indicate

- Global aluminium market transitions into deficit; LME prices sustain elevated levels and may extend gains

- Japan and U.S. buyers accelerate supply diversification toward Australian, Canadian, and Norwegian producers

- Alumina trade flows restructure, with Australian and South American suppliers increasing shipments to non-Gulf customers

Scenario 3: Structural Capacity Loss (18+ Months)

- Severe infrastructure damage forces multi-year capacity impairment at key Gulf smelting facilities

- Global aluminium market enters sustained deficit; prices reach multi-year highs

- Accelerated investment in non-Gulf primary smelting capacity reshapes the global production landscape

- Supply chain regionalisation accelerates, with North American, Southeast Asian, and African capacity development gaining commercial momentum

Could the Crisis Accelerate Supply Chain Regionalisation?

The gulf aluminium output falls as Middle East crisis disrupts smelters is unfolding against a backdrop of pre-existing pressure to diversify critical material supply chains away from geopolitically concentrated regions. The aluminium industry had already begun responding to this pressure before the current conflict, with investments in Australasian, African, and North American smelting capacity under consideration or development by various producers.

The current disruption materially strengthens the commercial case for this diversification. Buyers who previously accepted Gulf supply concentration as an acceptable risk are now experiencing the consequences of that concentration firsthand. Consequently, the long-term effect may be a global aluminium supply network that is more geographically distributed but also structurally more expensive.

New capacity developed in higher-cost jurisdictions will replace the low-cost Gulf production model built on subsidised energy and sovereign capital. In addition, industrial decarbonisation trends are further complicating investment decisions, as producers weigh cost competitiveness against emerging green production mandates. The tension between supply security and cost competitiveness will define aluminium procurement strategy for the decade ahead, and the events of 2026 will likely be cited as the inflection point that forced that conversation into boardrooms across the aerospace, automotive, and infrastructure sectors.

Furthermore, as end-user sectors worldwide grapple with the present aluminium chaos, the pressure on procurement teams to establish resilient, diversified supply relationships has never been greater.

Key Takeaways: The Gulf Aluminium Crisis at a Glance

- Gulf primary aluminium output fell 35% year-on-year in April 2026 to 330,000 tonnes, a decade-low confirmed by IAI preliminary data

- Q1 2026 GCC output reached a 4-year low of 1.49 million tonnes, with the Q2 deterioration accelerating sharply

- Alumina imports into the Middle East fell 63% year-on-year in March 2026, signalling upstream feedstock collapse ahead of the April production shock

- Global primary aluminium output declined 2.1% year-on-year in April 2026, with the Gulf contraction as the primary driver

- LME aluminium prices have risen approximately 13.67%, approaching 2-year highs as the market prices in structural disruption risk

- Japan and the U.S. face the sharpest import exposure, sourcing 28% and 21% of aluminium imports respectively from the Gulf

- China's 1.5% output growth to 3.68 million tonnes provides partial global offset but cannot replicate Gulf supply flows into key import markets

- The critical forward variables: EGA and Alba facility damage assessment, Hormuz shipping normalisation, and alumina feedstock flow recovery

This article contains forward-looking analysis and scenario projections based on available data as of May 2026. Market conditions, geopolitical developments, and production outcomes may differ materially from the scenarios described. This content is intended for informational purposes only and does not constitute financial or investment advice.

Want to Stay Ahead of the Next Major Commodity Disruption?

Significant supply shocks like the Gulf aluminium crisis create rare windows of opportunity for investors who can act quickly — Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts, turning complex commodity market shifts into actionable investment insights for both short-term traders and long-term investors. Explore historic discoveries and their market returns to understand the scale of opportunity, and begin your 14-day free trial today to secure a market-leading edge before the broader market catches on.