June 12, 2026

When Three Shocks Converge: Understanding the Nickel Market Perfect Storm in Indonesia and the Middle East

Commodity markets rarely move on a single catalyst. The most significant and durable price inflections tend to emerge when multiple independent pressures converge simultaneously, compressing supply while cost floors rise and demand signals remain uncertain. That is precisely the structural environment now surrounding global nickel, where Indonesian policy shifts, environmental enforcement, and Middle East conflict spillovers have collided to create conditions that analysts have described as a perfect storm. The nickel market perfect storm in Indonesia and the Middle East is best understood as a multi-layered structural reconfiguration, not a temporary market disruption.

When big ASX news breaks, our subscribers know first

The Fault Lines That Were Already There

Why Nickel Was Primed for a Reckoning Before 2025

Before any geopolitical catalyst arrived, nickel already carried significant structural vulnerabilities. Years of suppressed prices had created what market analysts describe as a coiled spring effect, where prolonged underpricing deferred capital investment in new supply while existing operations struggled to justify expansion.

The concept of incentive pricing is central here. In mining economics, the incentive price refers to the price level at which developers can justify building a new mine on a risk-adjusted basis. For nickel sulfide projects specifically, which represent the highest-quality Class 1 nickel relevant to battery supply chains, prices through 2023 and 2024 were insufficient to attract meaningful development capital. Without new supply pipelines being activated, the market became increasingly reliant on existing Indonesian laterite production, which carries its own structural fragility.

This combination of deferred sulfide development and concentrated dependence on Indonesian laterite operations meant that when external shocks arrived, there was no buffer capacity to absorb them.

The First Pillar: Indonesia's Policy Tightening

Indonesia Controls Roughly Two-Thirds of Global Nickel Supply

Indonesia's position in global nickel is without parallel. The country controls approximately two-thirds of global nickel output, a concentration that means even incremental domestic policy adjustments carry disproportionate consequences for global pricing and availability. No other single national jurisdiction holds comparable leverage over a major battery material.

The Indonesian government's decision to limit the volume of laterite ore that can be mined and processed domestically has been one of the defining supply-side events of 2025. Rather than relying solely on abundant domestic ore, Indonesian nickel pig iron and High Pressure Acid Leach (HPAL) operations have been forced to source increasing volumes of feedstock from the Philippines. Philippine ore is structurally more expensive to procure and transport, which directly elevates the cost floor for a meaningful share of Indonesian production.

Furthermore, the Indonesian nickel industry's growth has brought with it a set of escalating structural challenges that are now reshaping global supply dynamics.

What HPAL Is and Why Input Costs Matter So Much

HPAL, or High Pressure Acid Leach, is the primary processing pathway for converting laterite nickel ore into battery-grade nickel sulfate. The process is energy-intensive, chemically demanding, and critically dependent on a continuous supply of sulfuric acid. When either energy costs or sulfuric acid availability deteriorates, HPAL operations face simultaneous pressure on both their input cost structure and their operational continuity.

Environmental enforcement has added a third dimension to Indonesia's supply-side constraints. The Indonesian government has increasingly moved to address the significant environmental damage caused by laterite mining and processing operations, with enforcement actions leading to forced curtailments at a number of sites. These are not temporary suspensions pending compliance upgrades; they represent a structural tightening of the operating environment for Indonesia's nickel industry.

| Supply-Side Driver | Mechanism | Market Impact |

|---|---|---|

| Reduced mining quotas | Less domestic ore available for processing | Higher raw material costs for NPI and HPAL |

| Philippine ore substitution | Higher-cost external feedstock | Rising cost floor across Indonesian operations |

| Environmental shutdowns | Forced curtailments of laterite processing | Reduced output volumes, tighter available supply |

| Export regulation uncertainty | Policy risk for downstream buyers | Procurement hesitation and inventory drawdowns |

The Second and Third Pillars: How the Middle East Conflict Reshaped Nickel Economics

The Sulfur Supply Chain Disruption That Few Anticipated

The connection between Middle East conflict and Indonesian nickel production is not immediately obvious, but the supply chain logic is direct. Sulfur, which is refined into sulfuric acid and used in vast quantities by HPAL operations, is a byproduct of oil and gas refining. A significant portion of global sulfur supply transits through or originates near the Strait of Hormuz corridor. Disruption to that logistics pathway reduces sulfuric acid availability, which in turn constrains HPAL output in Indonesia regardless of how much laterite ore is theoretically available.

This is not a modest secondary effect. HPAL is among the most sulfuric acid-intensive processes in industrial mining, and Indonesian HPAL facilities have no easy short-term substitutes for Gulf-sourced sulfur supply. The result has been measurable pressure on nickel and cobalt production from HPAL operations, tightening output at precisely the moment when ore-side constraints were already active. According to BMI's analysis of Indonesian supply dynamics, Middle East conflict is driving significant volatility on top of already constrained supply conditions.

Energy Costs and the Full Cost Curve Transmission

Nickel laterite processing, encompassing both HPAL and nickel pig iron (NPI) production, is among the most energy-intensive operations in the entire mining sector. Coal is the primary energy source for NPI production in Indonesia, and coal prices are closely correlated with oil and gas price movements. When oil prices rise, gas prices follow, coal prices respond, and the entire Indonesian nickel cost curve shifts upward simultaneously.

This energy transmission mechanism means that the Middle East conflict functions as a dual input shock for Indonesian nickel producers: it simultaneously restricts sulfuric acid availability and elevates energy costs. The combination creates what can legitimately be described as a triple whammy of cost pressure, where feedstock, chemical inputs, and energy all deteriorate in the same direction at the same time.

The Barnacle Problem: Why Strait Reopening May Not Restore Supply Quickly

One of the least-discussed but potentially most consequential complications involves the operational status of supertankers that have been stationary in the Persian Gulf for extended periods. When large vessels remain at anchor in warm, still waters of 20 to 30 degrees Celsius for two to three months, marine barnacles accumulate on hulls and, critically, on propellers. Barnacle buildup on hull surfaces can reduce vessel speed by 40 to 60 percent through increased drag.

Accumulation on propellers creates a more severe problem and may render some vessels unable to exit the Gulf under their own power at all. The practical implication is that even a formal reopening of the Strait of Hormuz would not immediately restore sulfur and chemical supply flows to pre-conflict levels. Informed analysis suggests that full supply restoration could take six to nine months or longer, meaning the market should not price in a rapid normalisation simply because a ceasefire occurs.

The duration of the supply disruption may significantly outlast the conflict itself, a dynamic that is not yet fully reflected in mainstream price forecasts.

Is a Nickel Supply Deficit Now Inevitable?

What the INSG's 2026 Deficit Forecast Actually Signals

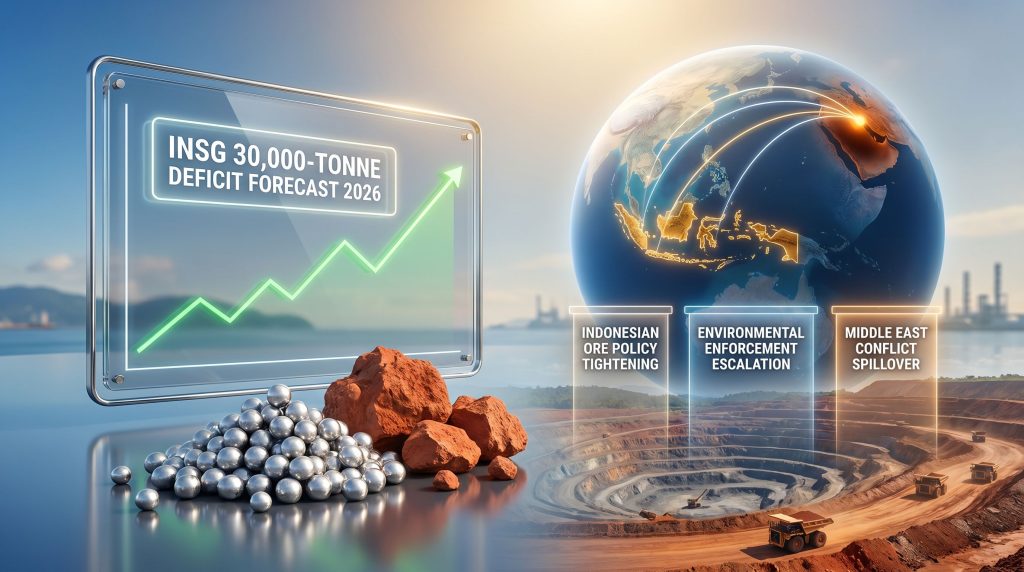

The International Nickel Study Group (INSG) has projected a supply deficit of approximately 30,000 tonnes for 2026, which would represent the first projected supply shortfall in the nickel market in roughly five years. Given that the nickel market has been in persistent surplus since the Indonesian NPI and HPAL expansion wave of the early 2020s, even a modest deficit carries significant psychological and structural weight for pricing.

A 30,000-tonne deficit is not enormous in absolute terms relative to total market size, but its significance lies in the directional shift it represents. Moving from chronic surplus to deficit recalibrates inventory behaviour, procurement strategies, and the risk premium that buyers are willing to pay for supply security. Consequently, the Indonesian nickel price and market trends heading into 2025 and beyond reflect this recalibration in real time.

The Three-Layer Cost Pressure Explained

The nickel market perfect storm in Indonesia and the Middle East operates through three simultaneous pressure layers:

- Indonesian ore policy tightening reduces domestic laterite availability and forces substitution toward higher-cost Philippine feedstock, lifting the cost floor for a structurally significant portion of global supply.

- Environmental enforcement escalation in Indonesia creates forced production curtailments that remove output from the market regardless of commercial demand signals.

- Middle East conflict spillover creates a dual input cost shock through sulfuric acid shortages affecting HPAL operations and elevated energy costs affecting both HPAL and NPI across Indonesia's laterite processing complex.

Two of these three drivers are structural in nature. They will not reverse when hostilities end. The third, while event-driven, carries a duration profile that markets appear to be underestimating based on the barnacle and logistics analysis outlined above.

Oil Prices, EV Demand, and the Masked Demand Picture

Why Artificially Suppressed Oil Prices Are Creating a Delayed Reckoning

A critical and underappreciated dynamic in the current nickel demand outlook involves the relationship between oil price suppression and electric vehicle adoption. When oil prices remain artificially low through government intervention or strategic release of reserves, the economic case for switching to an EV weakens. Consumers face less urgency. Demand destruction that would ordinarily accelerate the EV transition does not materialise.

The consequence is that oil inventory drawdowns proceed faster than they would under free-market pricing, as demand destruction is deferred rather than triggered. This creates the conditions for an eventual price spike that cannot be controlled through the same dampening mechanisms, because the underlying inventory buffers have been quietly eroded.

China's passenger car market is already showing early warning signs of this dynamic. Overall passenger vehicle sales have weakened, dragging EV sales lower alongside them. While EV penetration rates within the segment remain robust, the absolute volume decline reflects the consumer pressure that elevated living costs are already creating.

The next major ASX story will hit our subscribers first

Energy Storage Systems: The Demand Driver Changing the Calculus

Why ESS Is Outpacing EVs as a Battery Demand Engine in 2025 and 2026

While EV demand growth has moderated in several key markets, energy storage system (ESS) deployment has accelerated sharply. ESS applications, including grid-scale battery installations for renewable energy integration and regional power security, do not carry the same consumer discretionary sensitivity as vehicle purchases. They are infrastructure-driven, policy-linked, and often funded at a utility or sovereign level.

Paradoxically, the Middle East conflict has itself become a catalyst for ESS demand in surrounding regions, as energy security concerns have accelerated procurement of battery storage systems as insurance against supply disruption. In addition, the lithium boom driven by battery storage expansion is creating parallel demand pressures across the broader battery materials complex, of which nickel is a key component.

For nickel specifically, ESS growth is a structurally significant demand diversifier. It means that even if EV sales face near-term headwinds from inflation and consumer weakness, the underlying demand growth for battery-grade nickel does not evaporate.

Price Outlook: Scenarios and Structural Constraints

Comparing Bullish and Bearish Cases for Nickel in 2026 and Beyond

| Scenario | Key Driver | Likely Price Outcome |

|---|---|---|

| Indonesian policy tightening deepens | Further quota reductions plus environmental enforcement | Strong upside, cost floor rises structurally |

| Middle East disruption extends beyond 6 to 9 months | Prolonged sulfur shortage, elevated energy costs | Sustained price support across laterite processing |

| Oil price spike materialises | EV demand acceleration alongside higher production costs | Dual demand-supply pressure, amplified upside |

| Broader global oversupply persists | Excess Class 1 nickel inventory on market | Caps near-term price gains despite deficit projection |

| Indonesian policy reversal | Quota relaxation and environmental enforcement eases | Downside risk to the deficit thesis |

The Class 1 vs. Class 2 Distinction and What It Means for Battery Supply Chains

Not all nickel is interchangeable. Class 1 nickel, which includes refined nickel metal and nickel sulfate, meets the purity requirements for lithium-ion battery cathode production. Class 2 nickel, which includes NPI and ferronickel, is primarily used in stainless steel manufacturing. Most Indonesian NPI production is Class 2 and cannot directly substitute for battery-grade Class 1 material without additional processing.

This distinction matters because a supply deficit in Class 1 nickel can coexist with apparent global oversupply in aggregate nickel statistics. Investors and procurement teams focused on battery supply chains need to track Class 1 availability specifically, not headline nickel production figures.

Nickel sulfide projects, which naturally produce Class 1 nickel, remain economically unjustifiable at current incentive prices. Until prices rise sufficiently and remain elevated long enough to support the capital expenditure required for sulfide development, the Class 1 supply pipeline remains constrained. Furthermore, Indonesian supply cuts are increasingly acting as a structural tailwind for nickel prices, adding further credence to the bullish case for Class 1 supply tightness.

Cobalt's Parallel Tightening Story

How Reduced HPAL Output in Indonesia Creates a Knock-On Effect for Cobalt

Cobalt and nickel share the same HPAL processing infrastructure in Indonesia. When HPAL output is curtailed, whether through sulfuric acid shortages, environmental enforcement, or ore availability constraints, cobalt production falls in parallel. The two metals are co-products of the same process, and supply disruption is structurally linked.

This relationship means the cobalt market is experiencing its own tightening dynamic through the same pressure channels driving the nickel market perfect storm in Indonesia and the Middle East. Compounding this, the DRC cobalt export ban in early 2025, while since partially relaxed through quota-based export resumptions, created a separate supply shock that intersected with the Indonesian HPAL slowdown. Cobalt prices have responded accordingly, and the structural case for continued tightening remains intact given the dual compression from both the DRC and Indonesian supply channels simultaneously.

How Investors Should Think About Structural Supply Changes

Identifying Market Recalibration Before Price Momentum Confirms It

The most actionable signal in commodity markets is rarely price movement itself. It is the earlier identification of structural change in supply and demand behaviour before that change is reflected in market pricing. The framework here involves monitoring shifts in trade flows, production behaviour by dominant national producers, and cost curve inflections driven by policy or input costs rather than demand fluctuations.

In the nickel context, the convergence of Indonesian ore policy, environmental enforcement, and Middle East logistics disruption represents exactly this type of multi-factor structural reconfiguration. Each element individually might be dismissed as temporary or manageable. Together, they describe a market that has been structurally repriced upward in terms of its cost floor, regardless of what spot prices are doing in any given week.

Mine supply falling year-on-year is one of the clearest signals available to project developers and operators that the investment environment is shifting. For companies with exposure to nickel sulfide assets in particular, the combination of rising cost floors for competing laterite production and an emerging supply deficit creates the conditions under which previously marginal projects begin to attract renewed attention.

The most actionable signal in the nickel market is not price momentum alone. It is the convergence of structural supply constraint through Indonesian policy, rising cost floors from energy and feedstock, and geopolitical disruption through Middle East logistics. When all three compress simultaneously, the resulting deficit is not a short-cycle event.

Frequently Asked Questions: The Nickel Market Perfect Storm

What Is Causing the Perfect Storm in the Nickel Market Right Now?

Three simultaneous pressures are converging: Indonesian mining quota reductions and environmental enforcement reducing domestic ore supply, the shift to higher-cost Philippine feedstock lifting the cost floor, and Middle East conflict disrupting both sulfuric acid availability and energy costs for laterite processing operations.

How Much of Global Nickel Supply Does Indonesia Control?

Indonesia controls approximately two-thirds of global nickel supply, giving it unmatched leverage over global pricing and availability. Even incremental domestic policy changes carry outsized market consequences.

What Is HPAL and Why Does Sulfuric Acid Availability Matter So Much?

High Pressure Acid Leach is the primary process for converting laterite nickel ore into battery-grade nickel sulfate. It consumes sulfuric acid in very large quantities. Any reduction in sulfuric acid availability, including through Middle East logistics disruption affecting sulfur supply, directly constrains HPAL output regardless of ore availability.

Will the Nickel Market Move Into a Deficit in 2026?

The INSG has projected a deficit of approximately 30,000 tonnes for 2026, which would be the first supply shortfall in roughly five years. While this is subject to revision based on how the Indonesian and Middle East dynamics evolve, the structural direction of travel points toward tighter supply. However, China's coal plant strategy also plays a role, as coal-backed energy infrastructure continues to influence the energy cost base for nickel processing across the region.

How Does the Middle East Conflict Affect Nickel Prices?

Through two channels: sulfuric acid shortages constraining HPAL output, and higher oil and gas prices elevating coal costs and thus the energy cost base for both HPAL and NPI operations across Indonesia.

How Long Could the Current Supply Disruptions Last?

The Indonesian policy and environmental drivers are structural and unlikely to reverse quickly. The Middle East logistics component carries a six to nine month minimum duration even if hostilities formally cease, due to vessel maintenance requirements including the barnacle accumulation issue affecting stationary supertankers in the Persian Gulf.

Is the Nickel Price Increase Structural or Temporary?

The honest answer is both. Two of the three core drivers, Indonesian policy and cost floor elevation, are structural. One, the Middle East disruption, is event-driven but with an unusually long tail. The combination creates conditions for a price increase that persists well beyond a typical short-cycle commodity shock.

Key Takeaways

- Indonesian mining quota reductions and environmental enforcement represent structural, not cyclical, supply constraints that will not reverse with a change in commodity sentiment

- The shift to Philippine ore has permanently raised the cost floor for a meaningful portion of Indonesian nickel output

- Middle East disruptions have created a dual input cost shock, affecting both sulfuric acid availability for HPAL and energy costs for NPI operations simultaneously

- The INSG's 30,000-tonne deficit forecast for 2026 would represent the first projected supply shortfall in the nickel market in approximately five years

- Oil price suppression is delaying rather than eliminating the demand-side catalyst for nickel, creating a potential delayed acceleration scenario when inventories tighten

- ESS demand is emerging as a structural demand diversifier that reduces nickel's dependence on EV sales cycles vulnerable to consumer sentiment

- Cobalt is experiencing a parallel tightening through the same HPAL supply channel, compounded by the legacy of the DRC export ban

- Nickel sulfide projects remain economically unjustifiable at current incentive prices, keeping the Class 1 supply pipeline constrained

This article is intended for informational and educational purposes only. It does not constitute financial or investment advice. Commodity markets involve significant uncertainty, and forecasts referenced herein, including supply deficit projections, are subject to revision based on evolving geopolitical, policy, and demand conditions. Readers should conduct their own due diligence before making investment decisions.

Want to Position Ahead of the Next Major Nickel Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including nickel and battery materials — instantly translating complex geological and market data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then start your 14-day free trial at Discovery Alert to ensure you're positioned before the broader market catches on.